{kind=link}

Canadian Highlights

- The U.S. Supreme Court decision to strike down the IEEPA tariffs offers limited near-term relief for Canada, as ample uncertainty remains.

- Canada’s trade diversification thus far relies heavily on gold and oil, raising questions about whether it is sustainable.

- Focus remains on the CUSMA review process, with the resulting uncertainty expected to hang over the economy.

U.S. Highlights

- A Supreme Court decision on Friday struck down a large chunk of President Trump’s second-term tariffs.

- January FOMC minutes reinforced a shift in the balance of risks toward inflation, with policymakers signaling little urgency to resume rate cuts.

- GDP growth cooled to 1.4% at the end of 2025, reflecting a sharp contraction in federal outlays. Core PCE inflation rose to 3.0% y/y in December, remaining well above target.

Canada – IEEPA Tariff Struck Down, But Uncertainty Lingers

The biggest piece of news this week came Friday morning as the U.S. Supreme Court struck down the U.S. administration’s use of IEEPA legislation to impose tariffs. These duties were 35% on non-CUSMA compliant goods flowing from Canada to the United States. The market reaction was relatively muted as the decision was expected given the skepticism expressed by justices in oral arguments in November. Canadian equities are up this week as rising commodities prices have buoyed prospects for the energy sector. Meanwhile, bond yields were little changed on the week as the stream of economic data left the narrative on the country’s economic prospects relatively unchanged.

For Canada, the removal of the IEEPA tariffs represents some limited near-term relief, but it would be optimistic to assume this tariff relief is permanent or provides a sustainable upside risk to growth. First, the administration is likely to use other tariff tools, including the possibility to apply 50% duties on countries for trade practices deemed to “discriminate” against the U.S. We expect some new form of tariff regime will be established. Moreover, the IEEPA tariffs only applied to the subset Canadian goods that were not compliant with CUSMA rules of origin and that were not covered under Section 232 tariffs (autos, steel, aluminum, etc.), leaving many goods unaffected by the decision.

This week’s trade data gives some indication of the tariff impact. Exports to the U.S. were down $30.9 billion through 2025, of which $15.5 billion were in categories of goods affected by Section 232 tariffs. Of the remaining $15.4 billion decline, $13.5 billion is attributable to a decline in oil exports (which have been weighed down by lower prices and refinery outages in the U.S.). The decline in exports of goods that are not oil, gold, or covered by Section 232 was roughly $3.8, down a meagre 1.4% relative to last year.

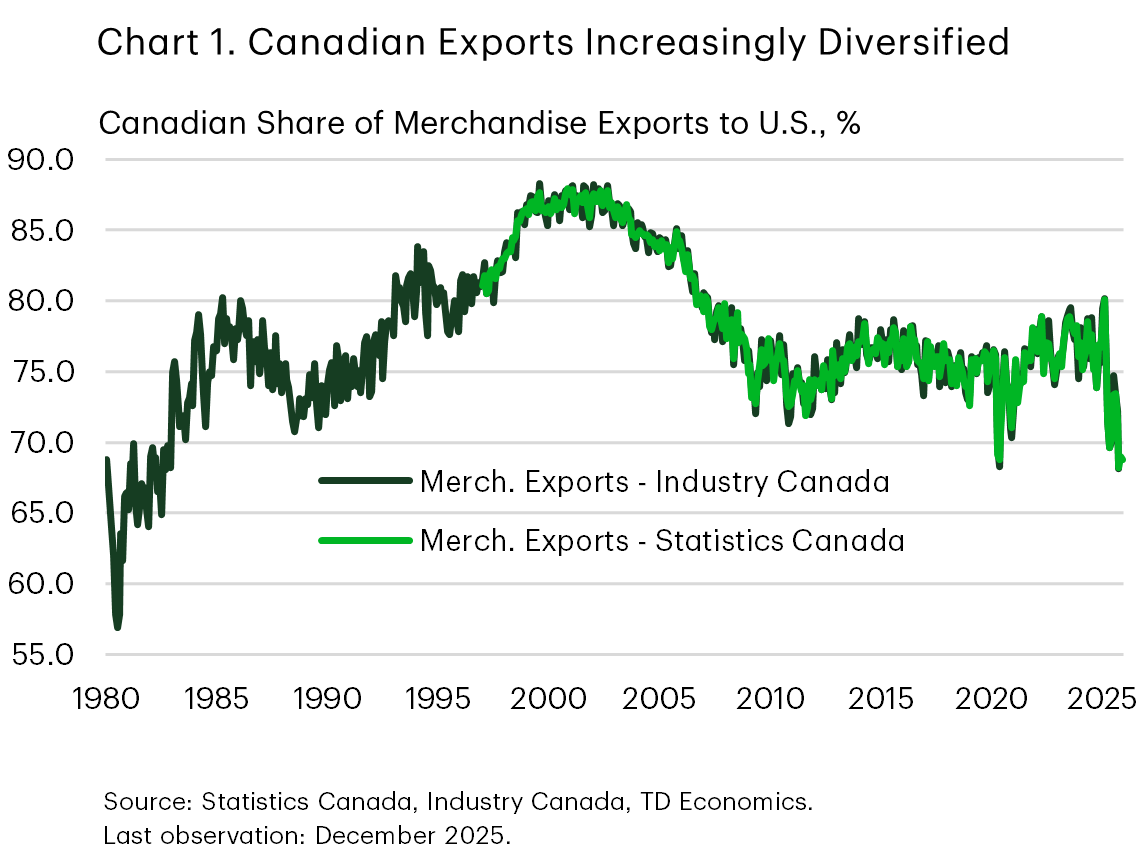

So, the focus for Canada remains the trade landscape and ongoing efforts to diversify its trade partnerships. As of December, Canada shipped roughly 68% of its goods exports to the U.S. The figure is down significantly from the 76% registered in December 2024, roughly unchanged since October. The 68% share is similar to the export composition during the pandemic, and a level of interaction not seen in over 40 years (Chart 1).

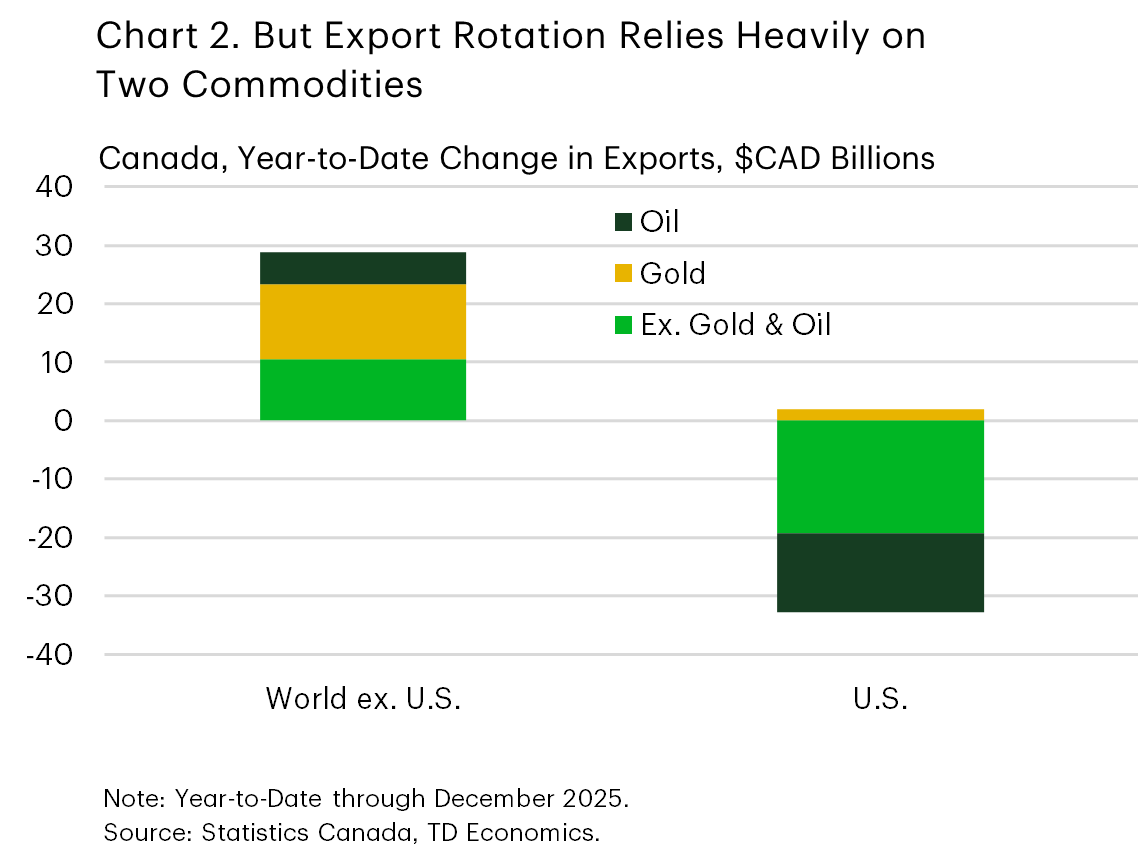

The rotation is underway, but it’s not all good news. Exports that are being negatively affected by U.S. tariffs are struggling to find new markets. Much of Canada’s success on the trade front has relied on two commodities; gold and oil. Total exports to the U.S. are down $30.9 billion through 2025, while flows to the rest of the world are up $28.8 (Chart 2). However, strip out the effects of these two commodities and the declines to the U.S. register $19.3 billion with a smaller $10.5 billion offset from the rest of the world.

This lack of new export markets for affected industries and the prominent role of commodities prone to large price changes does little to assuage concerns about the long-term sustainability of the current export mix, and the prospects for Canadian industry. Looking forward, the CUSMA review is set to pick up steam, and the resulting uncertainty is expected to hang over the economy.

U.S. – Tariff Uncertainty Makes a Comeback

Financial markets were largely rangebound for much of this week as investors digested the January FOMC minutes and an important run of macro data. Early market reaction to the Supreme Court’s decision to strike down a large chunk of President Trump’s second term tariffs appears broadly positive, with the S&P 500 is up 0.9% from last week’s close at time of writing.

The Supreme Court ruling found that the law that underpins many of Trump’s global tariffs – the International Emergency Economic Powers Act (IEEPA) – “does not authorize the President to impose tariffs”. The decision did not rule on how or if tariffs that have already been paid should be refunded – a potentially messy process. We expect the U.S. administration will act quickly to recreate its tariff regime using justification from other statutes. For more on this, see our commentary here.

Prior to the tariff decision, the January FOMC minutes dominated the financial market limelight. Two key takeaways stood out from the minutes. First, the balance of risks has shifted away from labor market weakness and toward inflation staying uncomfortably high. Driving home this point was the fact that most committee members judged that “downside risks to employment had moderated, while the risk of more persistent inflation remained”. Importantly, this assessment occurred before the release of last week’s delayed payrolls report, which showed a firmer labor market than many feared. Second, most participants judged that the current policy rate is closer to neutral rather than restrictive. That assessment diminishes the urgency to resume rate cuts.

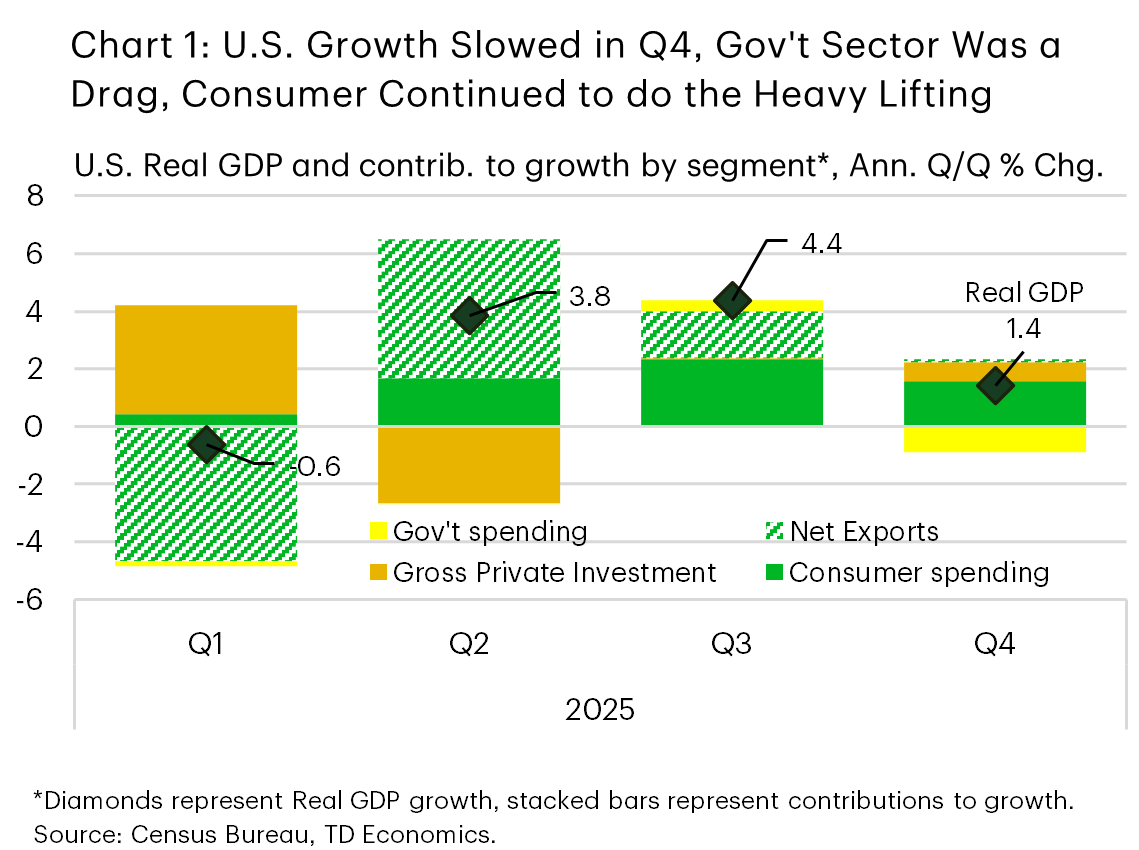

This week’s macro data broadly echoed the tone of the minutes, even as growth was weaker than expected at the end of 2025. Fourth-quarter GDP growth came in at 1.4% annualized in the first estimate, a notable slowdown from 4.4% in the third quarter (Chart 1). The disappointment was driven largely by a steep pullback in federal outlays, reflecting the 43-day government shutdown. Importantly, final sales to private domestic purchasers rose 2.4%, underscoring the resilience of underlying private sector demand despite the headline slowdown.

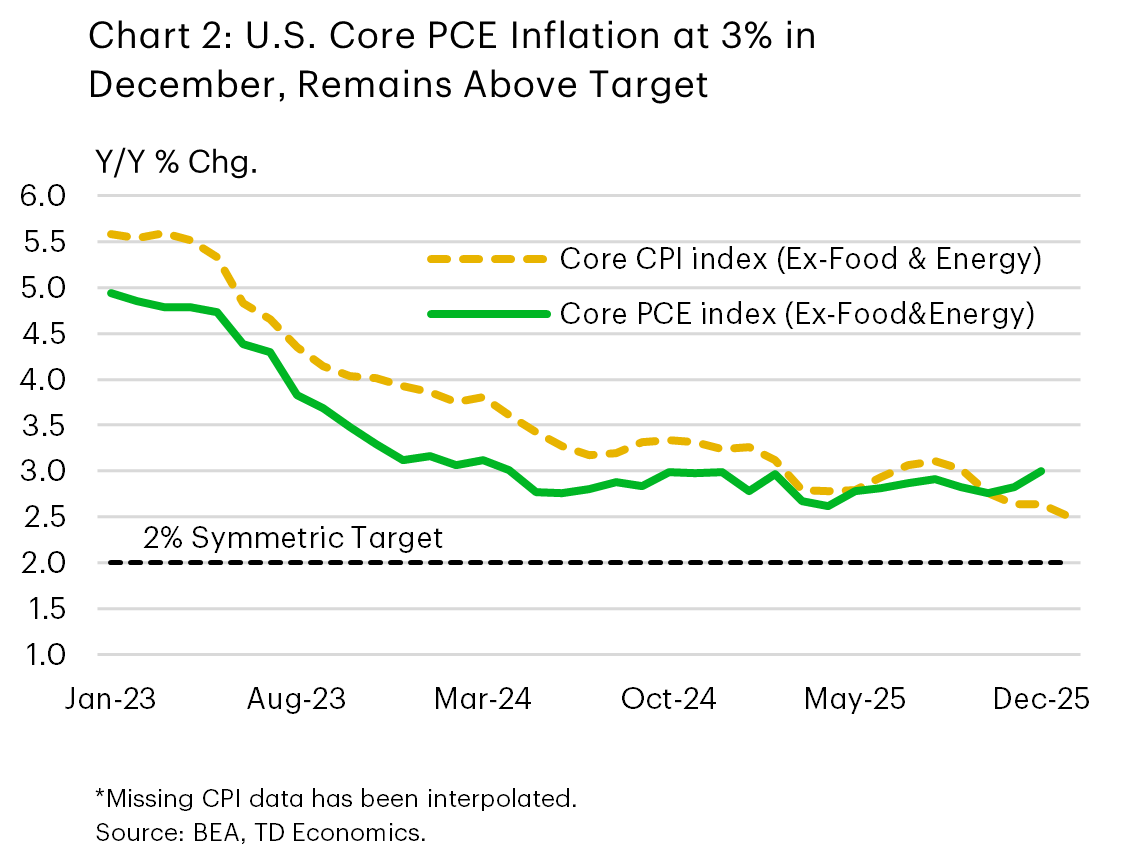

The December personal income and outlays report added further color to the economic backdrop at year‑end. Real consumer spending was up just 0.1% m/m in December, reflecting a pullback in goods spending. Inflation pressures, meanwhile, re‑accelerated at the margin. Core PCE inflation rose to 3.0% y/y, remaining well above target (Chart 2).

All told, even after accounting for this morning’s miss on Q4 growth, we still feel that the U.S. economy has entered 2026 with considerable momentum. That said, it appears that 2026 may start off in similar fashion to 2025 after all – with elevated tariff uncertainty. This reinforces the notion that the Fed will remain on hold for the time being, as it waits for the policy fog to clear.