Despite an upward revision in the forecast for inflation, the Bank of Japan remains squarely focussed on demand-side drivers of inflation when considering the timing of the next cut.

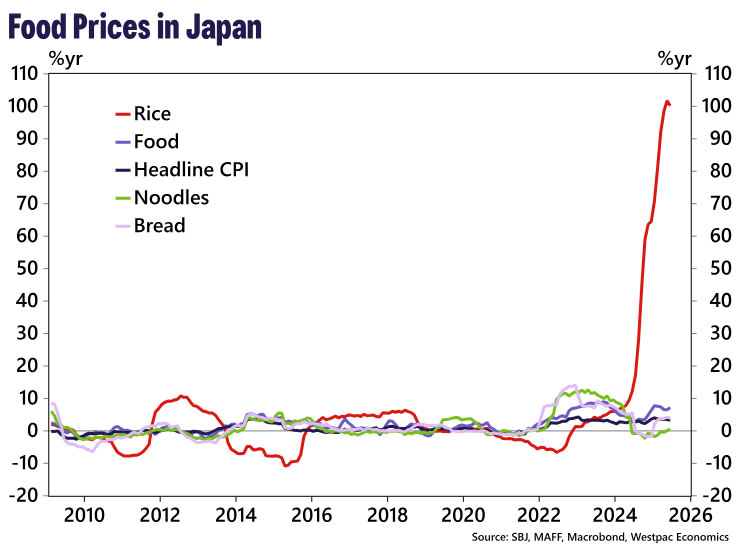

The Bank of Japan (BoJ) left its policy settings unchanged at its July meeting, but revised up its inflation outlook, particularly for FY2025 (ending March 2026). Median estimates for CPI (ex. fresh food) were nudged up to 2.7%yr for FY2025 (ending March 2026) from 2.2% previously. The revision was driven primarily by higher rice prices, which are included in the core measure. With the upward revision for FY2025 driven by a supply-side shock, the BoJ remain confident in achieving sustained inflation at their 2.0%yr target by the end of the forecast period. There were minimal adjustments to the GDP outlook despite acknowledging increased uncertainty in the global trade environment.

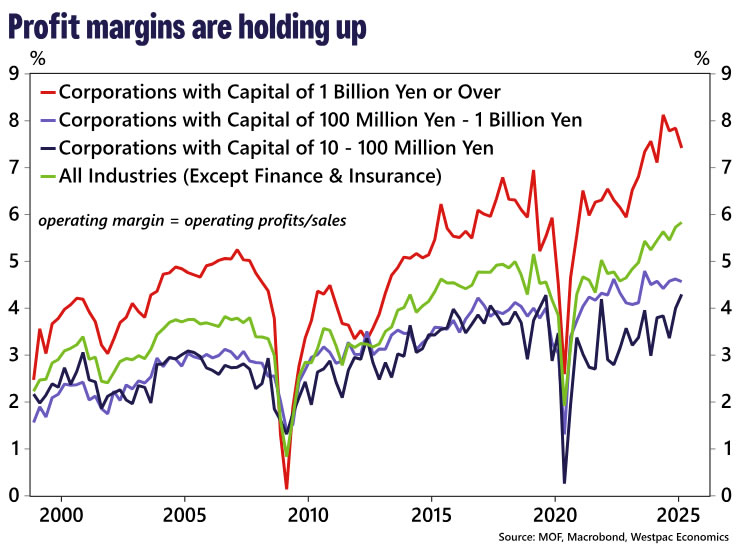

Through the remainder of FY2025, a tight labour market, alongside elevated profits, are expected to support wage gains, though the Outlook noted that “the growth rate is likely to decelerate somewhat, affected by the decline in corporate profits.” The outlook for business investment is expected to be similar, with profits still supporting critical investment, although the pace of investment is expected to “decelerate”. Beyond FY2025, strengthening profits are anticipated to support both wage and investment growth.

The next rate hike occurring in March 2026 remains our base case, following the outcome of the annual spring wage negotiations. The recent inflation upgrade was supply-driven and therefore does not alter the BoJ’s cautious stance on policy. In our view, the BoJ’s policy reaction function instead remains focused on demand-side dynamics.

That said, the BoJ has signalled that, if incoming data aligns with its projections, they will continue raising rates. If they gain sufficient confidence ahead of March, there is a risk that the next rate hike could come sooner, most likely in January 2026.

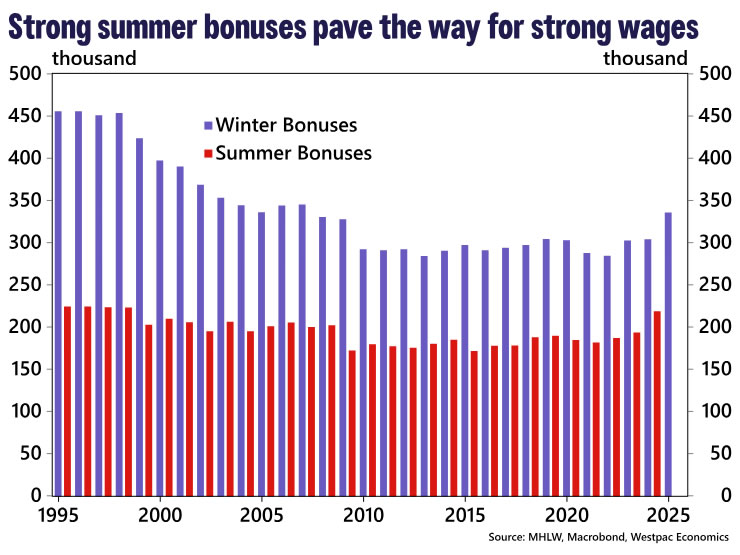

We will be paying close attention to summer bonuses data (due late August). If it prints in line with last year, it will suggest firms have both the capacity and willingness to lift wages heading into the spring wage round. This will be assessed alongside the Q2 Financial Statement data, which will provide a more accurate picture of firms’ underlying profitability. If Q2 earnings hold up, it would bolster the BoJ’s confidence that wage growth is sustainable, reinforcing the case for an earlier tightening step.

{kind=link}