Summary

- We expect the FOMC will leave its target range for the federal funds rate unchanged at 4.25-4.50% at its upcoming meeting on May 6-7, a view widely shared by financial markets and economists. Market pricing currently implies only a 9% probability of the FOMC cutting the fed funds rate by 25 bps.

- Since the FOMC concluded its last policy meeting on March 19, the Trump administration has announced unprecedented changes to trade policy. While some of these plans have been temporarily paused, tariffs remain significantly higher than what was generally anticipated prior to the April 2 “Liberation Day” announcement. After severe turmoil in financial markets initially following the announcement, markets have calmed somewhat, but financial conditions remain tighter than when the FOMC gathered nearly six weeks ago.

- “Soft” survey data on consumer and business sentiment have also weakened sharply over the past six weeks. Yet, “hard” economic data have remained in good shape. Steady initial jobless claims point to the labor market maintaining its footing, while the year-over-year rate of core PCE inflation is on track to ease to a four-year low of 2.6% when data for March print on April 30.

- Public comments by Fed officials during the inter-meeting period have emphasized the uncertainty that hangs over the outlook as a result of the changing trade environment. Higher tariffs present a tricky challenge for the Committee, as they threaten to both weaken the labor market and raise prices. There seems to be broad consensus on the Committee that the current monetary policy setting is well positioned to respond to changes in the outlook that threaten either side of the dual mandate.

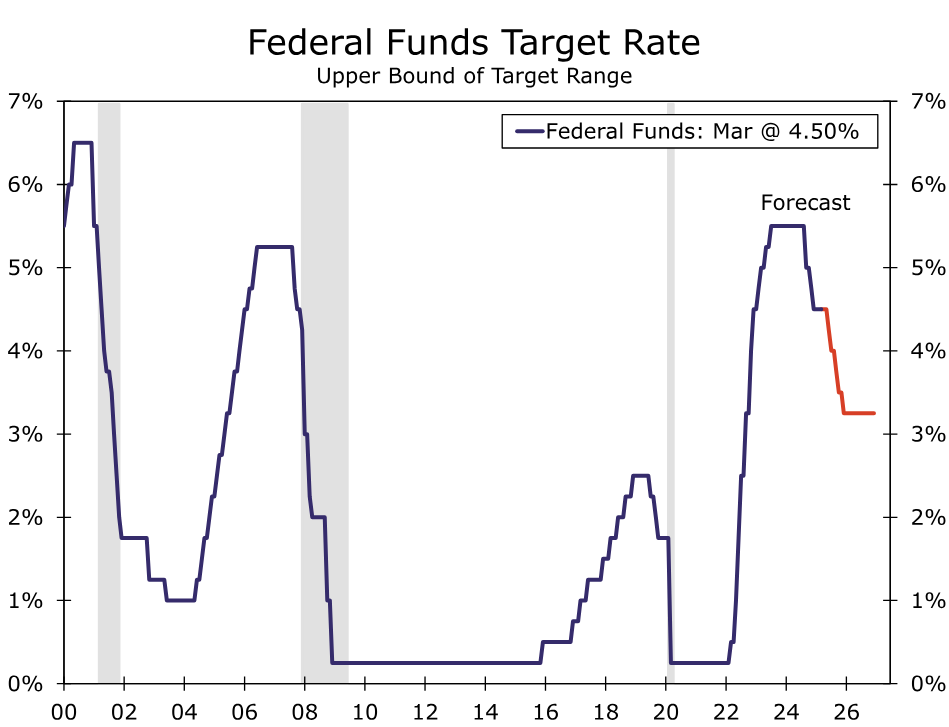

- Our current forecast looks for the FOMC to reduce the federal funds rate by 125 bps this year, starting with the June meeting. Some dialing back in the U.S. posture on tariffs, the relatively benign run of recent “hard” data and the patient comments from key Fed officials in recent weeks lead us to believe the risks are skewed toward the first rate cut occurring later than the June meeting. That said, with monetary policy still somewhat restrictive and weaker economic growth expected to weigh on the labor market in the months ahead, we still think the FOMC will reduce the federal funds rate this year by more than the 50 bps implied by the median projection in the March meeting’s summary of economic projections.

When in Doubt, Wait It Out

Unprecedented changes in U.S. trade policy, which have caused financial markets to whipsaw, have dominated the headlines since the Federal Open Market Committee (FOMC) concluded its last policy meeting on March 19. President Trump announced his “Liberation Day” tariffs on April 2. As we noted in a report we published at that time, Trump imposed a 10% universal levy on all of America’s trading partners. Additionally, he announced “reciprocal” tariff rates that were based largely on the size of an individual country’s bilateral trade surplus with the United States.

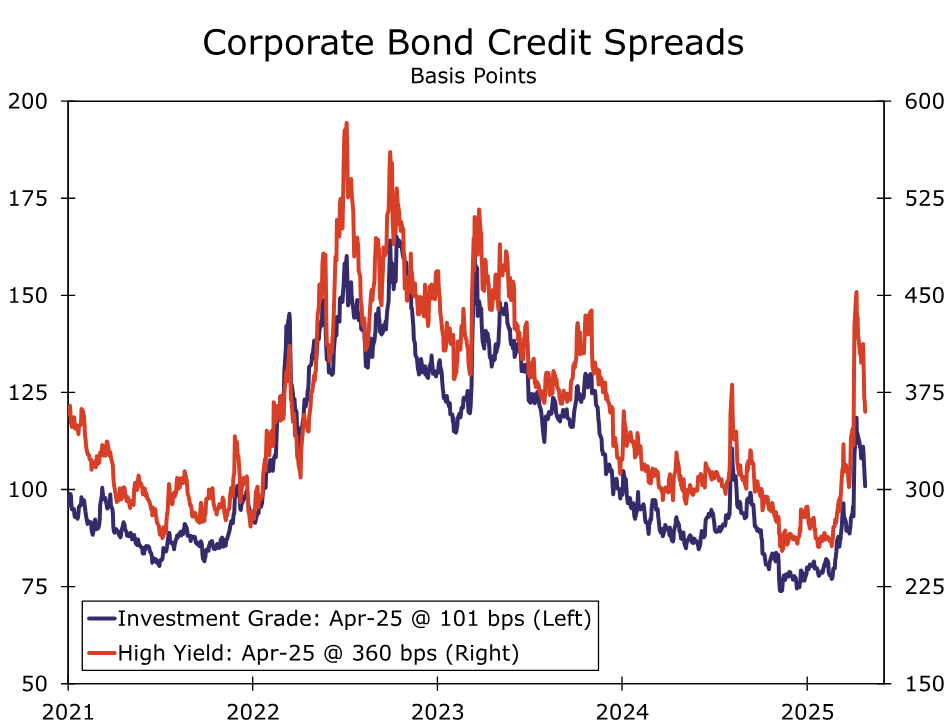

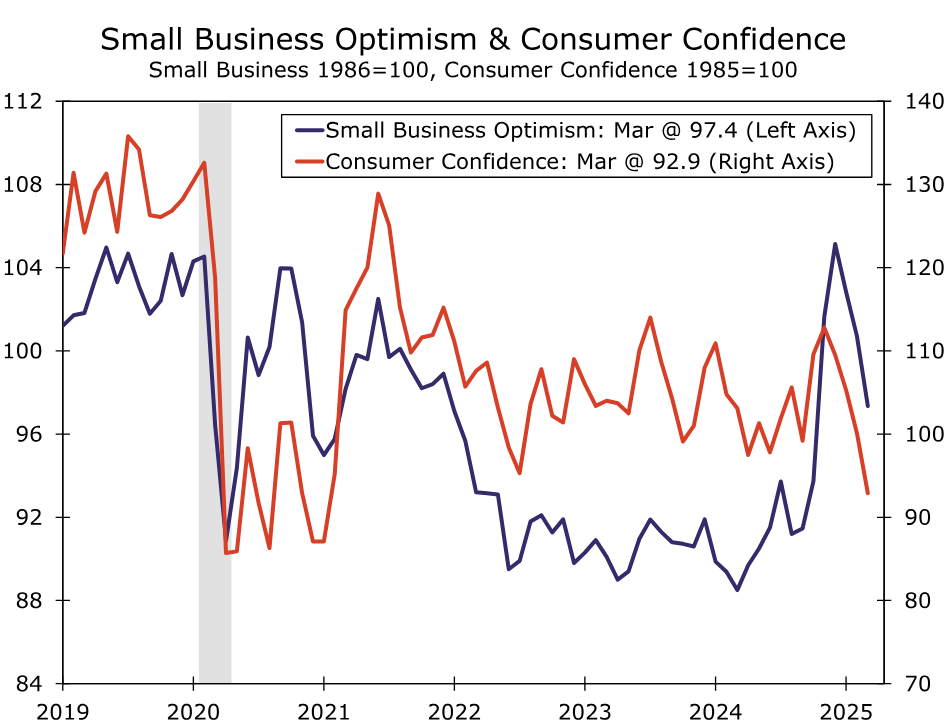

The reciprocal tariff rates, which were generally higher than most observers had expected, immediately caused financial markets to nosedive. The S&P 500 index plunged about 15% between its close on April 2 and its low on April 7, while corporate bond spreads widened markedly (Figure 1). Financial markets have steadied, due in part to the president’s decision on April 9 to pause implementation of the reciprocal tariffs for 90 days, but stock market indices generally remain lower and corporate bond spreads wider than when the FOMC last met. “Soft” data that measure consumer and business sentiment generally have deteriorated over the past six weeks or so (Figure 2). The optimism component of the NFIB small business survey has fallen to its lowest level since the November elections while the Conference Board’s measure of consumer confidence has retreated to its lowest level since the pandemic.

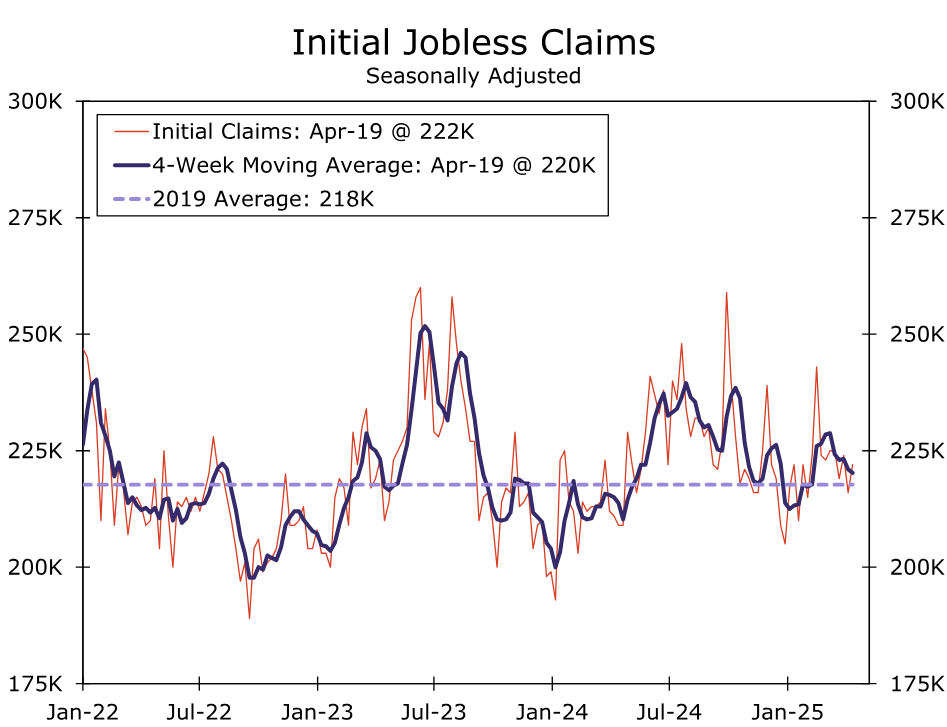

That said, there are few signs of doom and gloom in the “hard” data. The employment report released on April 4 showed nonfarm payrolls growing a strong 228K in March, while the 0.1 percentage point rise in the unemployment rate was due largely to rounding effects. The number of individuals filing for unemployment insurance for the first time has remained low in recent weeks, indicating that businesses remain hesitant to displace workers (Figure 3). Retail spending increased by a robust 1.4% in March relative to the previous month, although some of this strength likely reflects consumer purchases ahead of tariff-related price increases or shortages. Even manufacturing output rose at a respectable 5.6% annualized pace in Q1.

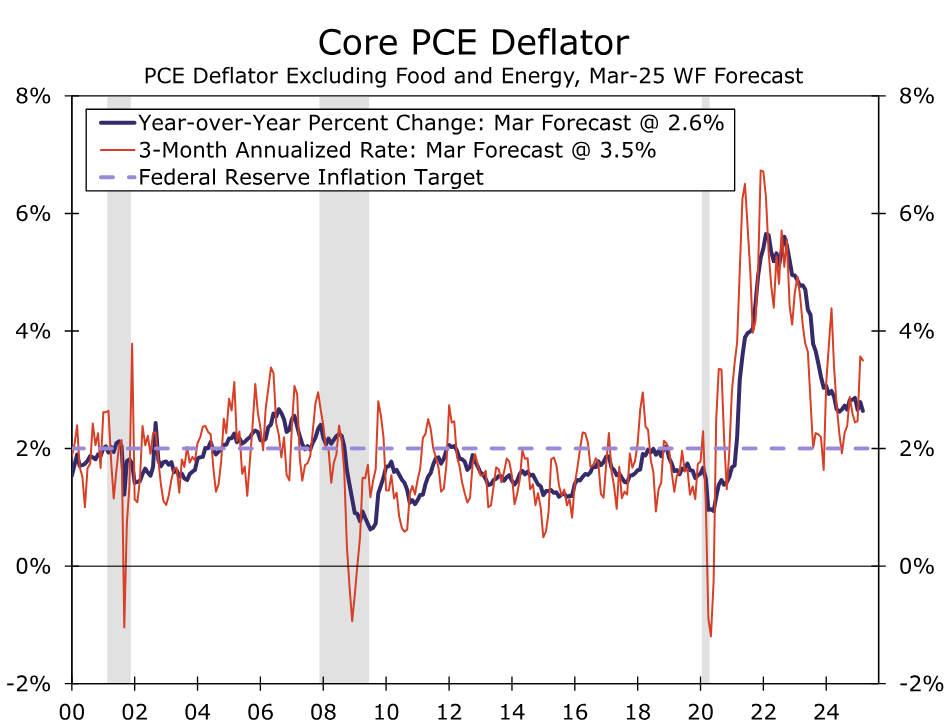

On the inflation front, there are few signs of tariff-related increases in consumer prices, at least thus far. Excluding food and energy prices, the consumer price index (CPI) edged up only 0.1% in March relative to February. We project the core PCE deflator, which most Fed officials believe is a better measure of underlying price growth than the core CPI, also will rise only 0.1% in March. (PCE inflation data for March are scheduled for release on April 30.) If realized, the year-over-year rate of core PCE inflation would drop to 2.6%, the lowest rate since March 2021 (Figure 4).

Of course, hard data tend to be backward looking, and it is still far too early to proclaim that the president’s tariffs, both implemented and threatened, have been a non-event for the U.S. economy. Fed Governor Christopher Waller used the words “uncertain” or “uncertainty” ten times in a speech on the U.S. economic outlook that he delivered on April 14. A few days later, Chairman Jerome Powell stated that “the U.S. economy is still in a solid position,” but he noted that the effects of the administration’s policy changes “on the economy remain highly uncertain.” Powell went on to say that, for now, the FOMC is “well positioned to wait for greater clarity before considering any adjustments to our policy stance.” John Williams, the president of the Federal Reserve Bank of New York, said that the U.S. economy, is “in a very good place” and that he does not “see the need to change the fed funds rate any time soon.” Other Fed officials also have made clear that they want to await further clarity in the economic data and on the economic policy front before changing course for U.S. monetary policy.

Given these recent public comments by Federal Reserve officials, we firmly believe the FOMC will keep its policy stance unchanged at the conclusion of its meeting on May 7. Our expectation is also reflected in current market pricing which, as of this writing, implies a 9% probability of a 25 bps rate cut on May 7. We also expect the post-meeting statement and press conference to remain noncommittal about future policy action in an effort to preserve maximum flexibility. The statement may change to more directly emphasize the uncertainty and risks caused by the recent changes to trade policy, but otherwise we see few other changes to the statement. In the press conference, Chair Powell probably will reiterate that uncertainty remains high but that policy is well positioned to respond to conditions as they evolve to both sides of the dual mandate. We will be listening closely for any signs of how Powell and the rest of the Committee are thinking about the balance of risks to the dual mandate and how timing effects may influence future policy decisions (e.g., what if price increases occur before layoffs, or vice versa?).

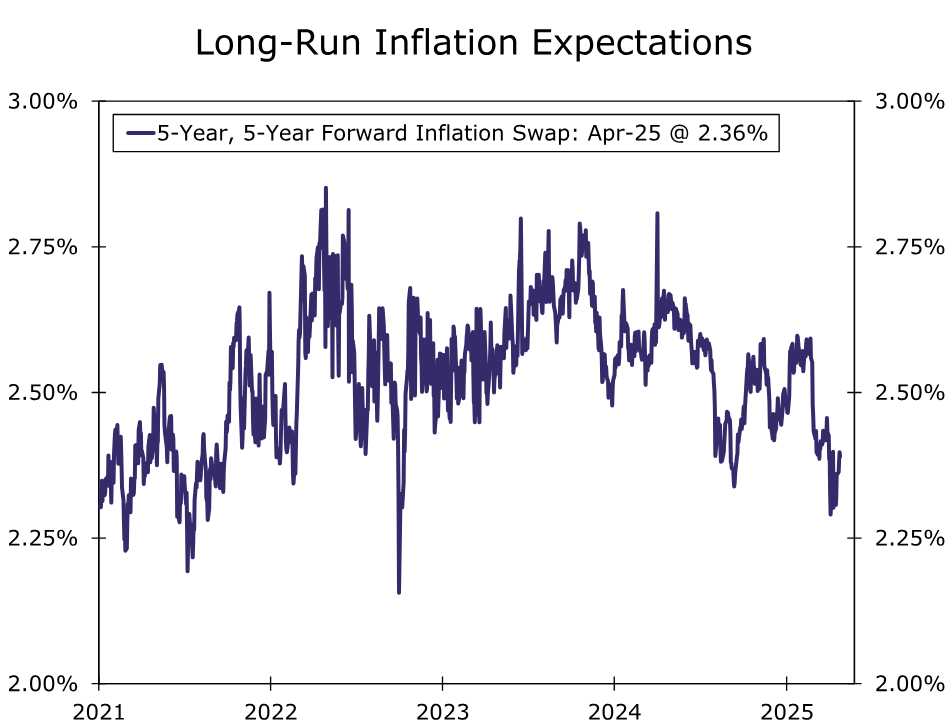

We believe the hit to U.S. economic growth and the labor market from higher tariffs will induce the FOMC to move toward a more neutral policy stance as the year progresses, even in the face of higher inflation. Econometric models suggest that the increase in inflation from tariffs should be transitory so long as long-term inflation expectations remain well-anchored. Although the University of Michigan’s survey of consumer sentiment has shown rising long-term inflation expectations in recent reports, other surveys, such as the New York Fed’s Survey of Consumer Expectations, have not shown the same increase. Furthermore, market-based measures of longer-term inflation expectations remain well-anchored and actually have fallen slightly in the weeks since President Trump announced his Liberation Day tariffs on April 2 (Figure 5).

Our current forecast looks for the FOMC to reduce the federal funds rate by 125 bps this year, with no change to the policy rate in 2026 (Figure 6). More specifically, our forecast projects five 25 bps rate cuts at the final five FOMC meetings of the year, starting with the June meeting. Some dialing back in the U.S. posture on tariffs, the relatively benign run of recent “hard” data and the patient comments from key Fed officials in recent weeks lead us to believe the risks are skewed toward the first rate cut occurring later than the June meeting. That said, we still think the FOMC will reduce the federal funds rate this year by more than the 50 bps implied by the median projection in the March meeting’s summary of economic projections. We will update our economic forecast the week of May 5, after we have heard from the FOMC and seen the April employment report.

{kind=link}