{kind=link}

Summary

Events in Venezuela are top of mind for market participants, and while developments are associated with an elevated degree of uncertainty, we are not making any changes to our markets or economic forecasts as a result of the deposition of Nicolás Maduro. The geopolitics may prove to be the most interesting aspect of U.S. intervention in Venezuela as fragmentation may be exacerbated and countries may shift strategic alignments to demonstrate support or opposition to the U.S. operation. We also believe Latin America’s shift toward conservative political platforms will remain intact as Venezuela is unique in many ways; however, similar deposition-style actions in select countries could reverse the recent trend of softening regional political risk.

We do not believe the U.S. deposition of Nicolás Maduro will act as a catalyst to disrupt global or Latin American financial markets nor oil prices. Events in Venezuela this past weekend are top of mind for market participants, especially those with exposure to Latin America and oil. While the situation is very much riddled with uncertainty—particularly in regard to what the political regime in Venezuela will look like near term and who ultimately shapes the longer-term Venezuelan government (i.e., democratically held free and fair election, extended U.S. occupation, U.S. installed administration etc.)—we struggle to see how, as the situation currently stands, financial markets and oil prices are materially affected in the immediate term.

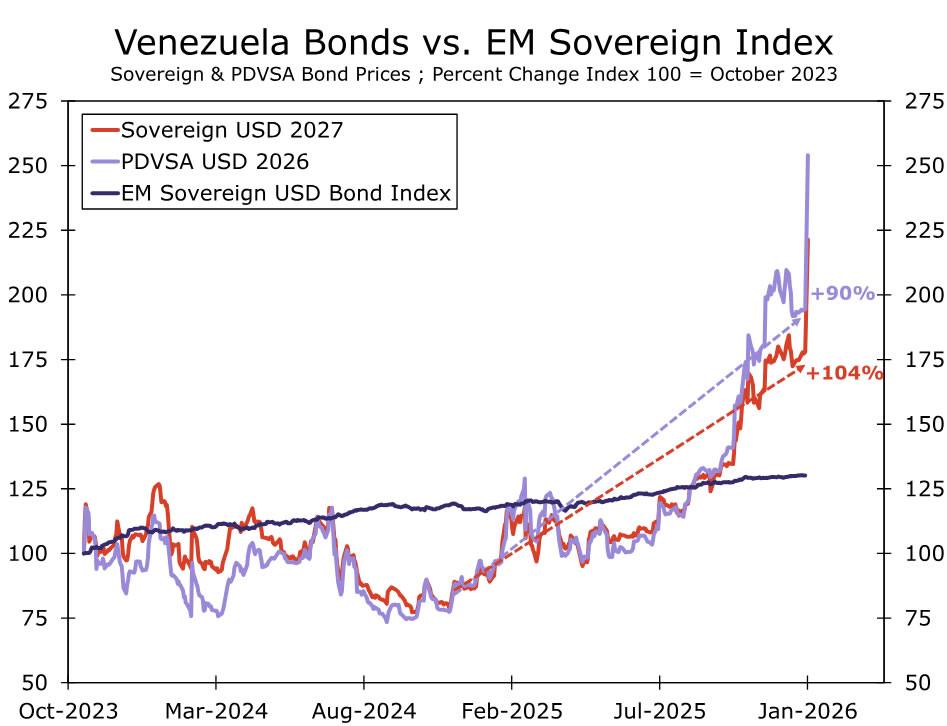

Venezuelan sovereign and PDVSA debt, both of which are currently in default, have been some of the best performing assets since the Trump administration took office in January 2025, essentially doubling in value over the past 12 months (Figure 1). Just about all EM assets rallied last year, but the degree of Venezuelan asset outperformance, in our view, stems from market participants pricing a rising degree of confidence in a Venezuela regime change scenario. This confidence seemingly grew as U.S. military activity in the region picked up pace late last year. The significant outperformance in Venezuela asset prices suggest market participants were unlikely to be caught off guard that a regime change scenario is now in motion, even if this scenario is in infant stages and the future remains far from certain.

In that sense, as things currently stand, we do not envisage material nor long-lasting financial market disruptions on the basis that markets may have been prepared for political turnover in Venezuela. This theory extends to macro asset classes across EM and Latin America, as well as oil prices, and we will not be making adjustments to any of our markets-related or global economic forecasts due to recent developments in Venezuela.

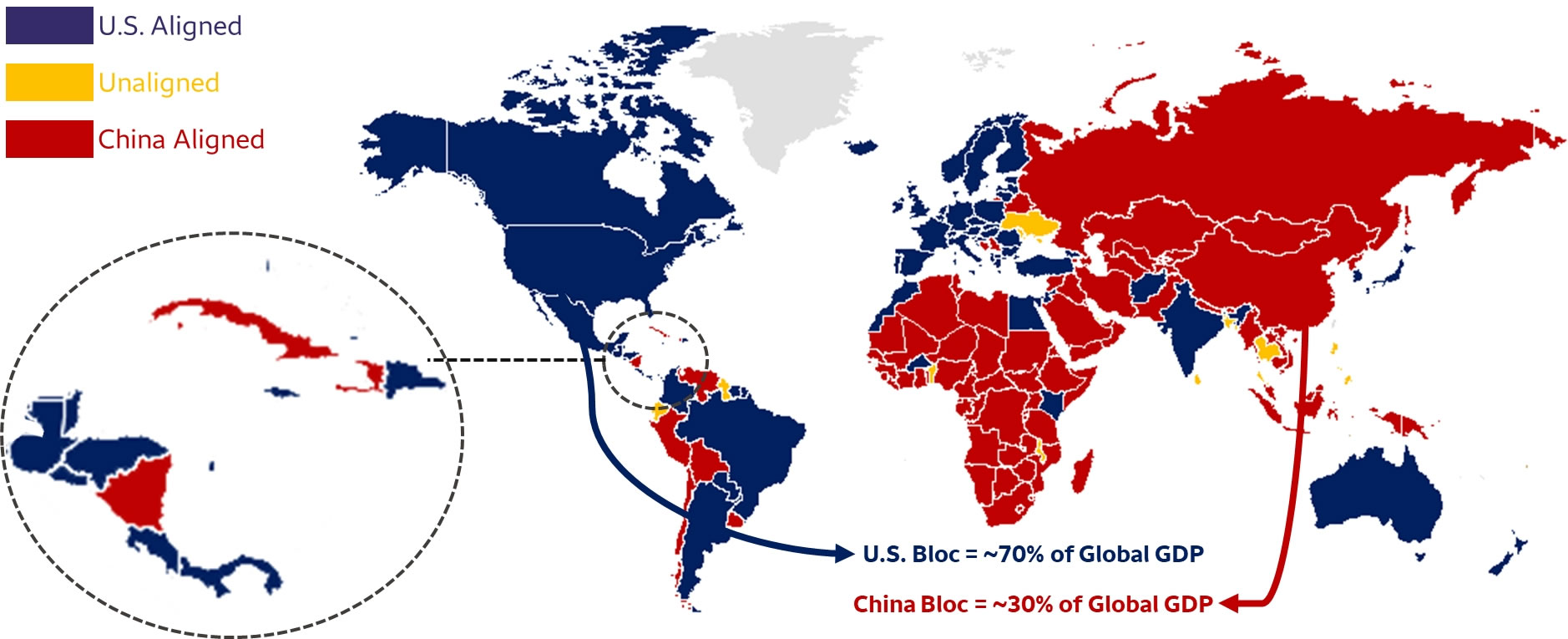

The geopolitical implications are just as paramount, if not more. An era of global fragmentation, heightened U.S.-China competition and a more interventionist approach to foreign affairs from the Trump administration all add a layer of geopolitical complexity to U.S.-Venezuela developments. From a geopolitical perspective, the U.S.-led deposition of Maduro should exacerbate the fragmenting of the global economy and also drive deeper wedges, and perhaps new alignments, across Latin America. We have argued that sovereign stances on geopolitical developments are a driving force of the global economy fracturing into distinct geopolitical and economic blocs: one led by the U.S. and another by China. Initial responses from the highest levels of foreign government seem to demonstrate clear divergences in the level of opposition or support for Maduro’s forced exit, particularly across Latin America.

According to our fragmentation framework, Latin American nations are already split between strategic alignment with the U.S. or opting for an alliance with China (Figure 2). In our view, the U.S.-led deposition of Maduro will likely deepen those fissures and ingrain strategic alliances even more (e.g., Argentina digs in behind the U.S., Nicaragua remains unequivocally aligned with China). Perhaps more interesting is the idea that select countries may flip their strategic alliance away from the U.S. and toward China, and vice versa. Candidates to flip toward China are Colombia and Brazil, which have already encountered new tensions with the U.S. during the past 12 months, but have also seen President Petro and President Lula strongly condemn U.S. actions in Venezuela. On the other hand, Chile currently screens as aligned with China; however, president-elect Kast has exhibited strong words of support for deposing Maduro. Over time, Chile’s alignment with the U.S. on Venezuela, and perhaps other notable geopolitical events going forward over the course of the Kast administration, could flip Chile into the U.S. bloc.

We believe it is worth noting, regardless of how countries align and how those alignments change, that the global economy likely will still experiences negative consequences of fragmentation and the forming of blocs. The magnitude of the negative impact will be determined by which countries are aligned, but in the aggregate, slower global GDP growth is a product of a fracturing global economy.

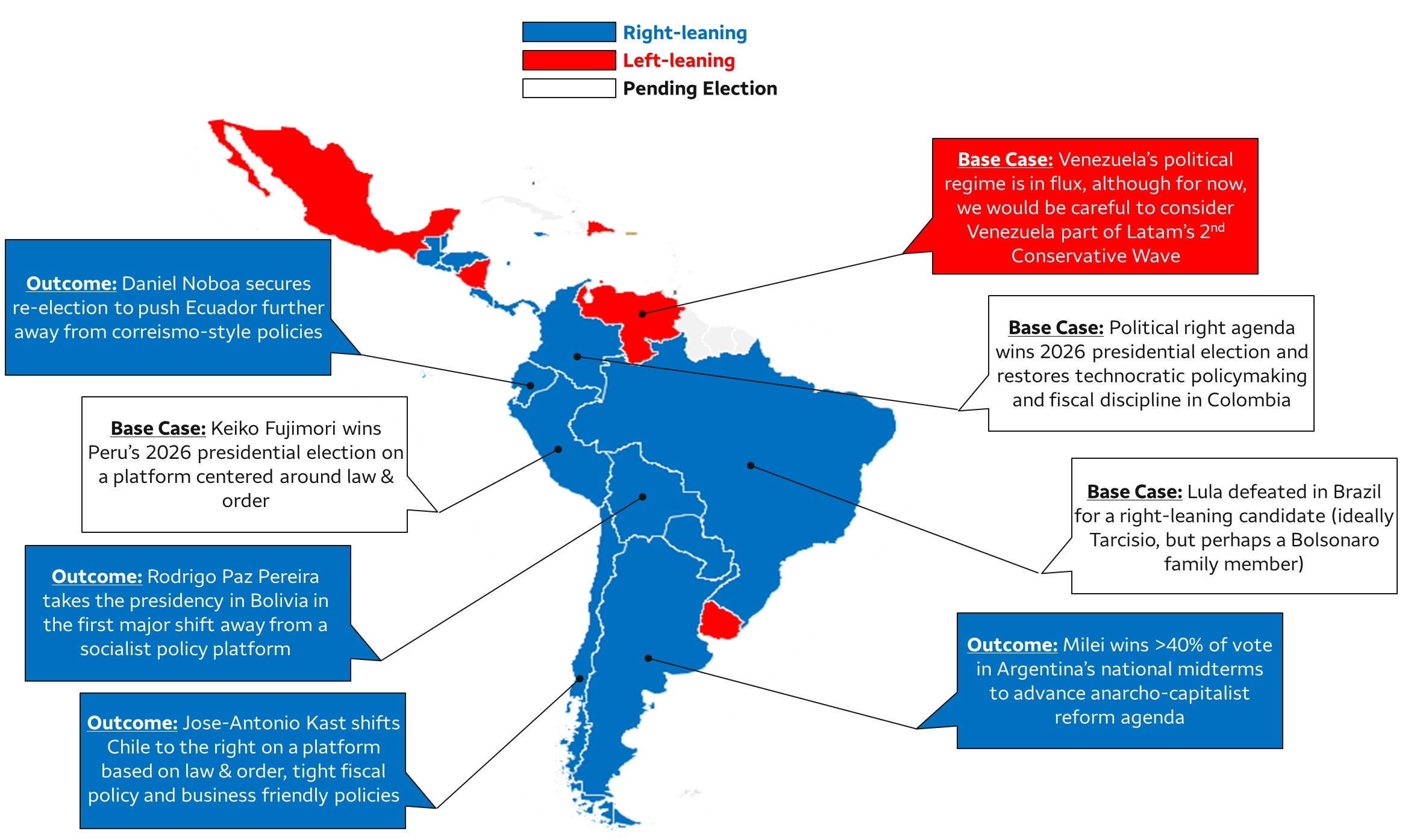

Latin America’s broad decline in regional political risk should be uninterrupted? Over the past 12-18 months, general and congressional elections across Latin America have yielded broad support for right-leaning political platforms. This trend has been on display in traditional left-leaning strongholds such as Ecuador, Bolivia and Argentina, and most recently in Chile and Honduras where conservative politicians won their respective general elections. We have noted in multiple publications (See: Unwinding the Tide. Latin America’s Shift to the Political Right 6/11/2025, Latin America Elections Outlook 8/1/2025, Latin America Elections Outlook. The Shift to the Political Right is in Motion 11/7/2025) how Latin America is in the midst of a second “Conservative Wave” and how regional political risk is set to decline as a result of these latest election trends (Figure 3). In our view, while Venezuela-related uncertainty will likely linger for an extended period of time, the softening in political risk associated with Latin America is likely to continue going forward.

That is not to say Venezuela will also adopt a right-leaning political platform at some point, but more a way of saying that events in Venezuela are idiosyncratic and unique and, similar to our view on how Venezuela-related events should have little impact on broader financial markets, we do not see Venezuela as disrupting the overall improvement in the political risk environment across Latin America. We believe this would be true even if Venezuela fell into a domestic power struggle situation that resulted in a prolonged U.S. occupation or no functioning government.

For us, the bigger risk for the regional political risk environment would be similar deposition-style actions toward countries in the region that are unaligned with the U.S. (i.e., Cuba and Nicaragua) and/or if the U.S. administration pursues counter-narcotics or oil incentivized activity in more systemically important regional countries such as Colombia and Mexico. We will not speculate on U.S. actions, but we would note that Venezuela is unique in the sense that geopolitical and political philosophy of the Maduro administration ran counter to that of the U.S., Venezuela has been aligned with China closely for decades, it has been suspected of being involved in the illegal flow of narcotics to the U.S. and it has the largest proven oil reserves in the world. While other regional nations may have some similarities to Venezuela, finding an exact comparable is a challenge. So, while we expect the broader political risk environment to remain on an improving trajectory, risks around this newfound stability exist.