Summary

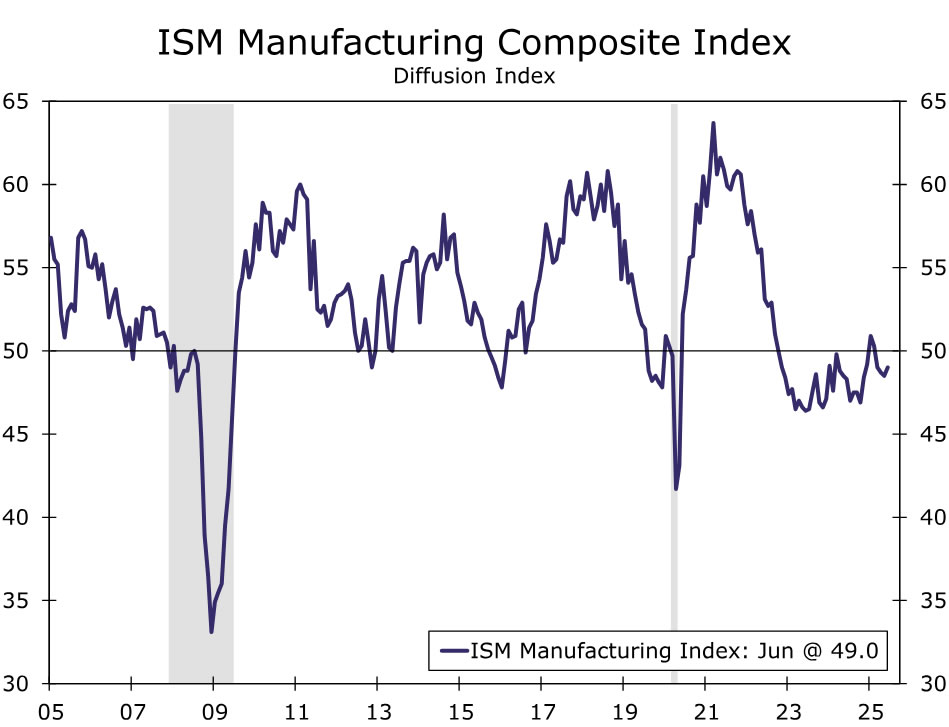

A rebound in production and a slower drawdown in inventories resulted in a more modest pace of contraction for ISM manufacturing in June. But worries about tariffs continue to crimp supply, leaving manufacturers fraught with trade-offs for holding inventory as pricing pressure builds.

Static in the Air

There is something in financial markets at the moment that is reminiscent of what you might experience just before a lightning strike. Equity markets testing record highs is analogous to the way the air becomes charged due to the accumulation of static electricity. Policymakers at the Fed say they are “well positioned to wait” before lowering rates, but that tingling sensation on your skin is the inevitable reaction to the relentless drumbeat of pressure from the White House to cut sooner. At issue of course is the degree to which tariffs will lead to higher inflation thereby justifying the Fed’s ‘wait-and-see’ approach or if the pass-through effect will continue to be as muted as it has been thus far, thereby clearing the path for lower rates.

Only hard inflation data confirming rising prices will be strong enough to ionize the air, but in this latest read on activity in the manufacturing sector, there is a case that supply chains remain disrupted, inventory management is fraught with trade-offs and pricing pressure is mounting.

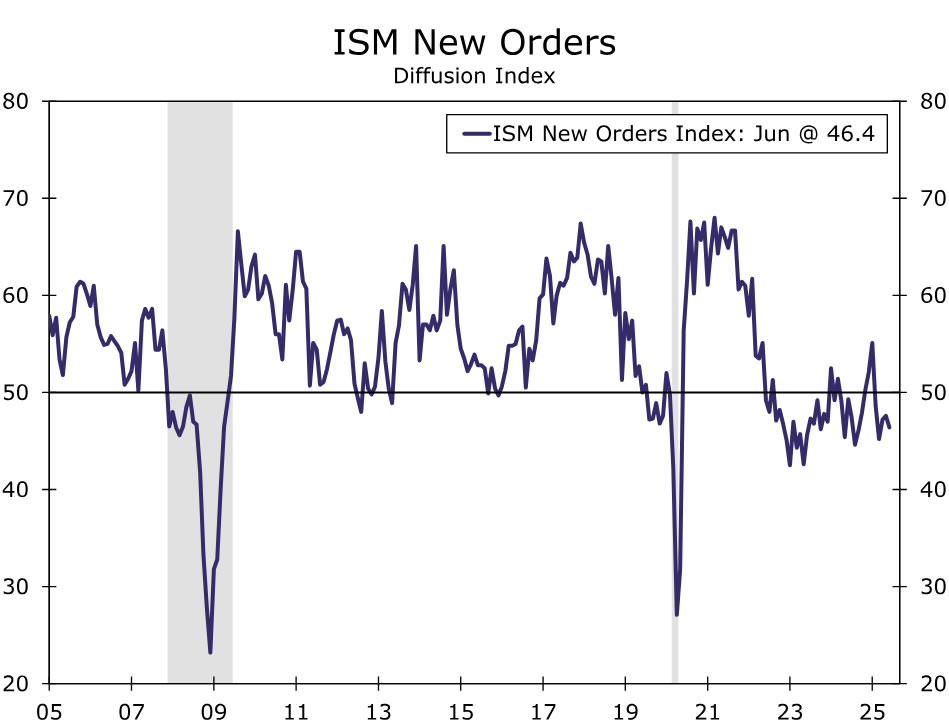

Tariffs are a top-of-mind worry across businesses with nine out of ten purchasing managers mentioning it in their responses. While tariffs are a universally held concern, it is clear that some industries are impacted more than others. In the machinery space, for example, one respondent said the “tariff mess has utterly stopped sales globally and domestically. Everyone is on pause. Orders have collapsed.” The new orders component dropped to 46.4.

That drop in orders was offset last month with a near-five point pop in current production, which led the overall ISM manufacturing index up half a percent to 49.0 in June. The report still paints the picture of a manufacturing sector rife with challenges. We take the rise in production in June with a grain of salt as it came after a weaker trend the past few months and there was a near-even split between the number of industries reporting expansion versus contraction in current production. We expect the rise in production more so reflects a mere rebound after a couple of months of halted activity rather than the start of renewed growth. Ultimately, the only two things rising on trend in today’s environment are wait times and prices; only supplier deliveries has an impact on the headline ISM.

Supplier deliveries, which measures the length of lead time for manufacturers to secure inputs, fell to 54.2 last month but remained in expansion and continued to be the largest counterweight to other components driving the composite index below 50. The measure is still consistent with longer wait times, a potential sign of building price pressure.

Inventories could be serving as a bulwark against the immediate pass-through of higher prices but those defenses are crumbling. The inventories index rose 2.5 points to 49.2; that means firms are still drawing down stockpiled inputs to sustain production, but the pace of that drawdown has slowed. When assessing their customer’s inventories, firms suspect those stockpiles are also too low and being drawn upon more incrementally.

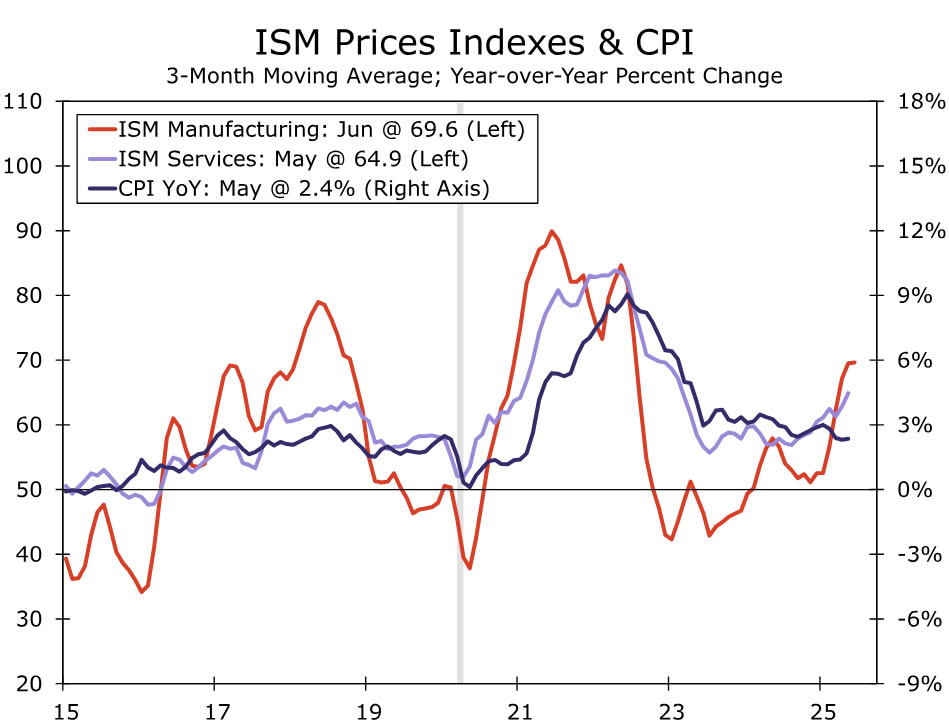

While the extent of tariff-induced inflation remains to be seen, the trend move higher in the ISM manufacturing prices paid index certainly suggests manufacturers are operating in a higher-cost environment. The prices paid index has now risen in nine of the past twelve months and remains the highest of any component above its prior six-month average. As the nearby chart shows, the overall consumer price index tends to track more closely with service-sector price pressure, but early price pressure tends to show up for manufacturers first.

Manufactures read on the labor market has been sour for some time. The employment component fell in June, keeping the index well-below the breakeven reading signaling a decrease in manufacturing jobs. We get the ISM services measure and the full nonfarm payroll report for June this Thursday, where we look for a slower pace of hiring. The stable moderation in the labor market has given the Fed cover to wait and assess the persistence of coming price pressure, but this ‘stable’ read on the labor market has begun to be called into question, increasing the importance around Thursday’s data.

{kind=link}