report will be the definitive barometer for whether the Federal Reserve’s recent easing cycle was a masterstroke or a premature reaction to a cooling labor market.){kind=link}

The first major economic release of 2026 arrives this Friday, January 9, at 8:30 AM ET. Following a year of significant volatility marked by a federal government shutdown and a series of interest rate cuts, this Non-Farm Payrolls (NFP) report will be the definitive barometer for whether the Federal Reserve’s recent easing cycle was a masterstroke or a premature reaction to a cooling labor market.

Risks Heading into the Release

The primary risk remains data noise. Residual effects from the late-2025 government shutdown continue to cloud the “true” hiring trend. Additionally, significant downward revisions to October and November figures could overshadow a decent December headline, painting a bleaker picture of the quarter’s momentum.

Market participants are also wary of a potential “January Effect,” where rebalancing and new-year optimism collide with high-stakes data.

Lastly there is the growing pressure on Jerome Powell in what will be one of his last meetings as Fed Chair. Comments from Stephen Miran on Thursday may be a sign of what Powell’s successor would bring as they would be appointees of the current administration.

Miran said he is looking at 150 bps of rate cuts through 2026, to boost the labor market. That is quite a stark contrast to what the Fed is currently pricing.

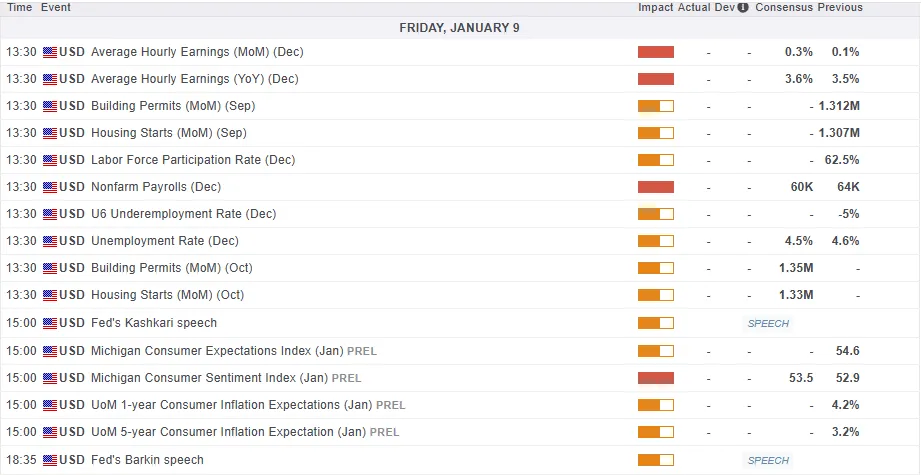

The Consensus: A Moderate Recovery

Economists are forecasting a modest rebound in hiring after months of data distortions. The consensus for December’s NFP sits at approximately 60,000 to 70,000 new jobs. This follows a November print of 64,000 and a catastrophic, shutdown-skewed October that saw over 100,000 jobs temporarily erased.

While the headline hiring remains below historical norms of 100k+, the unemployment rate is expected to edge down to 4.5% (from 4.6%).

This slight drop is largely attributed to furloughed federal workers returning to payrolls and a low rounding threshold in the household survey.

Meanwhile, Average Hourly Earnings (AHE) are forecast to rise 0.3% MoM (3.6% YoY), a level the Fed considers consistent with its long-term inflation goals.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Deviation from the Consensus: What It Means

The Hawkish Beat (85k+): A surprise to the upside would suggest the labor market is far more resilient than the Fed’s recent 75bps of cuts implied. This would likely ignite a “good news is bad news” reaction, as traders would be forced to price out a March rate cut, fearing the Fed may have to pause or even reverse course to combat “sticky” inflation.

The Dovish Miss (<50k): A sub-50k print would confirm fears of a “material” weakening in labor demand. This would validate the market’s current pricing for at least two more cuts in 2026, reinforcing the narrative that the US is in a late-cycle expansion vulnerable to recession.

Potential implications for the US Dollar Index (DXY) & Nasdaq 100

The market’s reaction to the NFP report will not be uniform, but rather dependent on the deviation from consensus forecasts. These are the potential reactions we could see depending on how the data comes out and is received.

The DXY is currently technically oversold and trades near key support levels. This creates an asymmetric upside risk. Because the market is already heavily positioned for a dovish Fed, a stronger-than-expected report (above 75k) could trigger a violent short-covering rally, driving the DXY back toward the 100 level. Only a significantly weak report would have the power to push the dollar toward fresh multi-year lows.

US Dollar Index (DXY) Daily Chart, January 9, 2026

Source: TradingView (click to enlarge)

The tech-heavy Nasdaq 100 index enters this release on a knife’s edge. If the report hits the “Goldilocks” zone (moderate hiring with cooling wages), the Nasdaq could rally on the promise of continued Fed support. However, a strong NFP would likely spike yields, putting immediate pressure on high-valuation growth stocks. Conversely, a deep miss might initially support stocks via lower yields, but could quickly sour into a “growth scare” sell-off.

Nasdaq 100 Four-Chart, January 9, 2025

Source: TradingView (click to enlarge)

Outlook Moving Forward

If Friday’s data confirms that hiring has bottomed out, the Fed may find its “soft landing.” However, if the 3-month average continues to slide, the pressure on Jerome Powell and his potential successor to provide more aggressive liquidity will become the dominant market theme for the remainder of the quarter.