{kind=link}

- We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 5 February in line with consensus and market pricing.

- Lagarde is likely to face questions on the recent strengthening of the euro but provide a neutral answer, not highlighting any target level.

- We expect a muted market reaction as Lagarde refrains from giving new policy signals since the ECB awaits new staff projections in March.

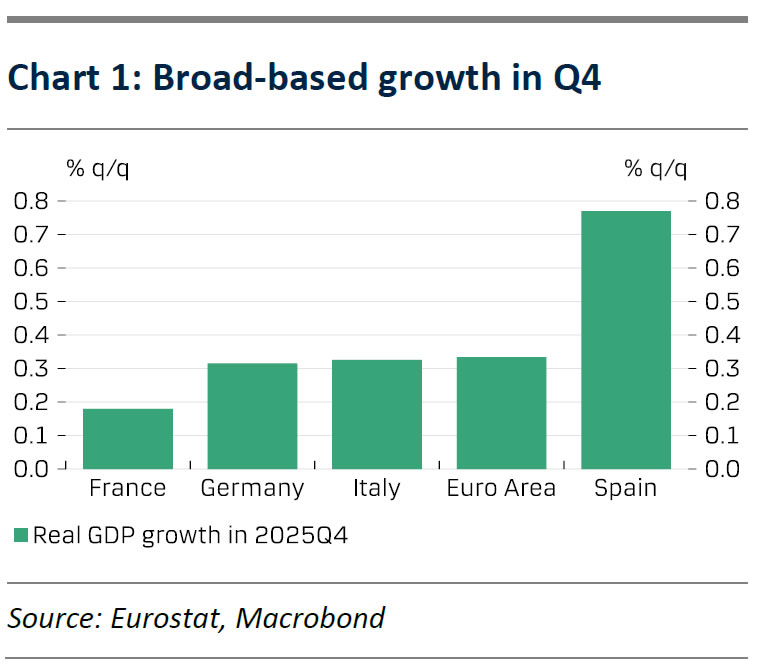

We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday in line with consensus and as priced by markets. There has been a lot of geopolitical turbulence since the December meeting but in the end, it has not changed the outlook for the ECB in our view. While uncertainty and trade barriers hurt economic activity in the long run, demand is much more important for the short-term outlook. Demand is decent as the economy grew more than expected by 0.3% q/q (consensus: 0.2%, ECB staff: 0.2% q/q) in Q4 2025 and the unemployment rate fell to 6.2%. The surprise was driven by stronger-than-expected growth in Germany, Spain, and Italy while France grew as expected – still at a modest pace (see chart 1). As growth in Q4 also seemed to be driven by private consumption and it was broad-based in the eurozone this supports the “good place” assessment of the ECB.

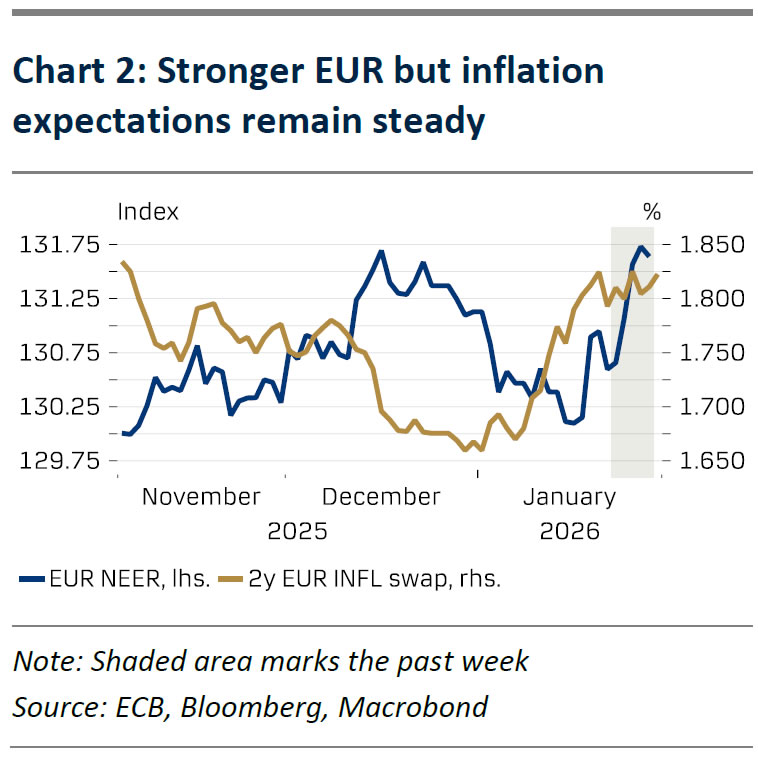

Over the past week, EUR/USD has risen above the 1.19 mark breaking out of the narrow trading range of 1.15-1.17 in H2 2025. This has reignited discussions as to whether a significant strengthening of the euro would meaningfully impact imported inflation and hence become an issue for the ECB. Yet, we note that the broad euro NEER is only 0.2% stronger compared to the December meeting and 1.0% stronger compared to the cut-off date for the latest staff projections as the recent strengthening comes after a weakening over New Year (see chart 2). A paper published by the ECB shows that a 10% appreciation of the nominal effective exchange rate reduces euro area core goods inflation by 0.25ppafter one year and headline HICP by 0.06 p.p. Importantly, we also note that inflation expectations remain steady despite the strengthening (see the shaded area in chart 2) and that a broad weakening of the USD constitutes an easing of global financial conditions (see more in RtM EUR, 30 January). Against this backdrop we do not see the magnitude of the recent EUR appreciation as a cause of concern for the ECB. Lagarde will likely face question about the euro, but we expect her to provide a neutral answer saying it is one of several variables they monitor and have no target level.

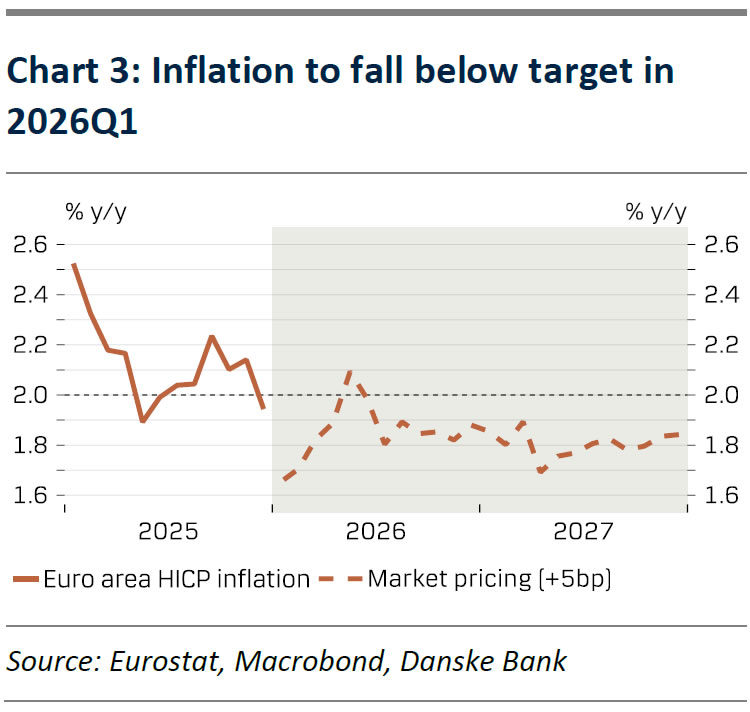

Communication since the last meeting has been supporting the “good place” assessment and indicated no near-term discussions of rate changes in the GC. Inflation in December was softer than expected particularly on core goods while the initial data from Spain and German regions suggests slightly higher than expected inflation in January. Energy base effects are expected to pull headline inflation significantly down to 1.7% y/y in 2026Q1. Yet, with growth still holding up, services inflation being sticky, and as inflation expectations anchored, we do think the bar for new rate cuts from the ECB is high. We therefore expect a muted market reaction as Lagarde refrains from giving new policy signals while the ECB awaits new staff projections in March. We keep our call of 2.00% deposit rate in 2026 and 2027.