{kind=link}

Summary

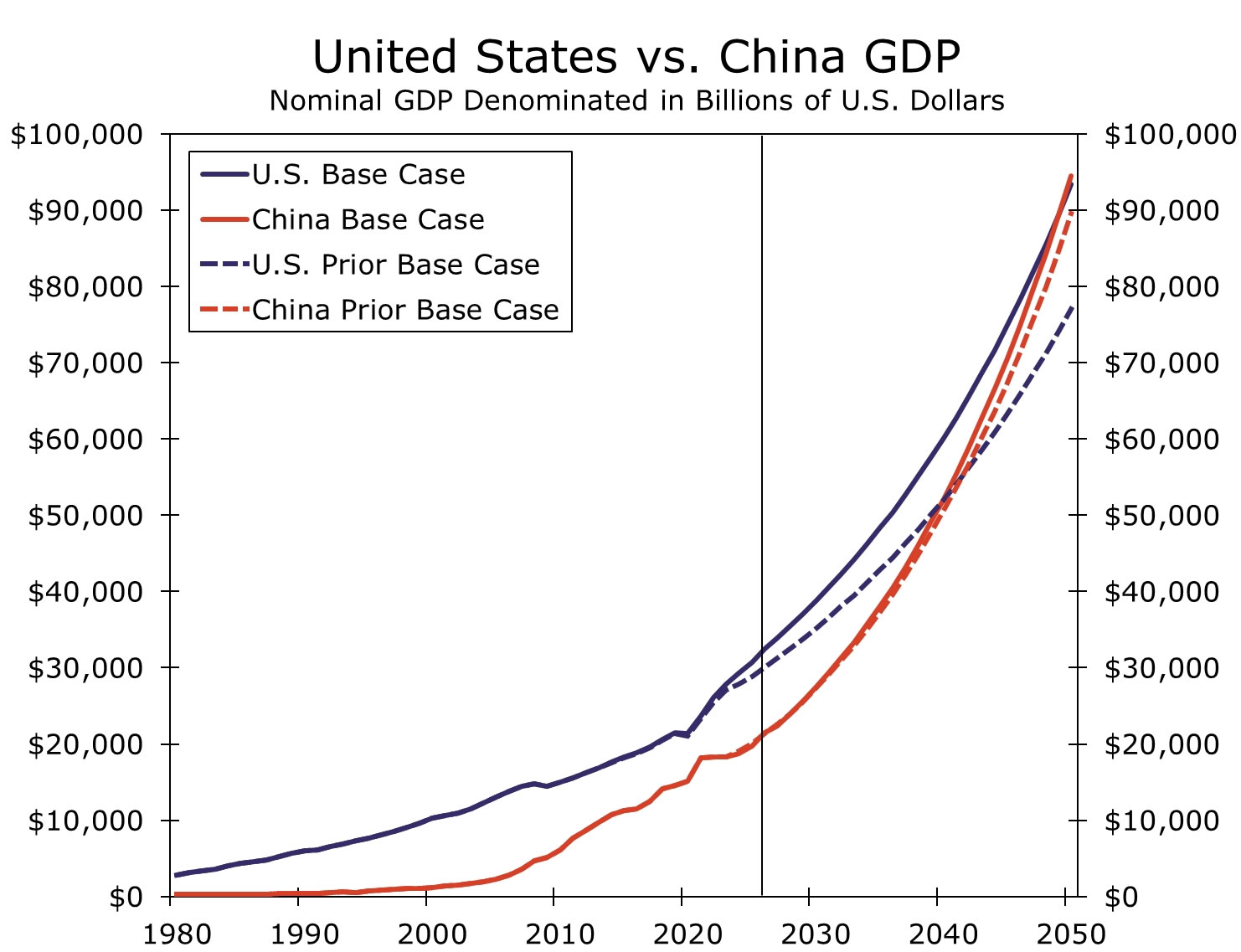

China’s rise to the world’s largest economy is again delayed. We now estimate China overtakes the U.S. to become the largest economy in the world in 2049, pushed out from a prior estimate of early 2040s. Despite last year’s resilience, the delay is a product of deteriorating underlying fundamentals that determine potential growth. China’s population is smaller and older, deflation pressures are persistent, and rising private and public sector leverage re-introduces “hard landing” risks in China.

At the same time, fundamentals in the U.S. are on an improving trajectory and diverging from underlying trends in China. Just as worsening fundamentals will keep China stuck in second place for a longer period of time, improvements across potential growth indicators should set a solid foundation for long-term U.S. economic growth. “Hard landing” risks in China are not as apparent in the U.S., which also keeps downside risks centered in China.

Embedded in our 2049 estimate is also the view that the Chinese renminbi will strengthen going forward. We continue to believe Chinese authorities have fundamentally shifted the way FX policy is considered and set with a preference for financial stability as opposed to currency weakness. FX policy can change as domestic and external conditions change, and while our renminbi assumption is more constructive relative to FX forwards, should the renminbi trend in line with forward pricing, China’s ascension to the top of the economic pedestal could come earlier than we expect, despite imbalances and structural impediments to sustainably high growth rates.

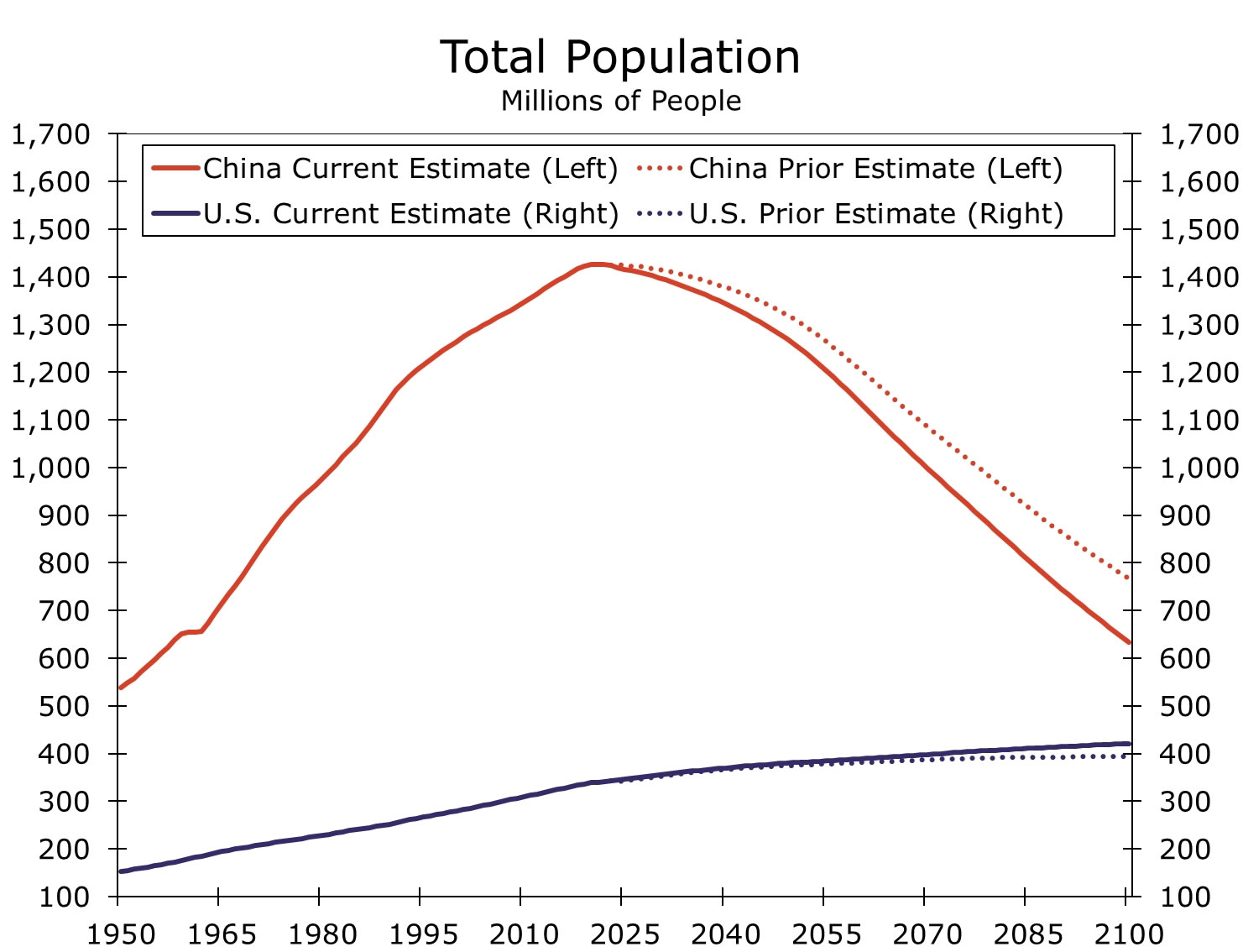

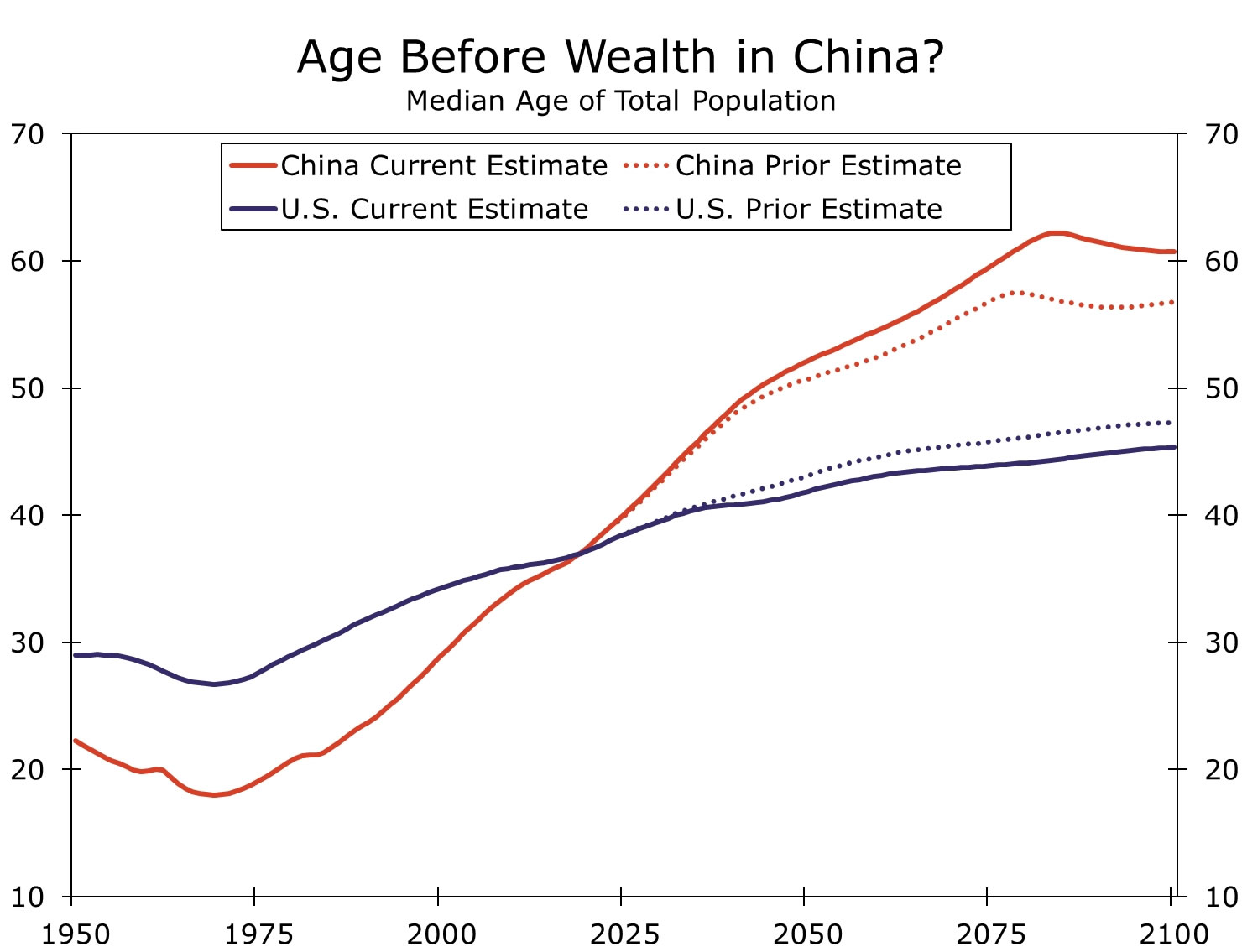

Demographics, deflation and debt are China’s most pressing challenges. Each of which have contributed to slower growth over the years, and each of which have deteriorated recently. So much so that demographics, deflation and debt are likely to apply even more downward pressure on China’s growth than we previously anticipated. On demographics, China’s problems are known, although perhaps not fully appreciated is how China’s population is now shrinking more rapidly (Figure 1) and aging quicker (Figure 2), according to the United Nations (UN). The UN now expects China’s population to more than halve over the coming decades, a significantly quicker decline than prior forecasts. A similar dynamic exists for age as the UN now estimates China’s population is getting older quicker than expected.

All else equal, a smaller and older labor force equals slower potential growth, and while the U.S. is far from setting the standard for ideal demographics, U.S. labor force trends are on a better trajectory than those in China. Population size is set to grow in the U.S. and that population is set to age at a less rapid pace. At least from a demographics’ perspective, long-term economic growth should be more resilient in the U.S. than China, and population trends are a key input into our view that China’s timetable for overtaking the U.S. is pushed out.

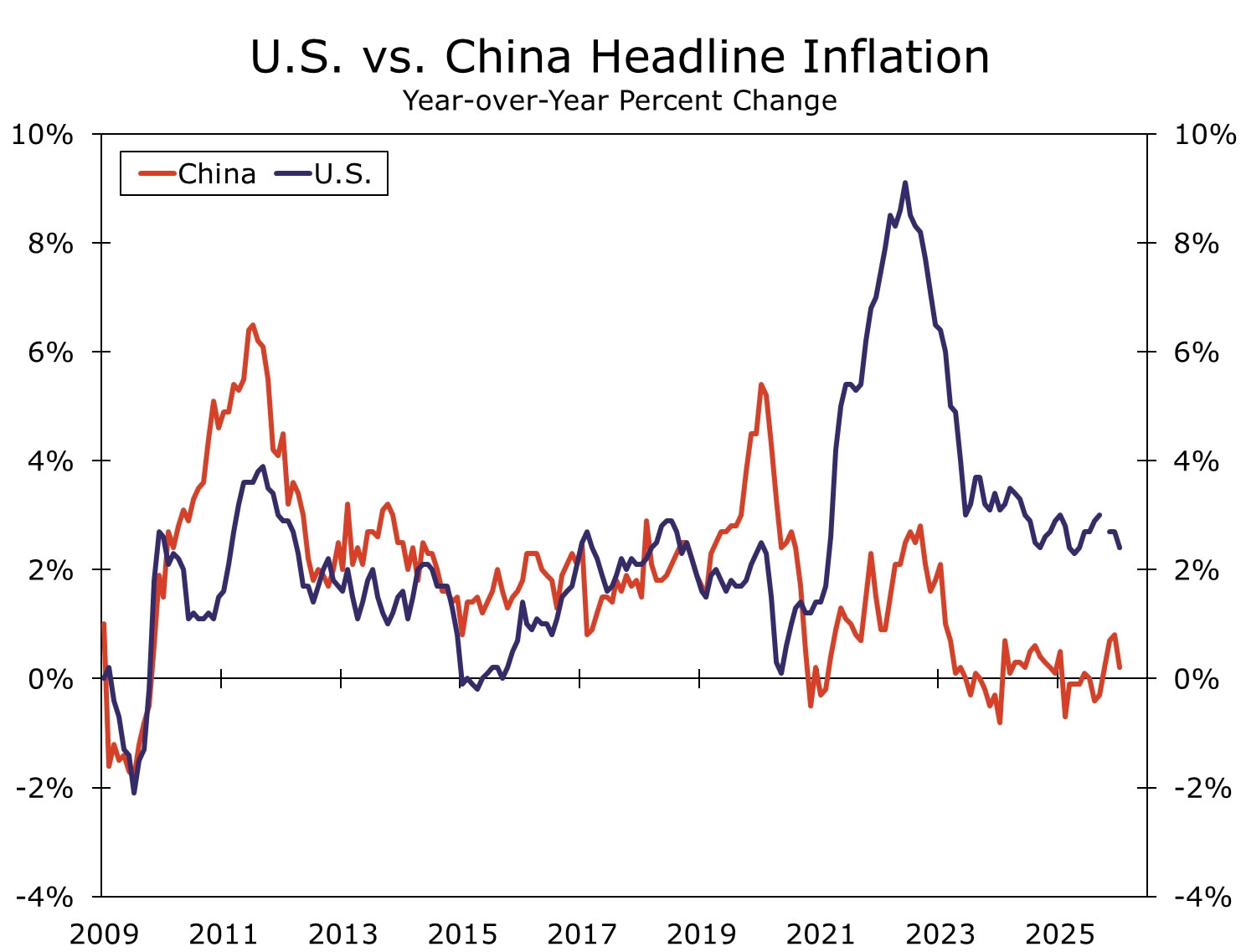

Diverging inflation trends between the U.S. and China also play a role in China lagging further behind the United States. We can point to multiple factors that generate deflation pressures in China (e.g., low consumer confidence, high household savings, sluggish domestic demand, real estate sector collapse), although just as influential are local manufacturers cutting prices to clear excess inventory (Figure 3). China’s export price index is down ~15% from the peak in 2023, and while anti-involution policies have helped put a floor underneath prices, export prices remain suppressed.

Front-running tariffs catapulted China’s share of the global export market higher, but if China wants to retain current market share, prices may be kept low and deflationary pressures could linger. U.S. inflation trends diverge from those in China (Figure 4). While above-target inflation in the U.S. can generate economic issues, for now, strong U.S. GDP growth combined with inflation pressures widens the gap between the U.S. and China.

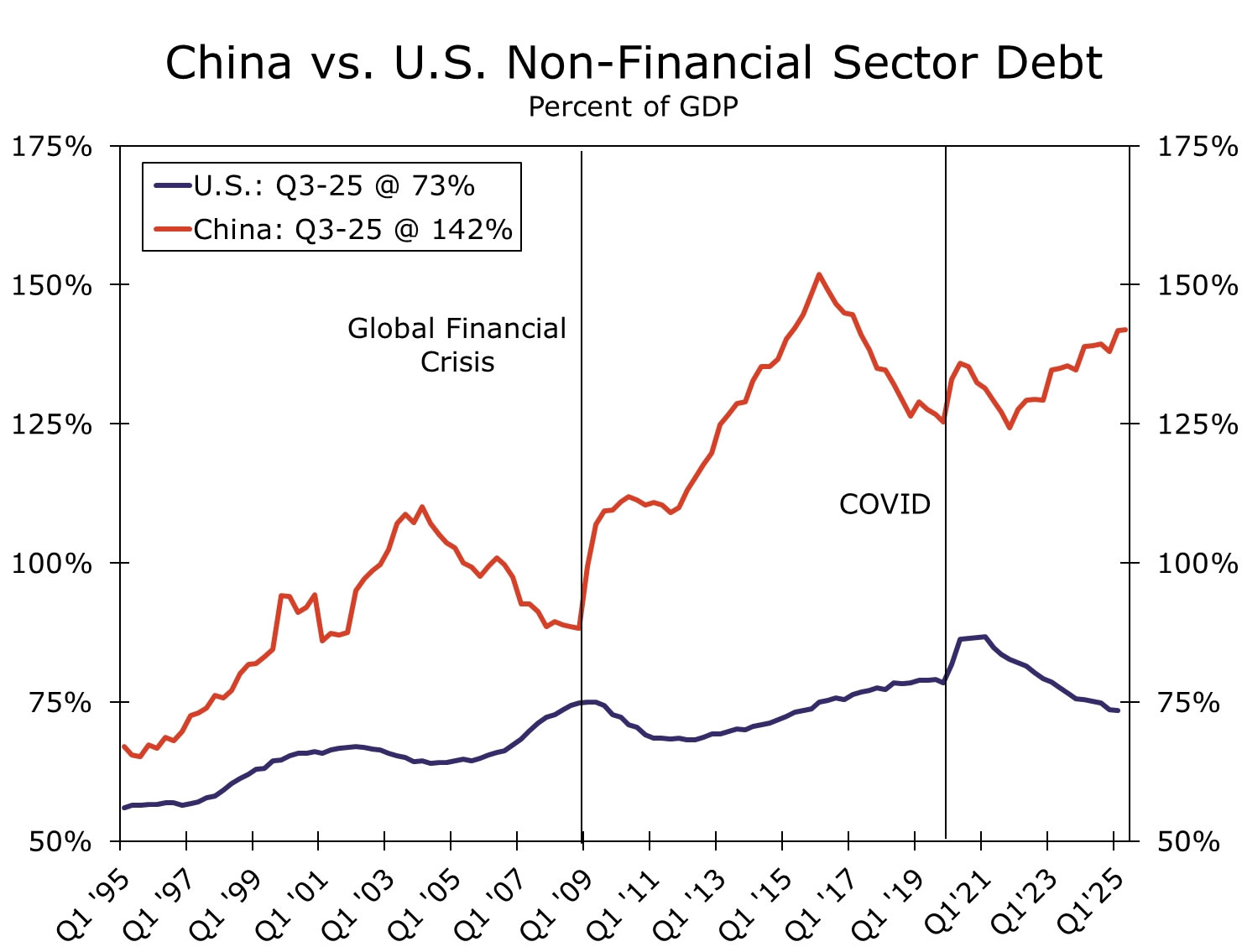

Historically, an overleveraged private sector, not excessive public sector debt, has preceded rapid economic slowdowns and acted as catalysts for financial crises (e.g., Japan 1980s, EM Asia 1990s, U.S. 2000s). For China, the most pressing leverage problems still exist in the private sector, and after multiple failed attempts at deleveraging, China’s private sector debt problems are intensifying. For the past few years, China’s private sector debt burden has been rising and is approaching all-time highs. Corporate debt is likely to rise further now that “three red lines” policies have been relaxed, a decision that can not only pressure long-term growth rates but also re-introduces China “hard landing” financial crisis scenarios.

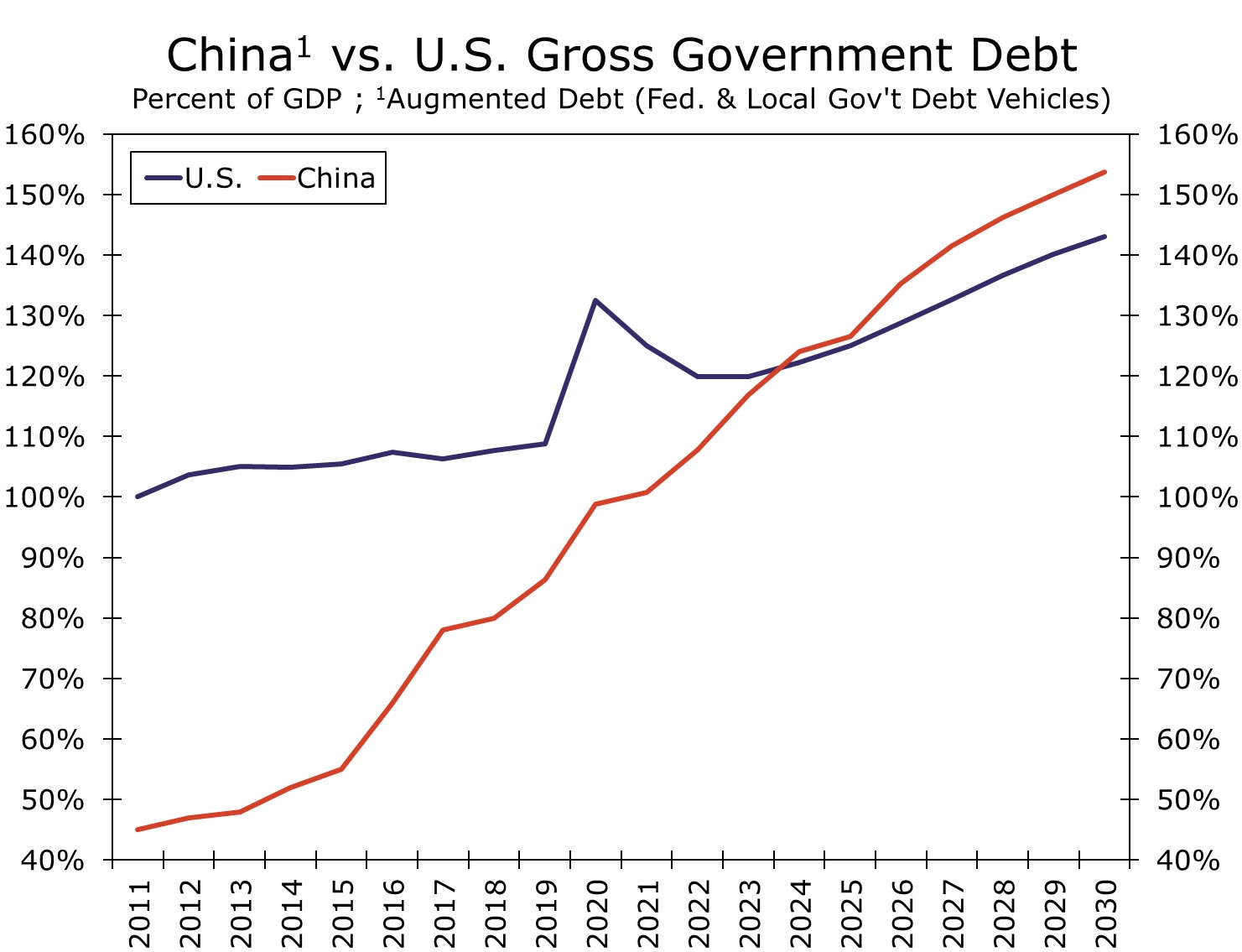

The trajectory of China’s private sector debt burden is diverging from trends in the United States (Figure 5), leaving the U.S. economy on a more stable foundation for long-term growth. Whether a crisis unfolds in China or not, diverging private debt trends keep “hard landing” financial risks top of mind in China not the U.S., leaving downside risks to long-term growth more present in China. Also, for all we hear about U.S. government debt, China’s public sector debt burden is larger, at least when adjusting for local government financing vehicles (Figure 6). Should private sector leverage issues spill over into the public sector, China has more acute issues, a dynamic that also delays China from catching up to the U.S., in our view.

The IMF suggests China may never overtake the United States… As far as comparing our growth and inflation outlooks, the IMF is more pessimistic on China’s growth prospects, at least over the Fund’s forecast horizon (i.e., the next five years). We—as well as the IMF—expect China’s economy to be unable to sustain 5% growth rates going forward, but the IMF expects a more rapid economic deceleration. At the same time, the Fund is more optimistic that China will be able to reflate its economy to 2% in the coming years than we are. Although taken together, IMF nominal GDP forecasts are less constructive than how we see China’s economy evolving. However, the IMF takes a less optimistic view on U.S. nominal GDP growth relative to ours. We both believe U.S. nominal GDP will hold steady going forward as opposed to trend deceleration in China, the IMF just holds a less optimistic definition of steady. If we extrapolate the IMF’s relative views on China and the U.S. over a longer-term horizon, the IMF is inherently, based on our longer-term extrapolations, saying China will never overtake the U.S. as the world’s largest economy.

…but the renminbi is the larger swing factor for China ascending to the world’s largest economy. IMF forecasts, however, assume the Chinese renminbi holds steady around current levels for the foreseeable future. While the Chinese renminbi is not a particularly volatile currency, our base case 2049 estimate assumes China’s currency gradually strengthens going forward as we believe China’s FX policy is based on currency strength to promote financial stability (perhaps due to “hard landing” risks rising) as opposed to a historical preference for RMB weakness to support export competitiveness.

In our base case 2049 scenario, we assume RMB strengthens 1% per year going forward. We made this same assumption in our prior estimate for when China could overtake the U.S., so no change that distorts the analysis is coming from FX. We believe worsening underlying fundamentals, not RMB, are the driving force of China’s delayed rise.

But while we assume RMB strength going forward, worth noting is that we still hold a less optimistic view on RMB relative to FX forward pricing. If we were to incorporate our baseline GDP and CPI forecasts with current RMB forward pricing, China could overtake the U.S. as early as 2038. Even if we were to use the IMF’s GDP and inflation forecasts and adjust for FX forwards, China becomes the world’s largest economy in 2039. In a scenario where the renminbi weakens, China moves further away from overtaking the United States.

Point being, just as much as underlying fundamentals play a role, so does China’s currency. Typically, currency performance moves in line with economic fundamentals, but not necessarily when a managed currency regime similar to China’s is in play. Granted, FX policy is not static and can change based on external or domestic factors, but if Chinese authorities are committed to financial stability and promoting the renminbi as a world’s reserve currency at a time when the dollar is broadly depreciating, China’s ascension could come a bit quicker even if underlying fundamentals are being eroded.