{kind=link}

- The Fed is facing increasing political pressure, and a pause in rate cuts has become a tool to defend its institutional independence.

- The labour market remains stable but fragile, supporting a cautious Fed stance despite inflation staying above target.

- Futures markets do not expect further rate cuts in the coming months, with meaningful easing priced in only from mid year.

- The risk of a loss of confidence in the US dollar is rising, potentially leading to a self reinforcing depreciation if the Fed’s credibility is undermined.

The US policy interest rate and core inflation measures in the United States (CPI and PCE year on year), source: Bloomberg

Rising political pressure on the Fed

The Federal Reserve is currently operating in an increasingly tense political environment. Pressure from the administration for further and substantial interest rate cuts has continued to build, turning monetary policy into a political battleground. This conflict recently intensified with legal action being taken against Fed Chair Jerome Powell, widely interpreted as an attempt to exert direct pressure on the central bank’s leadership. Powell’s unusually firm and public response suggests that the Fed is not prepared to yield easily. In this context, a pause in rate cuts can serve not only as a policy decision but also as a visible signal of institutional independence.

Maintaining unity among policymakers will be essential in this phase. That task may prove difficult, given the expected dissenting vote from Governor Miran, who has consistently argued for aggressive rate cuts, and increasingly open signals from Governor Bowman in favour of lower interest rates.

No rate cut at the upcoming meeting

Against this backdrop, the upcoming meeting of the Federal Reserve is very likely to end with interest rates left unchanged. The Fed has for some time signalled its readiness to pause after three consecutive rate cuts implemented in January. This would leave the target range for the federal funds rate at 3.50 to 3.75 per cent. Since the beginning of 2024, rates have been reduced by a total of 175 basis points.

According to Powell and many other policymakers, interest rates are now relatively close to a neutral level. This assessment supports a wait and see approach, allowing the Fed to rely more heavily on incoming data before committing to further policy adjustments.

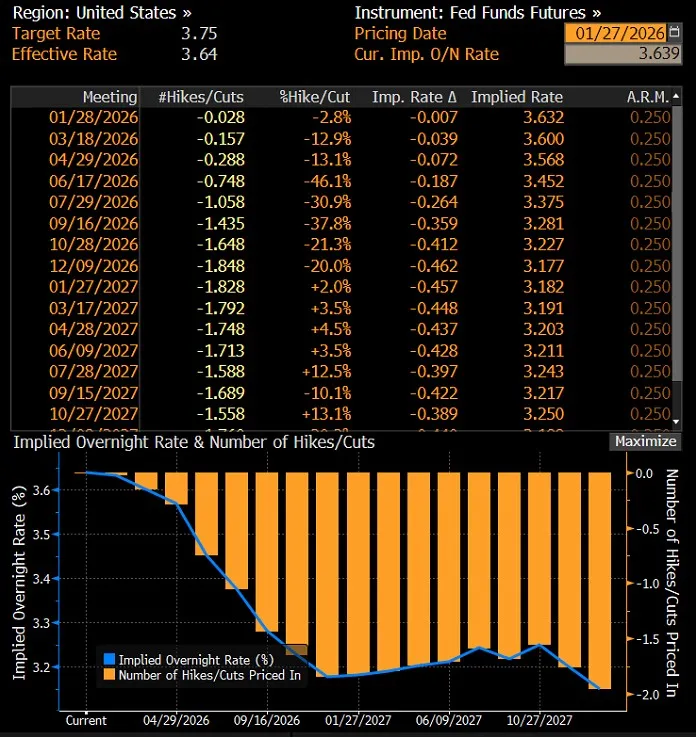

Fed policy expectations priced in by the futures market

The federal funds futures market is also aligned in its assessment of the likelihood of changes to monetary policy parameters at tomorrow’s Fed meeting. Market pricing clearly indicates that the probability of another rate cut in January is very low. The chances of such a move in March and April are also limited. It is only in June that the market begins to see meaningful odds of a further easing of monetary conditions.

Market pricing of the future path of US interest rates, source: Bloomberg

Labour market in the spotlight

The labour market has become a central focus of the Fed’s assessment. Despite solid economic growth last year, employment momentum has clearly weakened. Layoffs in federal agencies have added to this slowdown. At the same time, while private companies have largely avoided large scale redundancies, they have also shown little appetite for new hiring.

This combination has kept the labour market broadly stable, but the balance remains fragile. In the event of an economic slowdown, conditions could deteriorate quickly. Seen from this perspective, the recent rate cuts, despite inflation remaining above the 2 per cent target, can be interpreted as insurance against a sharper downturn rather than a response to immediate weakness.

Recent data offer temporary relief

So far, recent labour market data have not confirmed fears of further deterioration. In both November and December, more than 50,000 new jobs were created each month, which was sufficient to prevent an increase in the unemployment rate. This gives the Fed time to assess whether this trend continues at the start of the new year.

In parallel, more up to date inflation data will become available in the coming months. This includes the release of the PCE deflator, the Fed’s preferred inflation measure, whose publication had been delayed due to last year’s government shutdown. These data will be crucial in shaping expectations for the next phase of monetary policy.

When markets stop believing: the rising risk of a self-reinforcing dollar sell off

The current situation in the foreign exchange market clearly highlights a risk that was repeatedly flagged already last year. This risk appears to be particularly underestimated by proponents of the so called “TACO” (Trump Always Chickens Out) strategy, which is based on the belief that President Trump ultimately always backs away from his most confrontational decisions. The problem, however, is that given the unpredictable and often chaotic nature of policy making under the current US administration, there is a genuine danger that markets cross a threshold beyond which a loss of confidence becomes difficult to reverse.

From an investor’s perspective, this implies the risk of entering a phase in which even later attempts to soften the political stance will no longer be sufficient to halt negative market dynamics. In other words, markets may stop responding to deescalatory gestures if they are perceived as too late or lacking credibility.

Among the potential “critical points” long discussed are the risk of the US dollar losing its safe-haven status and a perceived erosion of the Federal Reserve’s independence in the eyes of market participants. If investors begin to seriously price in a scenario in which these pillars are permanently weakened, dollar depreciation could take on a self reinforcing character. In such an environment, even a retreat from the most controversial policy actions may fail to restore stability, resulting in a deeper and more persistent weakening of the US currency.

Recent market developments suggest that this scenario is becoming increasingly plausible. President Trump has indeed attempted to deescalate tensions related to Greenland by stepping back from tariff threats against parts of the European Union, which provided the dollar with only a brief period of relief. At present, downward pressure on the USD has intensified again, underscoring that ad hoc measures are insufficient to rebuild damaged investor confidence. A break above 1.19 in EUR/USD now appears highly likely.

EUR/USD has moved back into its medium-term upward channel. The declines seen in late December 2025 and early January proved to be only a temporary episode that briefly altered the direction of price action. For now, the uptrend in the main currency pair appears to remain intact.

EUR/USD exchange rate chart, daily data, source: TradingView