{kind=link}

Log in to today’s North American session Market wrap for November 11.

Many traders were off during today’s session as the world celebrates the 108th birthday of the resolution of World War I

Nevertheless, US stocks and cryptocurrencies were open, allowing for significant rotation towards more defensive sectors and assets.

Initial fears of Critical mineral export controls scaring participants subsided after China announced a one-year temporary suspension of export controls on rare earths, lithium battery materials, and other key metals.

However, the market quickly pivoted to domestic concerns.

The catalyst for the downside was a weekly ADP private employment report, a new series providing a high-frequency look at the labor market.

This weekly pulse offered a view contrary to the October monthly report (which saw a gain of 42K jobs): the latest numbers indicate that private employers reduced an average of 11,250 jobs a week over the past four weeks.

This suggests that recent strength observed could be already a thing of the past.

This bad employment news immediately drove further downside in Tech and AI-linked shares, with the Nasdaq Composite struggling and closing 0.3% lower – Nvidia lost close to 3% today.

Conversely, the Dow Jones Industrial Average appreciated, rising 1.2% to close at a new record high as money rotated towards more defensive, health care and energy-related sectors, a clear rebalancing away from high-beta tech.

Remember to take today’s trading with a pinch of salt as volumes were much lower than the usual.

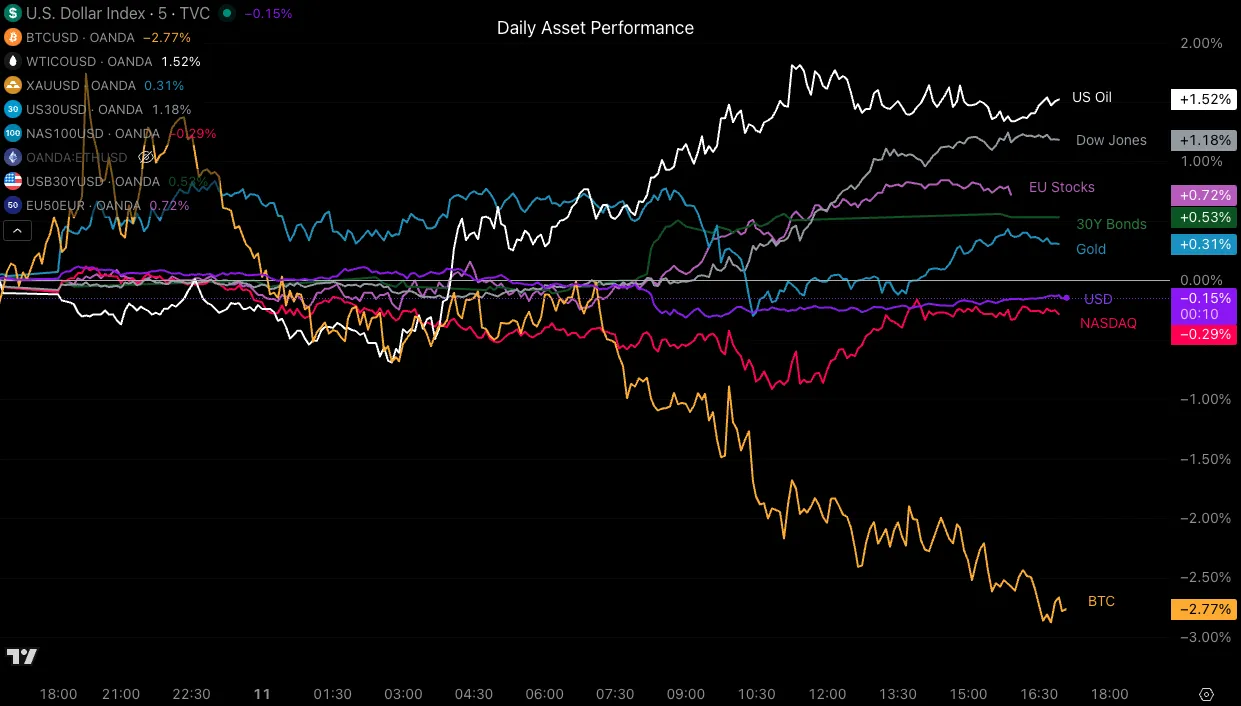

Cross-Assets Daily Performance

Cross-Asset Daily Performance, November 11, 2025 – Source: TradingView

Two noticeable patterns appeared today: One with the rotation happening from tech to defensive sectors which will be one to keep an eye on looking forwards.

The second being Oil and Nat Gas prices, which have began to take off in today’s session amid the geopolitical turmoil happening with Russian oil purchases and much else.

(To learn more, I invite you to check out our recent Oil analysis)

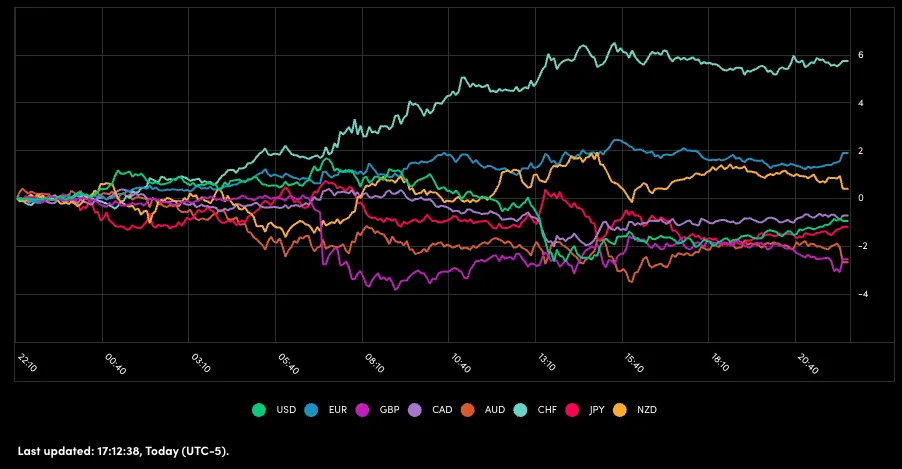

A picture of today’s performance for major currencies

Currency Performance, November 11 – Source: OANDA Labs

The Swissie really demarcated itself today with the ongoing US-Switzerland tariff talks.

For the rest, balanced price action took out some steam off of the more risk-on antipodean currencies. Keep in mind that volumes were heavily subdued.

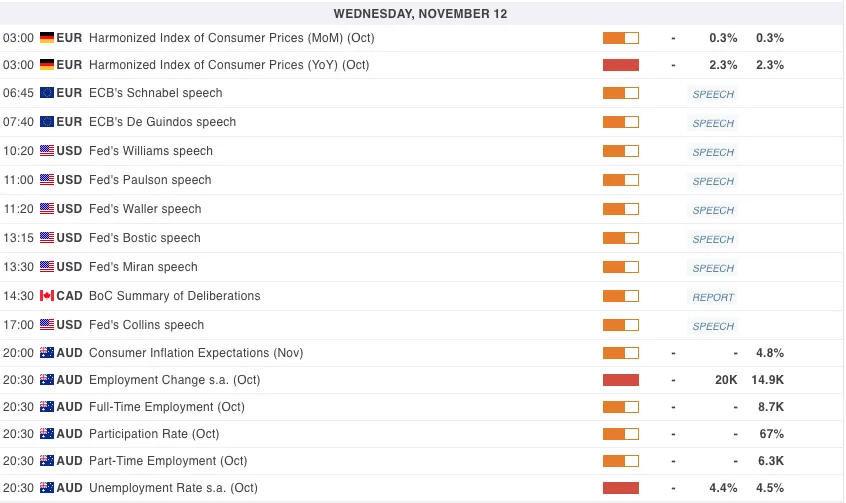

A look at Economic data releasing throughout tonight and tomorrow’s sessions

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

Wednesday will be data-heavy from Europe through Asia-Pacific, offering several directional drivers.

Early in the day, Germany’s CPI will confirm inflation holding steady (+0.3% MoM, +2.3% YoY), keeping the ECB on pause but watchful – Several ECB officials (Schnabel, De Guindos) will be speaking afterward.

The USD session features a full Fed speaker lineup — Williams, Waller, Bostic, and Collins — which will be interesting after the consecutive dovish employment reports.

Late in the global day, attention turns to the Australian jobs report, where markets expect +20K new positions and an unemployment rate steady at 4.5%.

Any miss here could strengthen bets for earlier RBA easing, especially if Inflation Expectations (4.8%) show further moderation.

The Bank of Canada’s Summary of Deliberations also lands mid-session, offering deeper insight into its latest policy hesitation.

Safe Trades!