{kind=link}

Canadian Highlights

- The housing data offered mixed signals this week. Housing starts came in above the recent trend, while existing home sales declined for the second straight month in December.

- Canada reached a trade deal with China, agreeing to admit up to 49k electric vehicles into the domestic market in exchange for a reduction on of tariffs on canola and other products.

- The two countries also signed an “agreement to collaborate in energy, clean technology and climate competitiveness”. Canada has now struck a more open stance to investment from China in the energy sector.

U.S. Highlights

- Headline retail sales rebounded in November from October’s decline. Sales in the control group rose for the second month in a row, pointing to resilience in consumer spending.

- The housing market finished last year on a firmer footing. Existing home sales have now risen for four consecutive months, reaching the highest since early 2023 in December.

- CPI inflation was steady in December at 2.7% y/y, down from a 3.0% peak in September.

Canada – Canada Makes a Deal with China

In a quiet week for economic data, Canadian market price action was largely driven by external developments. Bond markets remained calm, with yields drifting slightly lower over the week. Equity prices briefly wavered early on, but sentiment improved on optimism around the technology sector. U.S. exceptionalism continued to set the tone, though Canadian equities may see more action as details of the Canada–China trade deal filter through investor expectations.

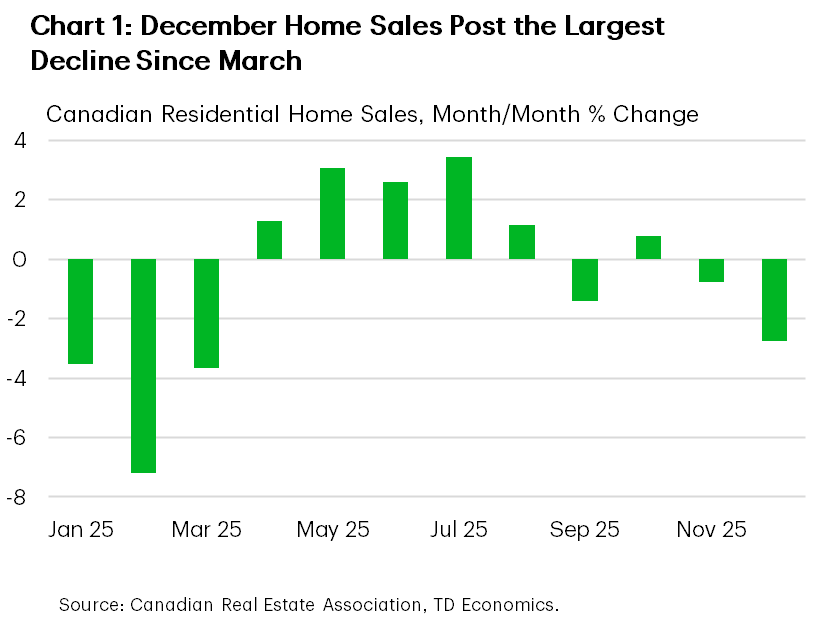

We did get housing market updates for December, with mixed signals from resales versus homebuilding. Housing starts came in above the recent trend, likely reflecting continued momentum in purpose-built rental construction. While this is welcome news, it remains to be seen whether the strength is sustained. Meanwhile, existing home sales declined for the second straight month in December, marking the largest drop since March (Chart 1). Listings also fell, helping ease pressure on prices, with the quality-adjusted home price index now down 4% year-over-year. Our current forecast points to a softer market, reflecting slower population growth, a sluggish economic backdrop, and lingering buyer caution.

Developments on the political front accelerated quickly. The first visit by a Canadian Prime Minister to China since 2017 resulted in a series of agreements on energy, agri-food, and trade. On energy, the countries expressed their intention to strengthen collaboration in energy, clean technology and climate competitiveness. With Canada keen on attracting Chinese investment on renewable energy projects.

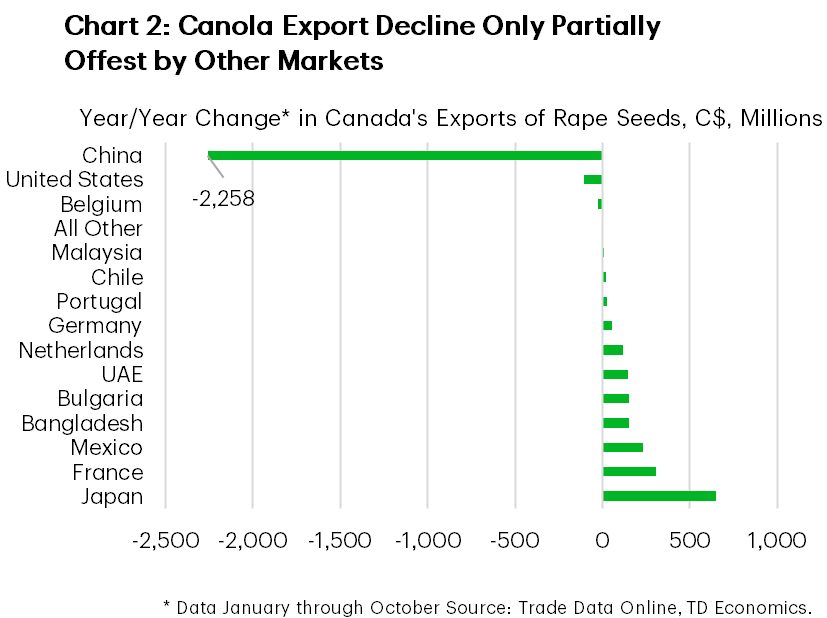

Canada also agreed to admit up to 49k Chinese electric vehicles into the domestic market at a tariff rate of 6.1%, sharply lower than the 100% tariff imposed in 2024. The quota represents roughly 3% of new vehicle sales in Canada, but 30% of EV sales. In return, China will reduce tariffs on Canadian canola seed from roughly 84% to about 15%, while those on canola oil and meal will be eliminated through the end of the year, implying a roughly 12% duty on canola exports overall. Over the past year, Canada’s canola seed exports fell by $2.3 billion, only partially offset by an increase of exports to other countries (Chart 2). With tariff relief on canola and other products, the government expects the deal to unlock nearly C$3 billion in exports.

PM Carney described the outcome as a “preliminary but landmark” agreement, representing a meaningful step toward rebuilding Canada-China economic relations. Further collaboration remains possible, particularly through the Joint Economic and Trade Commission, which is set to meet later this year and will be chaired by trade ministers from both countries. However, the scope for deeper progress may ultimately depend on progress and developments in trade negotiations with the U.S.

Next week brings more economic news. The Bank of Canada’s Business Outlook Survey and inflation data are both out on Monday. Consensus expectations are for inflation to soften on a month-on-month basis, while remaining steady year-on-year. This report is unlikely to move the needle for the Bank of Canada and we expect it to remain on hold for the time being.

U.S. – Economic Resilience Amid Uncertainty

A full economic calendar this week built on last week’s payroll report in underscoring the economy’s resilience through a turbulent fourth quarter marked by the government shutdown. Geopolitical risks escalated amid violent protests in Iran and the prospect of U.S. involvement, sending the VIX index, gold, and oil prices higher mid-week—WTI briefly exceeded $60 per barrel—though prices retreated by week’s end as the threat of direct confrontation diminished. Surprisingly, Fed Chair Powell’s statement Sunday night where he spoke out on threats to the Fed’s ability to set interest rates free from political interference for the first time garnered little reaction from bond markets.

Resilience was evident in the retail sales report, as consumers appeared to have largely shrugged off the effects of the government shutdown. Headline sales rebounded by in November after a flat October, while sales in the control group—used in GDP calculations— were up 1% through the first two months of the quarter. This suggests Q4 2025 consumer spending growth was likely stronger than our earlier 1.1% (annualized) estimate. Next week’s personal income and spending data will provide more detail on households’ November income and spending, especially on services.

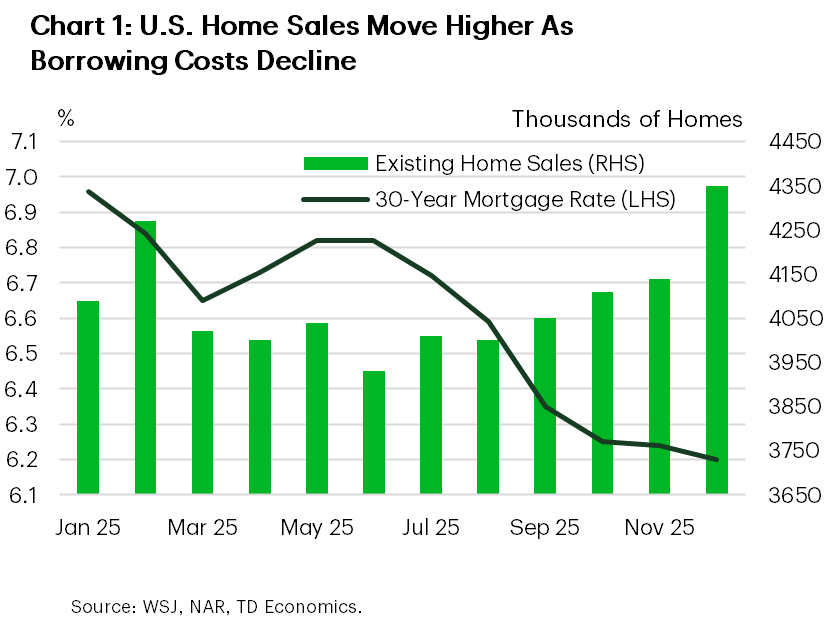

The housing market also finished last year on a firmer footing, with lower mortgage rates drawing more homebuyers off the sidelines (Chart 1). Existing home sales have now risen for four consecutive months, surging 5.1% in December to 4.35 million units—the highest since early 2023. We believe sales will continue to trend gradually higher this year; however, unless addressed, limited supply will continue to impede a stronger rebound.

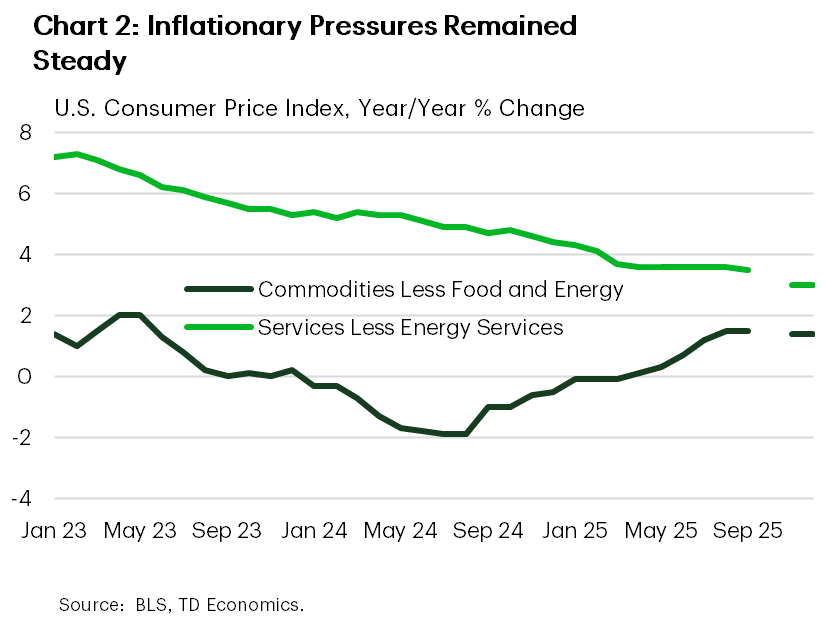

Inflationary pressures remained steady in December. The headline CPI was up 2.7% year-over-year, maintaining its deceleration from the recent high of 3.0% in September. Core goods prices were stable after five consecutive monthly increases (Chart 2). Food prices were somewhat elevated, rising 0.7% month-over-month (up 3.1% year-over-year), remaining a pressure point in households’ budgets.

Although inflation steadied in December, we still expect knock-on effects from tariffs to push it higher in the coming months. FOMC member Williams (voter) expects inflation to “peak at around 2-3/4 to 3 percent during the first half of this year,” but anticipates these will be “one-off” effects. Aside from tariffs, Williams noted that underlying inflation trends have been favourable, supply chain bottlenecks are absent, and the labour market is cooling gradually.

The latest Beige Book also reported both inflation and the labour market as broadly stable, with increased economic activity following the shutdown, and more Fed Districts seeing growth. Overall, recent data gives policymakers more reassurance that the economy stabilized at year-end while price pressures remained contained. This supports a “pause” on rate cuts for a few months, when tariff impacts are more clearly in the rear-view mirror.