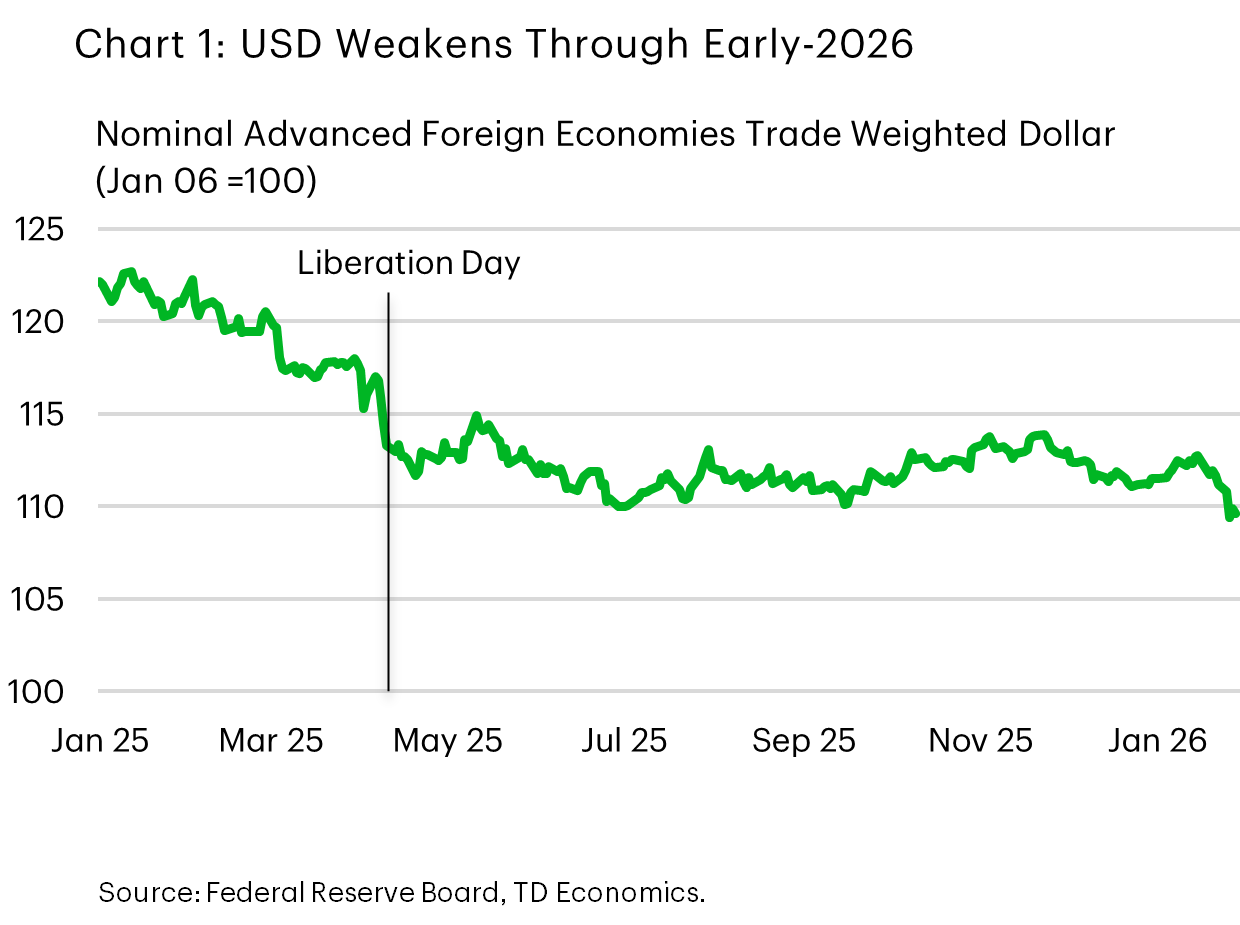

. More recently, Warsh has struck a relatively dovish tone, but historically he has leaned more hawkish. Financial market reaction is somewhat mixed. Equities have turned modestly lower – and look to the end the week in the red – while the yield curve has steepened by several basis points. Meanwhile, gold gave back most of its gains from earlier in the week, while the greenback suffered a second straight week of declines and has now slipped by 2.7% since mid-January (Chart 1).){kind=link}

Canadian Highlights

- Despite a busy week of Canadian economic updates, not much has changed for the economic outlook.

- Declines in non-precious metal exports to the U.S. are only being partly offset by gains elsewhere. This aligns with recent GDP and trade data pointing to effectively flat fourth quarter output.

- An increase in the GST/HST tax credit will provide modest relief to lower income households but is expected to have a limited macroeconomic impact.

U.S. Highlights

- President Trump has nominated former Fed governor Kevin Warsh as the next Fed Chair.

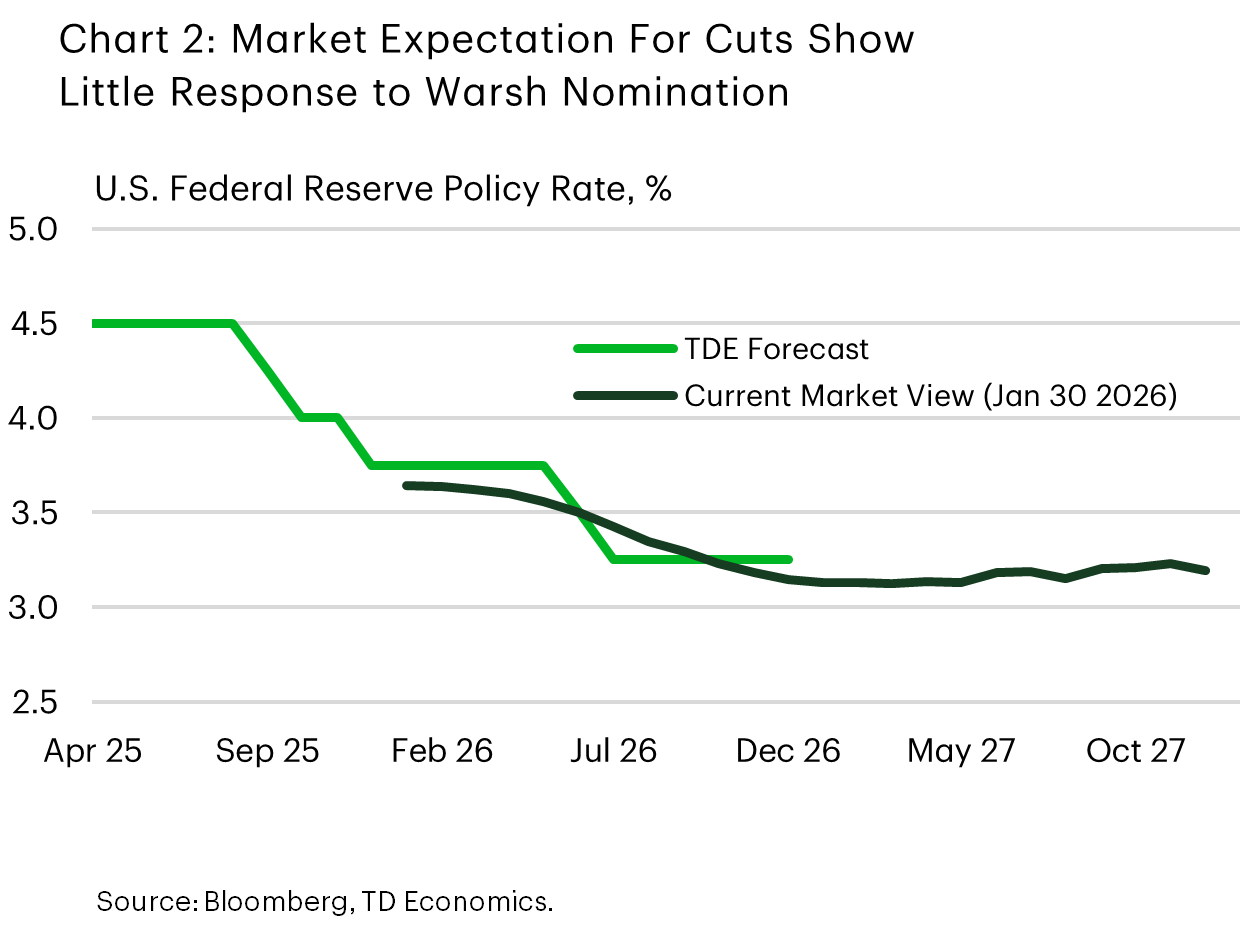

- The Federal Reserve elected to hold rates steady at the target range of 3.50-3.75%.

- The White House and Senate have reached a deal that would avert another government shutdown. The appropriations bill still needs to be confirmed by the House of Representatives on Monday.

Canada – Trade Uncertainty Lingers Over Economy

It was a busy week of updates on the Canadian economy, on top of an announcement of expanded support for modest income Canadians and a widely expected rate hold from the Bank of Canada. Yet, after all the news, Canadian bond yields are roughly in line with last Friday’s close. Currency markets made headlines this week (see commentary) with the U.S. dollar’s (USD) slide since mid-January – lifting the CAD roughly 2.7% against USD over that span. Overall, the economy is still tracking with our prior forecasts, with relatively weak growth expected in 2026.

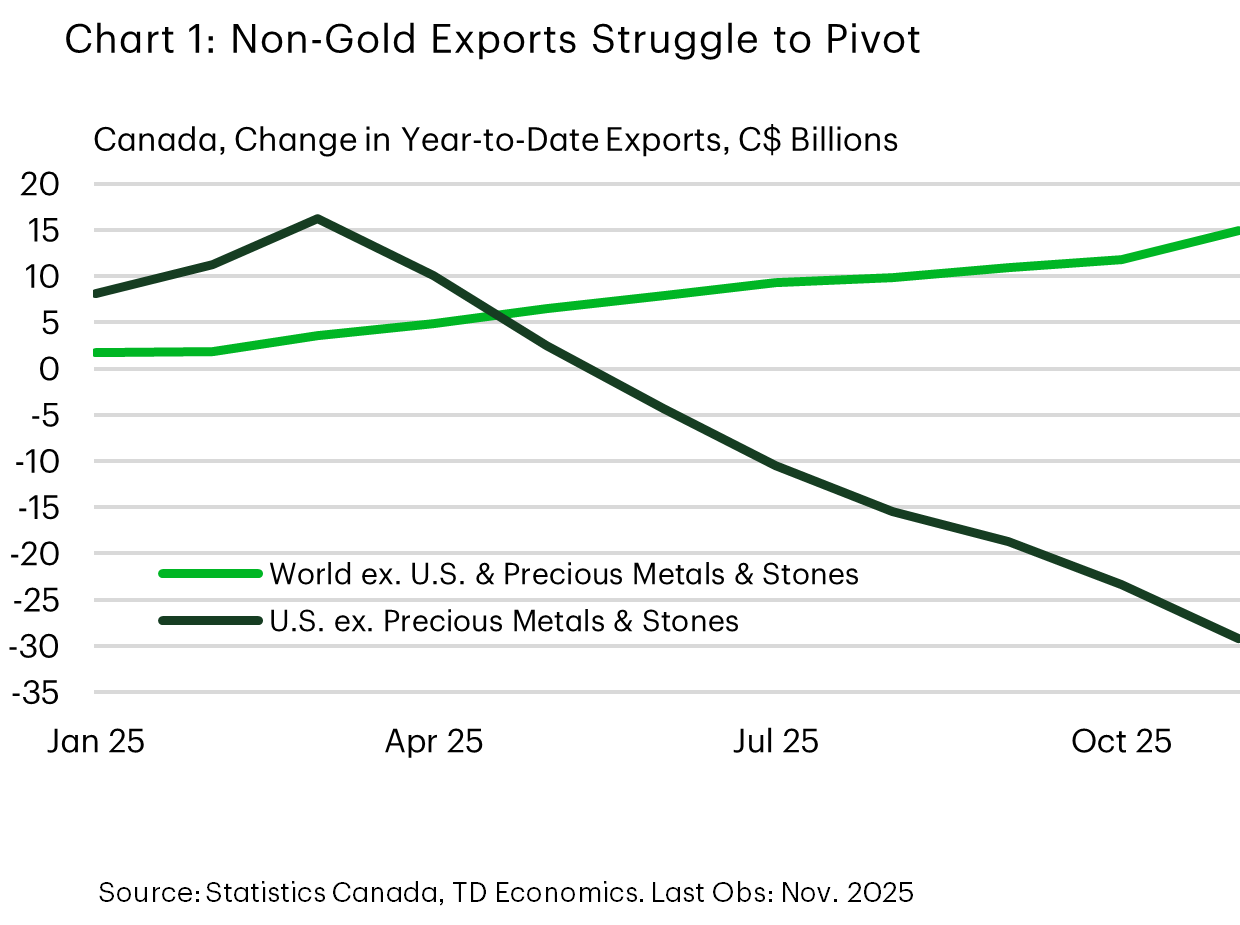

The trade picture remains challenging with the non-precious metal exports to the U.S. down $29 billion year-to-date (-5.5%), while exports to the rest of the world are up a smaller $14.9 billion (+10.9%). The picture highlights the challenge for Canadian exporters in finding or developing new markets.

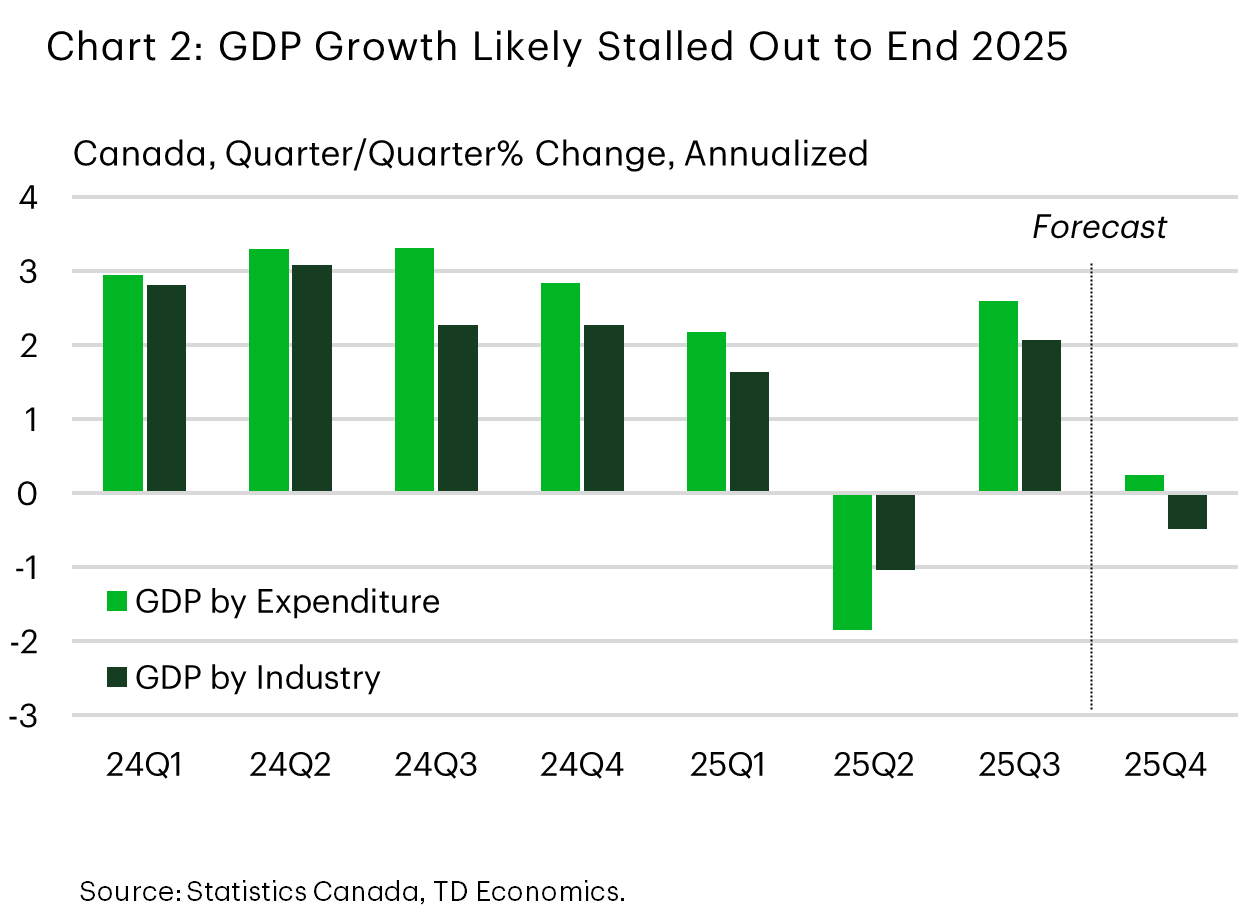

The difficult trade picture squares with the recent data flow from industry. Monthly GDP figures in the fourth quarter suggest a 0.5% (quarter-on-quarter annualized, q/q ann.) contraction to end the year. Now, there’s been a healthy wedge between the monthly and quarterly GDP figures of late (Chart 2), but it is a signal that is hard to ignore. Together with the updated trade figures, we now expect virtually no growth (+0.3%, q/q ann.) in the fourth quarter of the year – a touch above the Bank of Canada’s flat projection. The fourth quarter is a slight mark-down from prior projections but still conforms to the general picture of an economy that is going to struggle to gain traction over 2026. The picture, supported by the November trade data, is one of firms and consumers working under a cloud of uncertainty as they work to adjust to the new trade landscape. Circumstances are not expected to materially change in the coming months as the review of CUSMA picks up.

On the consumer front, the government announced an increase in the GST/HST tax credit, which it has rebranded the “Canada Groceries and Essentials Benefit”. The program is targeted towards lower income Canadians (about 12 million people receive the benefit), with payments expected to increase 25% for the next five years, along with a one-time payment of “a 50% increase” around mid-2026. The impact on the economy is expected to be relatively small (~0.1% of GDP), but could help to alleviate some of the challenges lower-income households have been facing, especially with regards to food costs.

We don’t expect this program to materially affect the outlook and, therefore, inflation. It is relatively small and the currents carrying the economy over the coming months are far more powerful forces. Uncertainty remains very high, so possible outcomes around the baseline are wide, but we expect 2026 to be a year where growth gradually stabilizes as a new normal is established.

U.S. – Kevin Warsh Nominated as Next Fed Chair

It was a quiet week on the economic data calendar, giving financial markets an opportunity to digest a torrent of developments on the earnings, political and policy front. The Fed interest rate announcement took a backseat, with the FOMC predictably holding the policy rate steady, while maintaining its cutting bias. But the bigger news was President Trump’s nominating Kevin Warsh to be the new Fed Chair (see commentary). More recently, Warsh has struck a relatively dovish tone, but historically he has leaned more hawkish. Financial market reaction is somewhat mixed. Equities have turned modestly lower – and look to the end the week in the red – while the yield curve has steepened by several basis points. Meanwhile, gold gave back most of its gains from earlier in the week, while the greenback suffered a second straight week of declines and has now slipped by 2.7% since mid-January (Chart 1).

As of writing, it looks like the White House and Senate leaders have reached a deal to avert another government shutdown… well, sort of. The “deal” will extend funding for five of the six agencies through September 30th. Funding for the Department of Homeland Security, which includes Immigration and Customs Enforcement (ICE), will be split off from the larger appropriations package and will only extend through February 13th. This will allow Congress more time to negotiate new policy measures on the current ICE deployment.

However, the funding bill will need to return to the House for another vote, which won’t happen until Monday, so there will be a brief lapse in appropriations over the weekend. Provided the revised bill passes without issue, the disruptions will be small. However, should passage in the House be delayed, and the shutdown drags on for even a few days, then it’s very likely that the January employment report – scheduled for release on Friday February 6th – will be delayed.

Turning to the Fed announcement, there was little doubt that the FOMC would hold the policy rate steady. For investors, the focus was more on tweaks to the statement and the press conference to get a better sense of forward guidance. Changes to the statement largely reflected a “mark-to-market” on current conditions. The assessment on economic activity was upgraded to “solid” (previously “moderate”), while the reference to the downside risks to the labor market were removed. During the press conference, Powell characterized the current policy stance as “roughly appropriate and not significantly restrictive”. Translation: the FOMC sees reduced risks to both sides of its dual mandate, suggesting less need for further policy action.

Importantly, Fed futures barely budged following President Trump’s announcement that he is nominating Warsh to be the new Fed chair – with two cuts still priced by year-end (Chart 2). For the time being, concerns surrounding Fed independence have been tempered. But rest assured – if confirmed by the Senate – market participants will parse every word over the coming months as Warsh shadows Chair Powell.