Summary

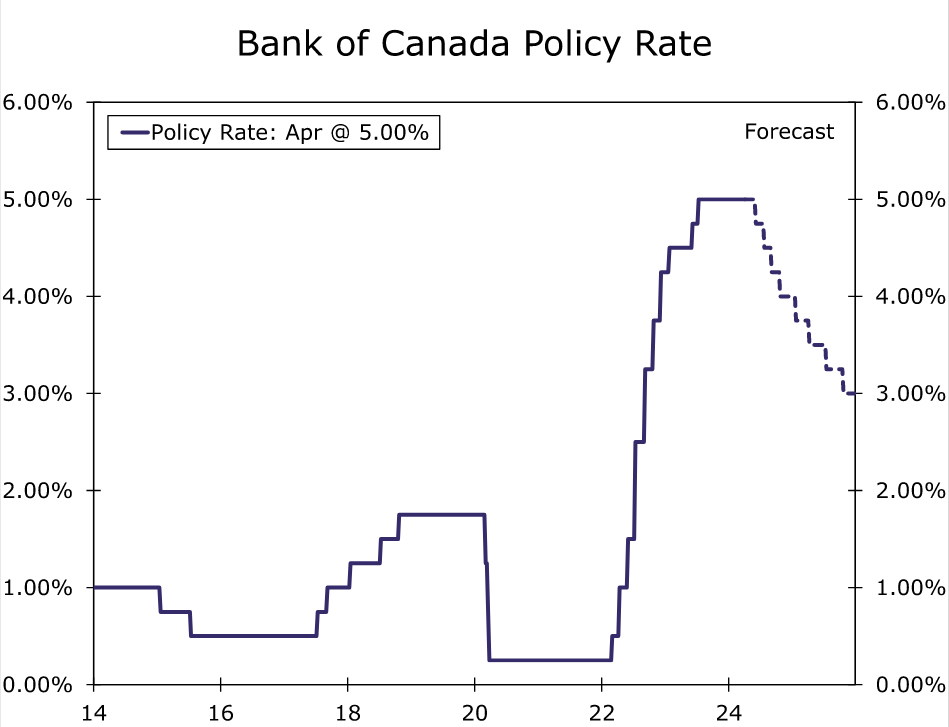

The Bank of Canada (BoC) held its policy interest rate steady at 5.00% at today’s monetary policy announcement, an outcome that was widely expected. However, the accompanying statement pointed to the potential for lower policy interest rates in the months ahead. BoC Governor Macklem said “we are seeing what we need to see” to lower policy interest rates, but that “we need to see it for longer to be confident that progress toward price stability will be sustained.” Macklem also said a June rate cut was within the realm of possibilities. Meanwhile, the BoC also lowered its CPI inflation forecasts, even as it upgraded its GDP growth forecasts.

While the outcome of the next monetary policy meeting in June is clearly data dependent, so long as core inflation remains contained and labor market trends subdued, we suspect that may be enough for the BoC to deliver an initial 25 bps policy rate cut at that meeting. We also forecast 25 bps rate cuts in July, September and October, for a cumulative 100 bps of rate reduction in 2024, which would see the policy rate end this year at 4.00%. Overall, we think the BoC will ultimately cut rates by more this year than currently expected by market participants over the rest of 2024. Moreover, with Bank of Canada easing this year likely to outpace that of the Federal Reserve, there is also potential for some further Canadian dollar weakness in the months ahead.

Bank of Canada Monetary Easing Door Slightly Ajar

The Bank of Canada (BoC) held its policy interest rate steady at 5.00% at today’s monetary policy announcement, an outcome that was widely expected. The BoC did not offer any clear guidance regarding the timing of monetary easing, but the details of the announcement nonetheless pointed to the potential for lower policy interest rates in the months ahead.

BoC Governor Macklem said the central bank has concluded that overall, data since January have increased confidence that inflation will continue to come down gradually even as economic activity strengthens. Of note, Macklem said “we are seeing what we need to see” to lower policy interest rates, but that “we need to see it for longer to be confident that progress toward price stability will be sustained.” The BoC said that labor market conditions continue to ease and that there are recent signs wage pressures are moderating, with many measures of wage growth now seen in a range of 3.5%-4.5%, down from 4%-5% previously.

On the more hawkish side, the BoC said cutting rates too soon could jeopardize the progress on inflation to date, and that its wants to see evidence downward momentum is sustained and that the recent decline in core inflation is not a temporary blip. The BoC also raised its estimate of the neutral policy interest rate by 25 bps to a range of 2.25%-3.25%, from a range of 2%-3% previously.

Clearly, the timing of potential Bank of Canada monetary easing is a balancing act, and the hawkish elements did come with some qualifiers. For example, Macklem also said we “don’t want to leave monetary policy this restrictive longer than we need to” and, in the post-meeting press conference he said that June was in the realm of possibility for rate cuts, and that the higher neutral rate does not impact “near-term” policy.

Finally, the BoC’s updated economic forecasts reflected the notion that stronger economic growth can co-exist with slowing inflation. There was a sharp upgrade to the 2024 GDP growth forecast to 1.5%, including a Q1 GDP growth forecast of 2.8% quarter-over-quarter annualized. In contrast, the 2025 GDP growth forecast was lowered only slightly to 2.2%. Meanwhile, the central bank lowered its inflation forecast for this year. Looking at the year-end (Q4/Q4) CPI inflation forecasts for 2024, 2025 and 2026, the BoC sees inflation at 2.2%, 2.1% and 2.1% respectively—only slightly above the 2% inflation target.

In our view, the announcement suggests the BoC is comfortable with recent economic trends and that, should they continue, that will pave the way for monetary easing. With two more inflation reports and one more employment report ahead of the BoC’s 5 June announcement, so long as core inflation remains contained and labor market trends subdued, we suspect that may be enough for the BoC to deliver an initial policy rate cut at the June meeting.

Canadian Economic Trends Mixed in Early 2024

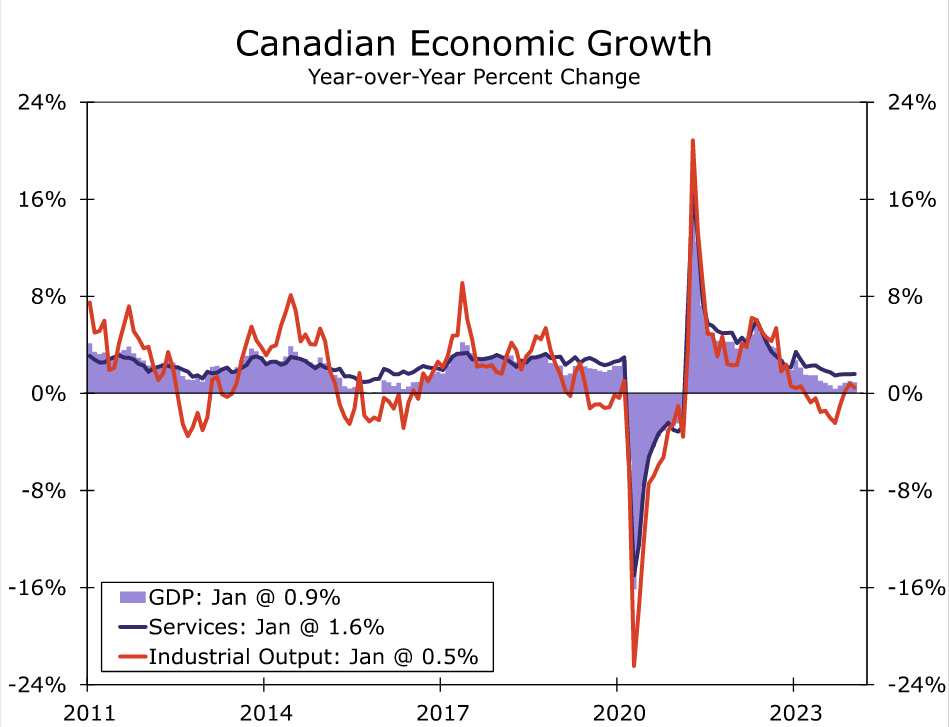

Canada’s economic trends have been mixed at the start of this year, though overall we believe they are consistent with easing price pressures, and thus Bank of Canada monetary easing in the months ahead. On the strong side, broader GDP growth firmed a bit around the turn of the year. Q4 GDP grew 1.0% quarter-over-quarter annualized, more than reversing its Q3 decline, with growth supported by consumer spending and exports. January GDP also rose 0.6% month-over-month, more than forecast, and Statistics Canada’s advance estimate is for February GDP to increase by 0.4%. Against this backdrop we have lifted our Canadian Q1 GDP growth forecast to 2.4% quarter-over-quarter annualized, with the risks around that forecast tilted toward a stronger outcome.

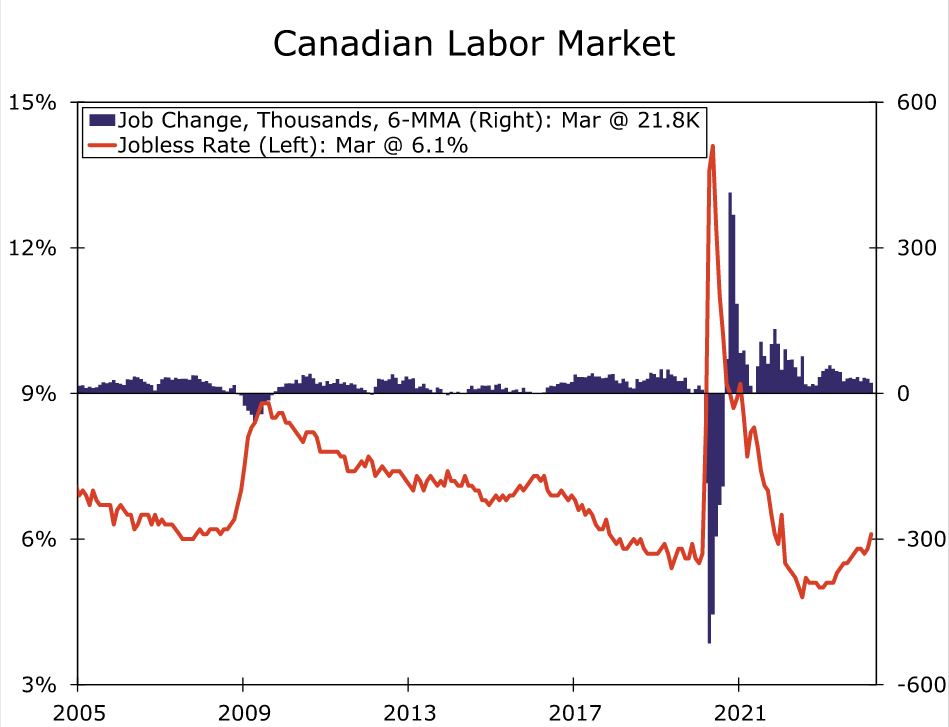

However, despite the stronger start to this year, there are still reasons to expect Canada’s economic growth to slow as the year progresses. The previous rise in interest rates means that the household debt service ratio, at 15.0% of disposable income, is at its highest level since 1990, which should be a headwind for the consumer moving forward. Elsewhere, although business sentiment and sales expectations improved slightly in Q1, they remain at subdued levels. A softening in Canada’s labor market also likely portends a slowing in GDP growth moving forward. Canadian employment unexpectedly declined by 2,200 in March, as full-time employment and part-time employment both fell, while the unemployment rate jumped more than expected to 6.1%.

Inflation Pressures Are Gradually Ebbing

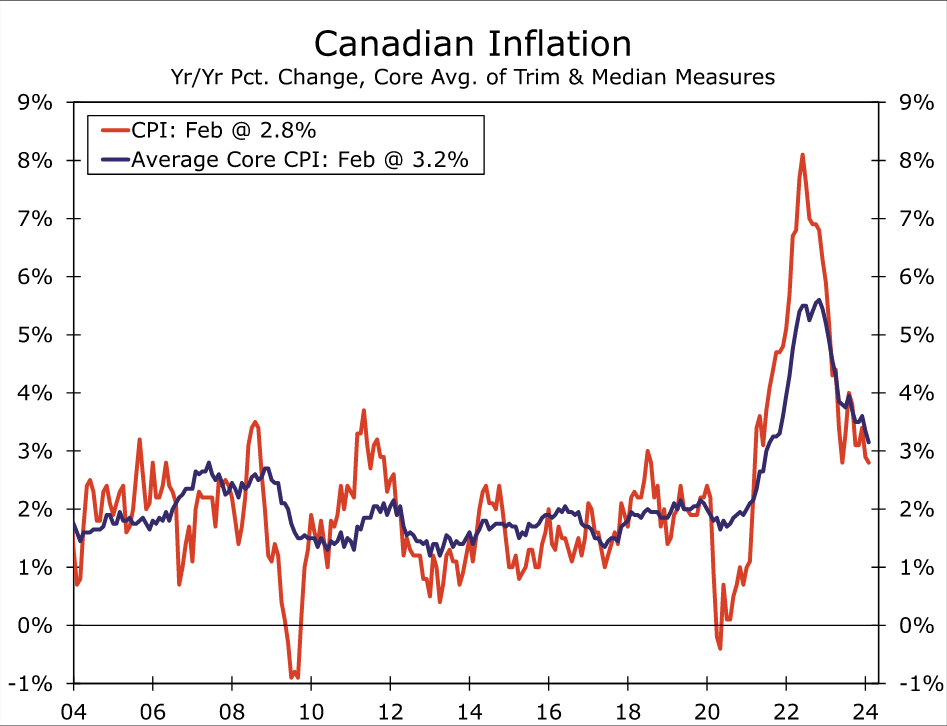

In contrast to the stronger economic growth seen early in 2024, there has been a noticeable slowing in inflation pressures early this year, an encouraging development for the Bank of Canada. CPI inflation surprised to the downside in both January and February, with headline and core inflation measures decelerating. For February, the headline CPI rose 2.8% year-over-year, while the average core CPI rose 3.2%. Significantly, however, underlying inflation pressures appear to be running closer to the central bank’s target over the most recent months, as the average core CPI rose by 2.2% on a three-month annualized basis in February.

So long as inflation remains contained, we view the Bank of Canada as on course to deliver an initial 25 bps policy rate cut to 4.75% at its June monetary policy meeting. We also forecast 25 bps Bank of Canada rate cuts in July, September and October, for a cumulative 100 bps of rate reduction in 2024, which would see the policy rate end this year at 4.00%. We expect a steady pace of rate cuts to continue in 2025, forecasting a further cumulative 100 bps of rate reduction, which would see the policy rate end next year at 3.00%. Overall, we think the BoC will ultimately cut rates by more this year than the cumulative 63 bps of rate cuts priced in by market participants for the rest of 2024. Moreover, with Bank of Canada easing this year likely to outpace that of the Federal Reserve, there is also potential for some further Canadian dollar weakness in the months ahead.

held its policy interest rate steady at 5.00% at today's monetary policy announcement, an outcome that was widely expected. However, the accompanying statement pointed to the potential for lower policy interest rates in the months ahead. BoC Governor Macklem said “we are seeing what we need to see” to lower policy interest rates, but that “we need to see it for longer to be confident that progress toward price stability will be sustained.” Macklem also said a June rate cut was within the realm of possibilities. Meanwhile, the BoC also lowered its CPI inflation forecasts, even as it upgraded its GDP growth forecasts.){kind=link}