Markets

Eurostat today published deficit and debt data for the years 2020-2023 in E(M)U). The euro area government deficit declined marginally from 3.7% of GDP in 2022 to 3.6% in 2023. The government debt to GDP ratio decreased over the same period from 90.8% to 88.6%. Zooming in on Belgium, Eurostat reported an increase of the deficit from 3.6% of GDP to 4.4% of GDP with the debt ratio rising from 104.3% to 105.2%. Other notable underperformers in the euro zone include France (-5.5% deficit & 110.6% debt), Italy (-7.4% & 137.3%) and Slovakia (-4.9% & 56%). Bloated public finances are one of the key drivers of our fundamental bearish view on (long term) interest rates. Especially since the ECB left the scene as unlimited, price-insensitive buyer of government bonds under its asset purchase programmes. Credit risk premia make their comeback while the snowball effect and some global trends (energy transition, ageing, defense,…) raise structural spending needs. In June, Europe will again launch excessive debt procedures against some countries (including Belgium) after easing measures in the wake of the Covid-pandemic. The (very) long end of European yield curve continued underperforming today while there was no one-on-one correlation with the timing of today’s figures. German yields currently add up to 3.6 bps (30-yr) with (minor) new YTD highs for tenors ranging from 5-yr until 30-yr. The German 2-yr yield tested the psychological 3% mark for a second session running. Risks related to tomorrow’s April EMU PMI’s seem asymmetric with anything apart from a huge negative surprise possibly sufficient to push yields beyond these recent levels. Changes on the US yield curve were more or less similar varying between -1 bp (2-yr) and +3.3 bps (30-yr). UK Gilts continue their outperformance following Friday’s reset. Bank of England comments cumulated into a shift in market thinking, putting the Bank of England more on par with the ECB than with the Fed. Short term UK yields lose up to 4 bps and contribute to follow-up losses in sterling. EUR/GBP rises from 0.8602 to 0.8638, the highest level since the first trading day of the year. The November top at 0.8768 is the next real reference. GBP/USD underperforms given today’s USD strength, losing a big figure to GBP/USD 1.23. Losses for EUR/USD are technically insignificant with the pair changing hands at 1.0630.

News & Views

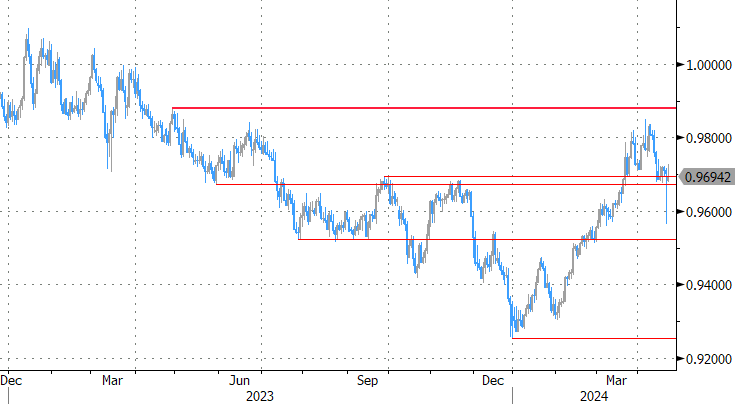

The Swiss National Bank announced that it will raise the minimum reserve requirements for domestic banks. The change will start from July 01 2024 on. The new regulation includes the SNB increasing the minimum reserve ratio from 2.5% to 4%. The central bank also broadened the basis for calculating the minimum reserve. Liabilities arising from cancellable customer deposits (excluding those tied to pension provision) will now be included. The SNB said that the adjustments will ensure that the implementation of the SNB’s monetary policy remains effective and efficient. The new setup will reduce the SNB’s interest rate cost after the bank recorded a loss in 2023. The SNB states that the amendments will not affect the current monetary policy stance. After a protracted decline of the Swiss franc between New Year (EUR/USD <0.93) and early April (EUR/CHF 0.984), CHF recently found a new short-term equilibrium near EUR/CHF 0.97.

Belgian consumer confidence dipped slightly in April from -5 to -6. The decline masked a clear deterioration in employment expectations (unemployment indicator rose from 17 to 24). According to the assessment of the NBB, the announcement of the bankruptcy and closure of several companies and retailers did not go unnoticed by consumers, who indicated that they are much more concerned about how the job market will develop in the next three months. For the second month in a row, the deterioration in this component was clear to see (17 from 10 in March). On the other hand, consumer expectations regarding the general economic situation in Belgium improved (-18 from -20). On a personal level, households revised slightly upwards their expectations of their own financial situation (-1 from -2) along with their saving intentions (18 from 17).

Graphs

EMU 10-yr swap yield tests the YTD top. Can PMI’s trigger a break tomorrow?

EUR/CHF: higher reserve requirement by SNB doesn’t impact CHF

Geopolitical tensions move to the background and so do Brent crude prices

GBP/USD: sterling extends losses after BoE signals willingness to go the ECB’s way.

U). The euro area government deficit declined marginally from 3.7% of GDP in 2022 to 3.6% in 2023. The government debt to GDP ratio decreased over the same period from 90.8% to 88.6%. Zooming in on Belgium, Eurostat reported an increase of the deficit from 3.6% of GDP to 4.4% of GDP with the debt ratio rising from 104.3% to 105.2%.){kind=link}