{kind=link}

The Bank of Canada delivered a well-telegraphed, widely-expected hold today, keeping the overnight rate at 2.25%—the bottom of the neutral range and where we expect it will remain through the end of 2026.

The decision was after upward GDP revisions in the Q3 GDP release dating back to 2022, and a string of positive labour market surprises that saw a key indicator of the output gap, the Canadian unemployment rate, drop from 7.1% in September to 6.5% in November.

As much as recent data has been encouraging, we see it as reaffirming our cautiously optimistic base case rather than a fundamental shift in the Canadian economic outlook, and continue to expect a gradual recovery in the economy and labour market supported by the 275 bp rate reduction from the BoC since June 2024.

That outlook broadly aligns with the BoC’s. Governor Macklem said in the press conference to expect modest growth and slow absorption of economic slack, while reiterating its holding bias.

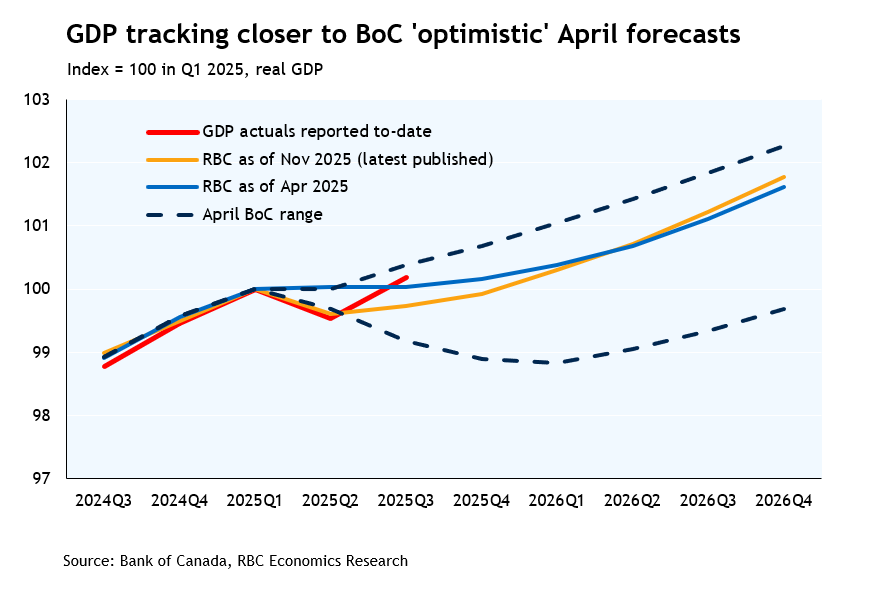

Looking back, Canadian economic growth has already tracked toward the more optimistic end of the range of possibilities that the BoC projected in April, thanks to a combination of CUSMA exemptions shielding the bulk of goods exports to the U.S., and underlying resilience in household spending.

With that, we think the BoC is done with rate cuts, and that the next change in interest rates is more likely to be a hike. Our base case assumes this won’t occur until 2027, but risks are tilted toward an earlier move.

What are the risks that could lead inflation to deviate from 2%?

BoC’s assessment that today’s policy rate is “at the right level” rests on a key assumption that “ongoing economic slack to roughly offset cost pressures associated with the reconfiguration of trade”, leaving inflation tracking around the 2% target.

We agree with that assessment, but have also argued that robust consumer demand growth could keep underlying price pressures elevated next year.

By most measures, the economy still has excess supply—it can produce more than is currently demanded. This creates downward pressure on inflation as businesses compete for limited demand. Still, recent data already suggests a smaller (albeit still negative) output gap than previously expected.

Consumer purchases have also broadly held onto resilience this year and could remain a source of strength if not upside risks to our growth and inflation forecast in 2026, following improvements in labour market conditions. That could lessen the disinflationary pressures relative to what was expected.

Offsetting that is the cost of “trade reconfiguration”—Canadian producers are not directly paying tariffs, but still face cost increases for managing trade complications, investing in alternative sources or partners, and absorbing higher prices from U.S. counterparts through integrated supply chains.

On both fronts, we see risks mostly tilted towards more inflationary pressures, not less. If either of those risks were to materialize more tangibly, risks of BoC rate hikes as early as H2 2026 rise.