Asia Market Wrap – Asian Stocks Advance

Asian stocks advanced as tech stocks continue to drive the rally. It seems the deal between Advanced Micro Devices and OpenAI gave investors a boost.

The MSCI Asian‑Pacific Index was up about 0.3 percent, touching a record level. Japanese shares kept climbing, while worldwide markets also nudged toward peaks. Yet worries about a US government shutdown and turmoil in France seemed to push some people toward safe assets. Gold and Bitcoin both hit fresh highs. A sign that concerns still linger?

Tech firms still anchor the global rise. The AMD‑OpenAI partnership could be another data‑center project this year. It follows Nvidia’s earlier promise to spend up to $100 billion on OpenAI, a move that appears aimed at meeting growing AI demand.

European Session – Shell Jumps as Energy Shares Gain

European stock markets were mostly unchanged on Tuesday, as losses in the industrial and healthcare sectors were balanced out by gains in energy companies and luxury stocks.

The main STOXX 600 index was steady at 570.2 points. French stocks also stabilized after their sharp drop yesterday following the sudden resignation of the Prime Minister. The outgoing Prime Minister is holding final talks with political parties today and tomorrow.

On the downside:

Healthcare stocks fell 0.6%, with major companies like Germany’s Bayer and Denmark’s Novo Nordisk both dropping around 2%.

Top defense companies, including Rheinmetall and BAE Systems, also lost about 1%.

Helping to support the market:

Oil and gas stocks were boosted, rising 1.9%. Energy giant Shell saw its shares climb after it predicted higher production and better trading results for liquefied natural gas in the third quarter.

Luxury goods companies LVMH and Kering saw their shares rise by 1.8% and 2.2% respectively, after Morgan Stanley upgraded its rating on them.

In company news, discount retailer B&M fell sharply by about 15% after predicting a 28% drop in its core earnings for the first half of the year, leading to a forecast of lower annual profit.

Shares of the major oil company Shell rose 1.9% to 2790.5 pence, making it the second-biggest gainer on the FTSE 100. The company announced several updates. The company raised its forecast for the third quarter’s production of Liquefied Natural Gas (LNG) to between 7.0 and 7.4 million metric tons. It also expects that its trading results for the integrated gas division in the third quarter will be significantly higher than they were in the second quarter.

However, Shell also stated it will take a $600 million financial hit due to the cancellation of its Rotterdam biofuels project. Even with this loss, the company’s stock has performed well this year, having climbed over 10.5% year-to-date as of its last closing price

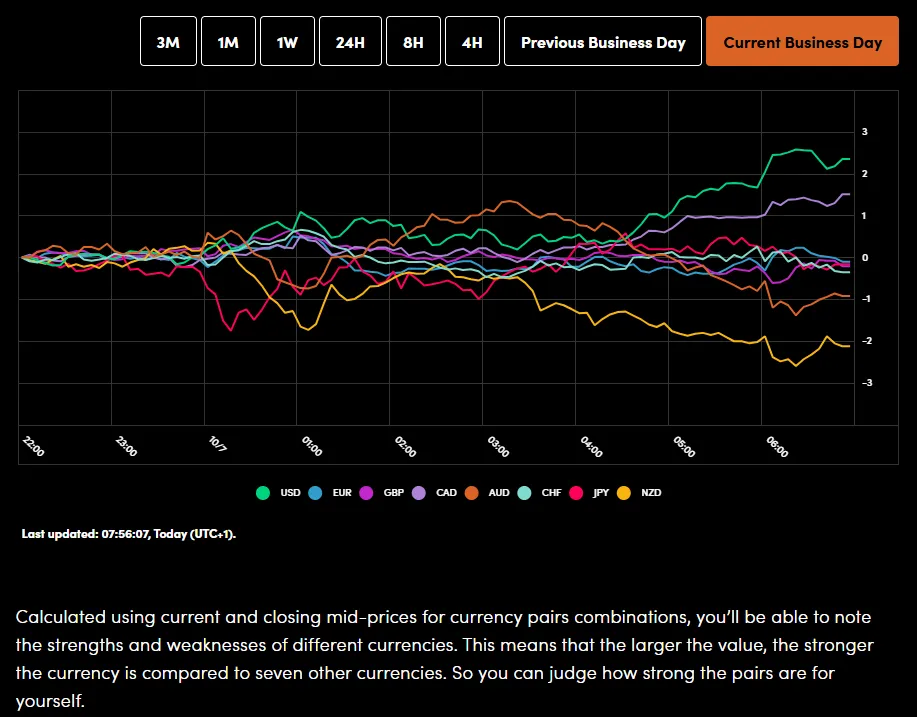

On the FX front, the Japanese yen continued to weaken on Tuesday, falling to its lowest level against the dollar in two months.

The yen slid 0.1% to 150.46 per dollar (after touching a low of 150.62). It also hit a fresh all-time low against the euro at 176.35 before regaining some ground. This move comes as attention in Japan shifts to who the new pro-stimulus party leader, Sanae Takaichi, will name to her government.

Meanwhile, the US dollar index edged up 0.1% to 98.23. The euro slipped 0.1% to trade at 1.1694, extending its losses from the previous day. The British pound also weakened 0.1% to 1.3463.

In commodity currencies, the Australian dollar fell 0.1% to 0.6608, and the New Zealand dollar dropped 0.3% to 0.5822.

In the cryptocurrency market, Bitcoin declined 0.7% to 124,334.94, while Ether rose 0.5% to 4,713.78.

Currency Power Balance

Source: OANDA Labs

Oil prices continued to rise on Tuesday. The rise in Oil prices are largely down to the fact that the OPEC+ group announced a smaller production increase for November than expected, which eased some of the worries about the market having too much supply.

Specifically, Brent crude increased by 0.29% to 65.66 a barrel, and US West Texas Intermediate (WTI) crude climbed 0.31% to reach 61.88 a barrel.

For more on the OPEC + output hike and Oil prices, read OPEC + Delivers Modest Output Hike, Brent Crude Rises 1.7%. What Next for Oil Prices?

Gold prices reached another record high on Tuesday. This surge is due to two main reasons: the ongoing US government shutdown, which shows no sign of ending, and the near certainty that the US Federal Reserve will cut interest rates this month.

Spot gold rose 0.1% to trade at 3,962.63 per ounce, after earlier setting a new all-time high of 3,977.19. US gold futures for December delivery also gained 0.2% to reach $3,985.30.

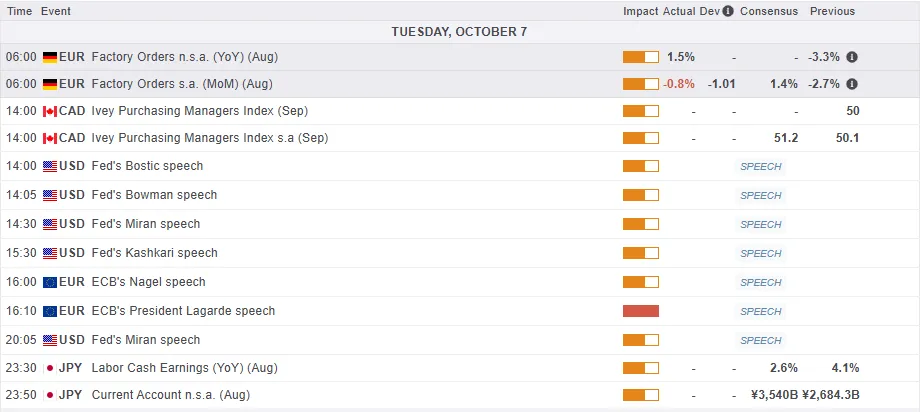

Economic Calendar and Final Thoughts

Looking at the economic calendar, it is a rather quiet day from a data perspective for both the US and European sessions.

The day will be dominated by a host of Central Bank speakers with ECB President Christine Lagarde and the Feds Stephen Miran’s comments likely to get the most attention.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day – DAX Index

From a technical standpoint, the DAX index has pulled back to the top of the channel it broke out of last week.

This sets the index up for a potential 900 point rally to the upside.

Given that global equities have started the week on the front foot, European equities are lagging which could bode well for the DAX if price can hold above the 24200 level in the early part of the week.

Yesterday we saw a hammer candlestick close on the daily timeframe which does support further upside. However, this morning we are seeing a pullback in the DAX which may present a better risk-to-reward opportunity for would be longs.

Immediate upside resistance for now rests at 24500 before the 24665 swing high from July 10 comes into focus.

A move to the downside will face support at 24200 before the confluence area around 24000 comes into focus.

DAX Index Daily Chart, October 7. 2025

Source: TradingView.com (click to enlarge)

. It also hit a fresh all-time low against the euro at 176.35 before regaining some ground. This move comes as attention in Japan shifts to who the new pro-stimulus party leader, Sanae Takaichi, will name to her government.){kind=link}