Markets

Today’s eco calendar was light compared to earlier this week but that didn’t prevent a further sell-off on core bond markets. April US durable goods orders were stronger than expected, but March figures face a downward revision. Core shipments, input for GDP (investments), increased by 0.4% M/M following a 0.3% decline in March (earlier reported flat). US yields currently add around 2 bps across the curve. The US 2-yr yield (4.95%) has its eyes again on the psychologic 5% mark. We hold our view that this resistance will hold as long as the Fed categorically rules out the possibility of another rate hike (if necessary). Wednesday’s released FOMC Minutes showed that Fed chair Powell undersold this risk after the May 1 policy meeting. However, for now we expect this 5%/5.05% resistance level to hold. US money markets are now back positioned for only one 25 bps rate cut in December, compared with two rate cuts (September/December) at the start of the week. Apart from hawkish FOMC Minutes, yesterday strong PMI’s played a role as well as did the global context with strong underlying core inflation in the UK and stubborn wage pressure in Europe. The debate on the neutral rate is gaining more and more traction as well. The median estimate in March projections already showed a slight increase from 2.5% to 2.56% with potentially more to come in June. Heavyweight Fed governor Waller touched on the issue in a speech today. He said that the US is on an unsustainable fiscal path. If the growth in the suppl of US Treasuries begins to outstrip demand, this will mean lower prices and higher yield which will put upward pressure on the neutral rate. Waller mentioned demographics, globalization and regulation amongst factors that pushed the neutral rate to too low levels the past years. German yields add up to 2.5 bps today as well with the front end of the curve underperforming. The German 2-yr yield rises to the highest level since October 2023 with EMU money markets reducing ECB policy rate expectations to only two rate cuts this year.

European stock markets lose up to 0.5% today following yesterday’s WS correction. Technical bearish engulfing signs in the US at the open don’t lead to follow-up losses yet but technical charts still suggest room for a short term correction. EUR/USD rises from 1.0810 to 1.0840 on the back of the repositioning in short term EUR rates.

News & Views

Czech economic sentiment declined in April from 97 to 96.4 while consensus expected a limited further improvement to 97.3. The decline was mainly due to an unexpected setback in consumer confidence (101.6 from 103.8). Business confidence was nearly unchanged (95.4 from 95.6). Confidence in the economy among entrepreneurs increased in the trade (+3.7 points) and the selected services sector (+ 1.1 points), but deteriorated in the construction sector (- 1.2 points) and in the industry (- 2.0 points). Respondents of the consumer survey expecting a deterioration in the overall economic situation in the next twelve months significantly increased. The assessment of both consumers’ current financial situation and their financial situation in the next twelve months is unchanged. The share of consumers who believe that the current time is not suitable for making major purchases also didn’t change. The decline in consumer sentiment is a bit surprising as the decline in inflation resulting in a higher real wages/disposable income should support consumers’ spending capacity going forward. After a rebound over the previous two months, delayed Fed/global rate cut expectations currently slow CZK gains with EUR/CZK holding near 24.71.

Swiss National Bank governor Jordan said that even a moderate rise inflation can have a serious impact on people’s standard of living, especially for low wage owners. In this respect it is very important for the SNB to fulfill its mandate. With respect to the interruption of profit payments from the previous financial year to the cantons, Jordan indicated that the SNB always had reservations with respect to the use of its reserves. Payouts, if any, are a side-product. The main contribution of the SNB for the country is to provide stability. Jordan also indicated that he is not in favour of the SNB publishing minutes of the internal deliberations at monetary policy meetings. The SNB in March reduced its policy rate by 25 bps before the Fed and the ECB as inflation declined firmly within the 0%-2% range. Swiss inflation in April reaccelerated slightly to 0.3% M/M and 1.4% Y/Y (from 1.0%). In the wake of this release, markets scaled back expectations for a follow-up rate cut in June to about 50%. Still the Swiss franc remains in the defensive. At EUR/CHF 0.9925, CHF currently trades at the weakest level against the euro in more than a year.

Graphs

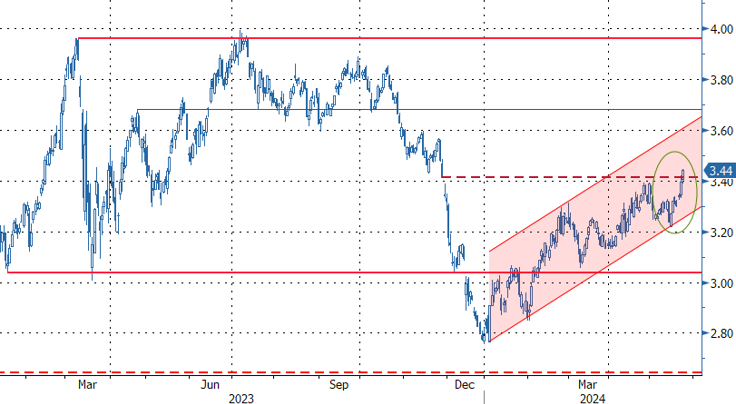

EU 2y swap rate: market doesn’t buy European inflation isolation narrative…

EUR/CHF: …Switzerland on the contrary…

USD/JPY: yen approaches danger zone as unilateral intervention prove useless in a higher-for-longer world

Nasdaq: technical bearish engulfing pattern suggests room for a short term correction

, increased by 0.4% M/M following a 0.3% decline in March (earlier reported flat). US yields currently add around 2 bps across the curve.){kind=link}