. If the proposed 15% Section 122 surcharge is finalized, weighted average tariffs would rise to around 15%, still modestly below prior levels. This limited relief supports our view of steady global growth amid elevated policy uncertainty and rising idiosyncratic risks (see International Economic Outlook: February 2026).){kind=link}

Summary

- The Supreme Court ruling on International Emergency Economic Powers Act (IEEPA) tariffs provides limited relief for the rest of the world, with weighted average tariff rates modestly lower. This is consistent with our baseline view of steady (but uncertain) global growth, rather than a material downside shock.

- The binding constraint now comes from Section 122’s flat surcharge (10% as implemented, with 15% still under consideration), applied uniformly across countries.

- This results in clear relative winners and losers versus the pre-Supreme Court ruling landscape. Under a 15% Section 122 regime, tariff rates fall the most for China, India, Brazil and South Africa, while they rise for the UK, EU, Australia and Japan.

- The ruling also creates an unprecedented legal vacuum for the 19 countries that struck trade deals with the US in recent months. Deal rates lack an enforceable legal mechanism, having been implemented exclusively through IEEPA authority.

- In practice, this sets up a classic prisoner’s dilemma. While countries could challenge or renege, fear of retaliation via Section 301/232 investigations alongside non‑trade leverage in defense, technology and diplomacy, will likely deter overt confrontation. Slow‑walking of commitments appears more likely than outright withdrawal. Section 338 tariffs remain a wild card, though the legal bar for deployment appears high. On net, trade deal momentum with the US is likely to slow materially in 2026.

Key takeaways

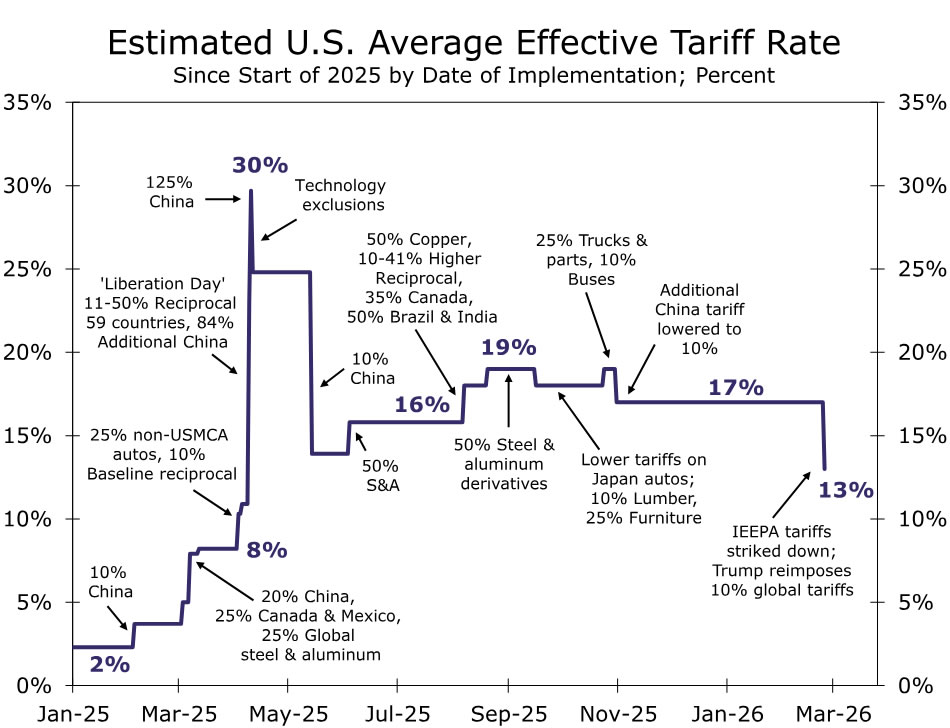

The U.S. weighted average tariffs rate declined to 13% from 17% following the Supreme Court’s February 20 ruling striking down IEEPA tariffs and the administration’s imposition of 10% Section 122 tariffs on February 24 (Figure 1). If the proposed 15% Section 122 surcharge is finalized, weighted average tariffs would rise to around 15%, still modestly below prior levels. This limited relief supports our view of steady global growth amid elevated policy uncertainty and rising idiosyncratic risks (see International Economic Outlook: February 2026).

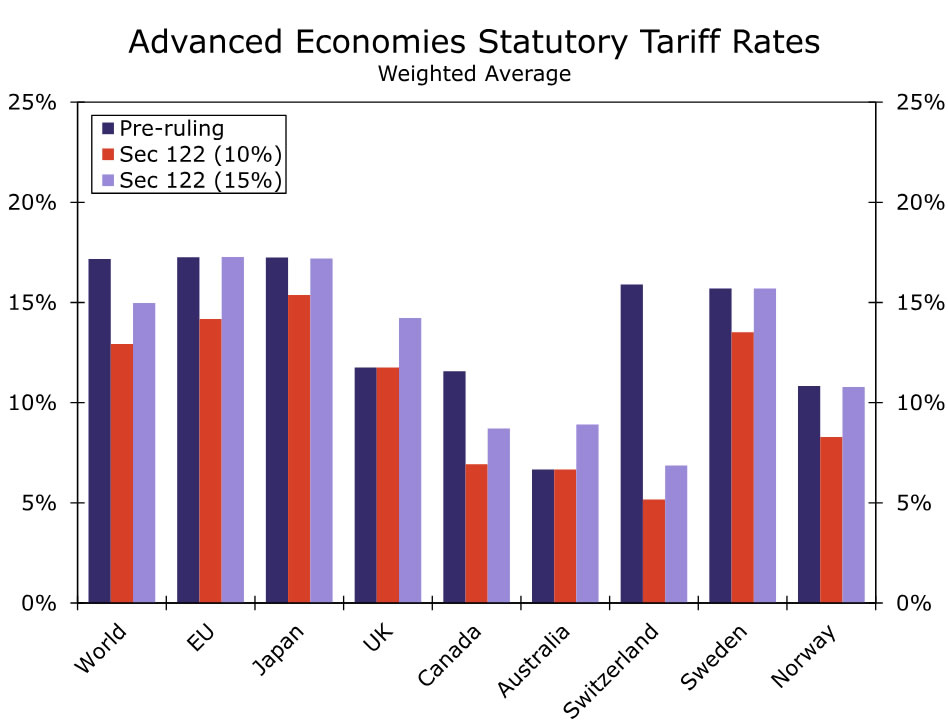

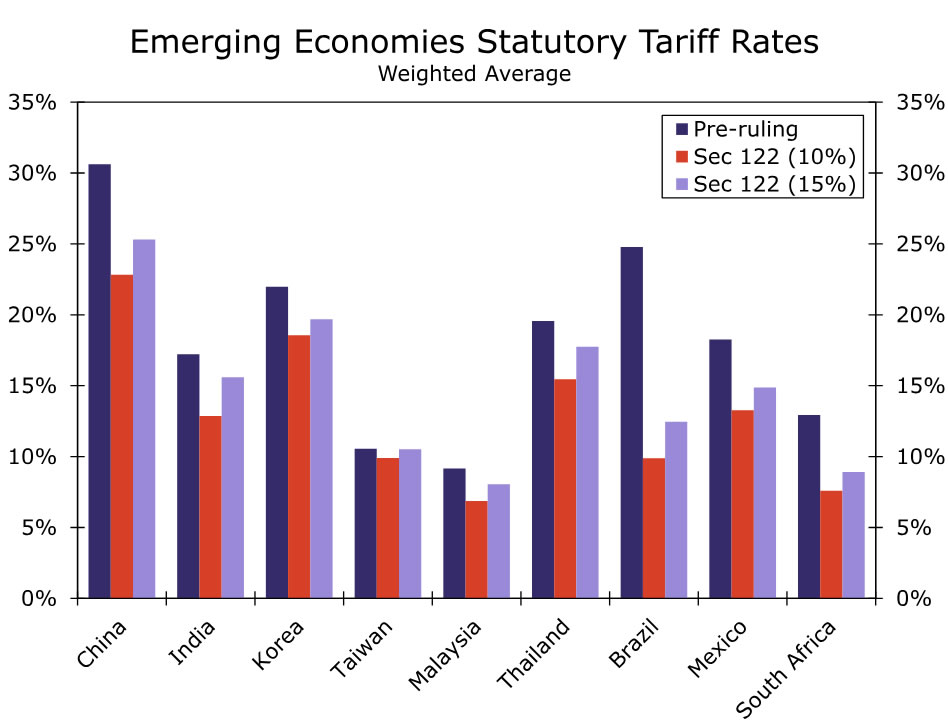

Section 122 of the Trade Act of 1974, now serving as the interim replacement, has a critical structural limitation: it must be applied on a non‑discriminatory basis. While it authorizes a temporary import surcharge to address balance‑of‑payments concerns, it does not allow country‑specific differentiation. As a result, the administration cannot legally impose a 10% rate on one country and 15% on another under Section 122 alone. For now, U.S. Customs and Border Protection (CBP) has implemented the original 10% rate, while the administration works toward finalizing the increase to 15%. The surcharge stacks on top of Most Favored Nation (MFN) duties and existing section 301 tariffs, while fully replacing IEEPA‑based rates.

This produces meaningful cross‑country dispersion relative to prior tariff levels. Figure 2 and Figure 3 compare current and planned statutory tariffs with those prevailing pre‑ruling for major advanced and emerging economies, applying existing exemptions and (unstacked) sector specific tariffs. Under a 10% Section 122 regime, tariff rates decline for most trading partners with the United Kingdom and Australia as notable exceptions with unchanged rates. Under a 15% regime, tariff relief is largest for China, India, Brazil and South Africa versus pre-ruling levels, while tariff burdens rise for the UK, Australia, EU and Japan.

The Supreme Court decision creates a unique and unresolved legal situation for the 19 countries that finalized trade deals in recent months. All bilateral agreements since 2025 such as those undertaken by the EU (July), UK (May), Japan (September), South Korea (November), Indonesia (July), Taiwan, India and others, were implemented via executive orders with tariff rates set using IEEPA. The Court’s 6‑3 ruling made clear that IEEPA does not authorize tariffs, voiding the sole enforcement mechanism underpinning these agreements. The deals themselves were executive agreements, not Congress‑ratified treaties, leaving them without a clear legal foundation.

Section 122 authority expires on July 24, 2026, unless extended by Congress—an outcome we see as unlikely given bipartisan opposition and heading into the November Midterm elections. In the interim, the administration is likely to rely more heavily on accelerated Section 301 investigations, which offer the most robust path toward restoring country‑specific tariff authority and face no statutory rate cap. These are likely to be complemented by ongoing and prospective Section 232 investigations across sectors such as semiconductors, pharmaceuticals, drones and other strategic industries. Section 338 tariffs under the Tariff Act of 1930, which authorizes duties of up to 50%, remain a theoretical option, but their non‑use thus far suggests a higher legal and political threshold.

A strategic game is now unfolding that likely implies slower deal-making in 2026. Section 122 appears to function as a bridge while the administration reconstructs a legally durable tariff regime via 301/232 authority. Countries that negotiated deals face a sharp asymmetry: concessions (investment pledges, market access, export‑control alignment) were real and in many cases already delivered, while agreed tariff ceilings have been legally nullified. We see responses falling into three broad buckets:

- Wait and see (EU, UK): The EU has frozen ratification of its July agreement that had achieved a 15% “inclusive” deal rate rather the potential 15% Section 122 tariffs “adding” to 2-4% MFN rates. The European Parliament’s trade committee has postponed a vote pending “full clarity” from Washington. EU leverage remains significant with $600bn in pledged US‑directed investment and zero tariffs on US industrial goods. A breach of deal ceilings would allow the EU to withdraw concessions and reimpose retaliatory tariffs. The UK has adopted a similar posture, though with less confrontational rhetoric. Figure 2 shows the UK’s gap between the threatened 15% tariffs and the 10% deal rate is the widest among peers.

- Signal commitment and seek protection (Japan, Korea, Mexico, Canada): Japan and Korea have also raised concerns that their agreements set 15% as an all‑in ceiling, compared to the Section 122 surcharge. Japan’s Trade Minister Akazawa has explicitly flagged the discrepancy, yet Japan has reiterated its intention to proceed with its $550bn investment commitment, including a recently announced $36bn critical minerals package. Korea has likewise indicated it will honor its deal. Separately, we expect Mexico and Canada to continue to push for USMCA compliance as a means of reducing the impact of announced tariffs. Ultimately, this ups the ante for ongoing discussions of USMCA extension that need to be completed by July 1, 2026.

- Slow‑walk compliance and delay engagement (China, India, Brazil, South Africa): With IEEPA leverage removed, US coercive power has weakened materially. These countries were subject to the highest IEEPA rates and are the primary beneficiaries under Section 122. We expect slow compliance under existing understandings and a deliberate delay in deeper deal‑making as the administration works to re‑establish its tariff authority. The lower tariff rates imply modest improvement in near-term sentiment even as the medium-term uncertainties about the economic relationship with the US linger.