policymakers are set to raise rates 25 bps this week, a now consensus view but a stance we took well before financial markets fully priced tighter BoJ monetary policy. Markets fully digesting a BoJ December rate hike likely means the Japanese yen will fall short of hitting our YE-2025 USDJPY target; however, no element of surprise also means emerging market currencies should be more protected and not experience much post-hike volatility, a different dynamic relative to last year's BoJ August hike that injected volatility across many high-yielding emerging currencies as the yen funded carry trade unwound.){kind=link}

Summary

Bank of Japan (BoJ) policymakers are set to raise rates 25 bps this week, a now consensus view but a stance we took well before financial markets fully priced tighter BoJ monetary policy. Markets fully digesting a BoJ December rate hike likely means the Japanese yen will fall short of hitting our YE-2025 USDJPY target; however, no element of surprise also means emerging market currencies should be more protected and not experience much post-hike volatility, a different dynamic relative to last year’s BoJ August hike that injected volatility across many high-yielding emerging currencies as the yen funded carry trade unwound.

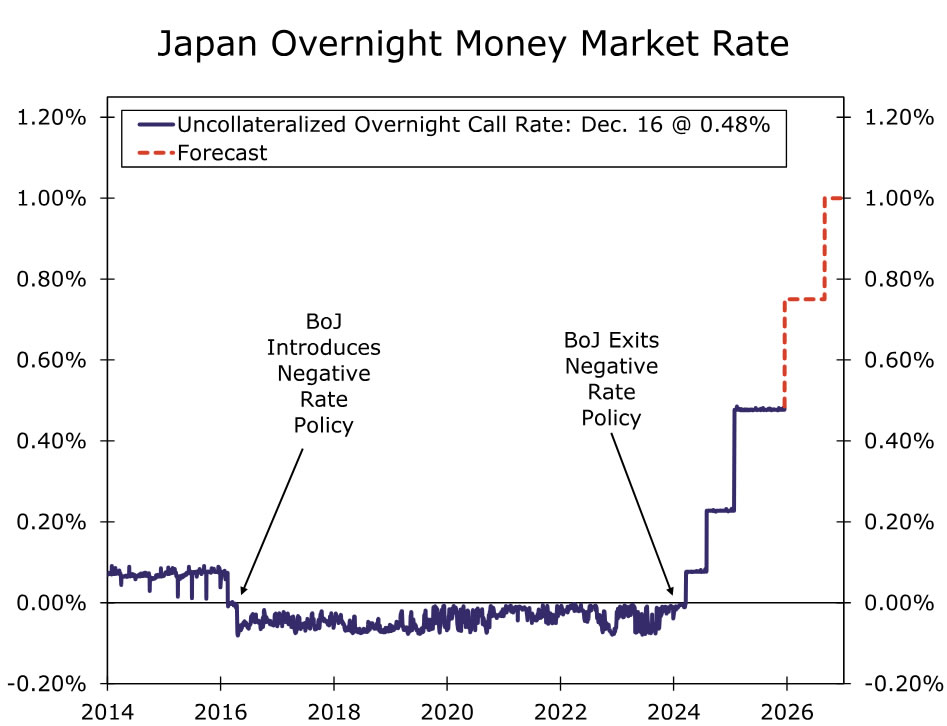

Looking ahead, even before we hear from BoJ policymakers on the outlook for monetary policy, we are adjusting our BoJ forecast profile to now include another 25 bps rate hike in Q3-2026. Financial markets are priced for the BoJ to deliver a rate hike closer to the end of next year, which puts our updated BoJ outlook moderately out of consensus on the more hawkish side. Our revised view leads us to believe the yen may be more resilient in H2-2026 than we originally forecast on diverging paths for BoJ-Fed monetary policy.

Bank of Japan Preview

Bank of Japan (BoJ) policymakers will make their final monetary policy decision of 2025 at the end of this week, and we—alongside the broader consensus—expect a 25 bps rate hike to be delivered. We have been steadfast in our view that the BoJ would raise rates this week, a forecast we highlighted in our 2026 Annual Economic Outlook well before financial markets fully priced a December rate hike. Our rationale for a hike came down to our assessment of underlying economic fundamentals in Japan which—despite political preference for easier monetary policy after Prime Minister Takaichi’s election earlier this year—we felt were consistent with tighter BoJ monetary policy. Since we published our year ahead outlook, economic fundamentals, in our view, have become more consistent with higher interest rates. This conviction stems from wage hikes that are above the current pace of inflation, fiscal stimulus deployed by the Takaichi administration and leading indicators that suggest activity is still firm. Adding to our conviction is a Japanese yen that has broadly remained on the defensive and has not participated in the dollar depreciation trend as much as peer G10 currencies.

Going forward, we do not believe that Japanese economic conditions are set to change all that materially. Meaning, we expect the Japanese economy to remain supported, and while GDP growth will not be all that exciting in 2026, we expect activity to continue to be consistent with an economy that can digest higher interest rates. On inflation, headline CPI may slip back toward the BoJ’s target next year; however, wage hikes, fiscal stimulus and the lagged effect of U.S. imposed tariffs keep the balance of risk tilted to the upside. Taken together, resilient growth and upside risks to inflation, we are revising our Bank of Japan forecast profile to now include another 25 bps rate hike to be delivered Q3-2026 (Figure 1). As of now, financial markets are priced for additional BoJ tightening in Q4-2026, leaving our view moderately out of consensus and more hawkish relative to peer economists. Similar to the upcoming December hike, local political dynamics will remain the biggest hurdle to additional tightening. But if local economic conditions evolve as we expect in 2026, we have our doubts that political preference or interference will prevent BoJ policymakers from taking the BoJ Target Rate to 1.00% by the end of next year.

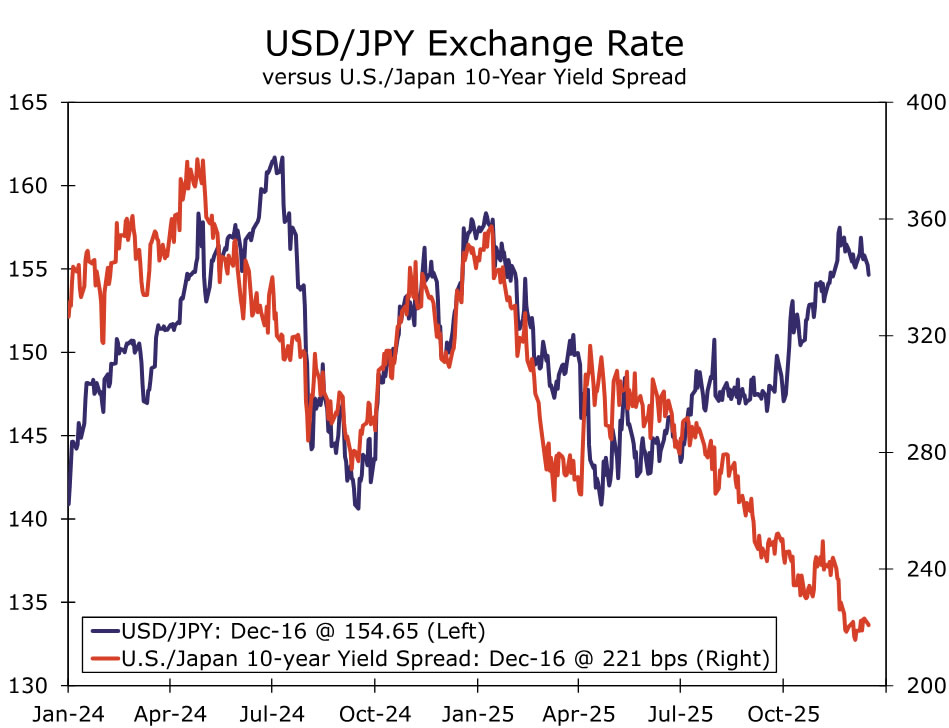

Should the BoJ move ahead with a hike this week, the yen may not strengthen the way we outlined in our 2026 outlook, at least not in the near-term. When we published our 2026 outlook, our BoJ December hike forecast was very much out of consensus, and we believed the rate hike would be more of a surprise that would prompt a sharp JPY rally headed into the end of the year. But as mentioned, with a hike almost fully priced, near-term upside for the Japanese yen is likely limited. Or said another way, for JPY to strengthen in line with our forecast, an exogenous catalyst would need to materialize. Rather than a USDJPY move lower toward our original Q4-2025 target of JPY152.00, USDJPY is likely to hover around current levels through the end of this year. Also, with financial markets expecting a BoJ December rate hike, volatility across emerging market currencies, similar to what unfolded after the BoJ raised interest rates in August 2024, is unlikely. Carry positions funded by Japanese yen have been scaled back as other funding currencies (i.e., CHF) have become associated with less hawkish central banks, and in turn, have become more popular alternatives. Positioning data suggests leveraged funds are also net long JPY, additional evidence that EM currencies should be more protected in the upcoming BoJ hike. More medium-term, the Japanese yen could be more resilient than we initially expected. An earlier rate hike in 2026 than markets are pricing should be supportive of the yen, especially when considering USDJPY has been disconnected from U.S. Treasury and Japanese Government Bond yield differentials over the back half of 2025 (Figure 2). We still believe the U.S. dollar will be in rebound mode when the BoJ delivers its hike in 2026, but against a backdrop of major central banks keeping monetary policy settings on hold by H2-2026, BoJ rate hikes should prevent USDJPY from rising as much as initially expected over the back half of next year.