Sunrise Market Commentary

- Rates: Corrective steepening, even if Fed holds scenario?

We expect the US central bank to continue its tightening cycle and keep a more hawkish tone with (small) upside risks to the 2019 dot and to growth forecasts. The impressive sell-off on the front end of the yield curve suggests that some short term profit taking is possible while immediate losses at the longer end of the curve seem more likely given current positioning. - Currencies: Fed to solidify USD downside protection

Today, the focus for USD trading is on the Fed policy decision. A scenario of 3 rate hikes in 2018 should further protect the USD downside. However, the market as already moved in that direction of late. So, any further USD gains might remain modest.

The Sunrise Headlines

- US stock markets closed yesterday’s session mixed with Nasdaq underperforming (-0.2%) and Dow Jones outperforming (+0.5%). Asian risk sentiment is positive overnight with Japan underperforming.

- Democrat Doug Jones of Alabama scored an upset win in a deeply Republican state, capturing the US Senate seat here in a special election that drove a wedge within the Republican party and gave Democrats another burst of momentum ahead of the 2018 midterm races.

- The EU warned the UK against rowing back on the agreements it made last week as leaders prepare to hand Britain its first reward in the Brexit negotiations.

- Crucial details of the Republican tax plan, including the proposed corporate rate, were in flux late on Tuesday as negotiators from the US Congress rushed to finalize the plan ahead of a self-imposed Wednesday deadline.

- A bitter EU row over imposing refugee quotas on member states has reignited, leaving leaders struggling to reach agreement on how to handle the next migrant surge.

- Japanese machinery orders bounced back in October with a faster increase than expected (5% M/M), re-affirming the resilience of capital spending – a key driver in the economy’s near two-year expansion.

- Today’s eco calendar contains EMU industrial production, the UK labour market report, US CPI and the Fed meeting. The FOMC is expected to raise its policy rate to 1.25%-1.50% and will release new projections for 2018, 2019 and 2020.

Currencies: Fed To Solidify USD Downside Protection

Fed to support further USD comeback?

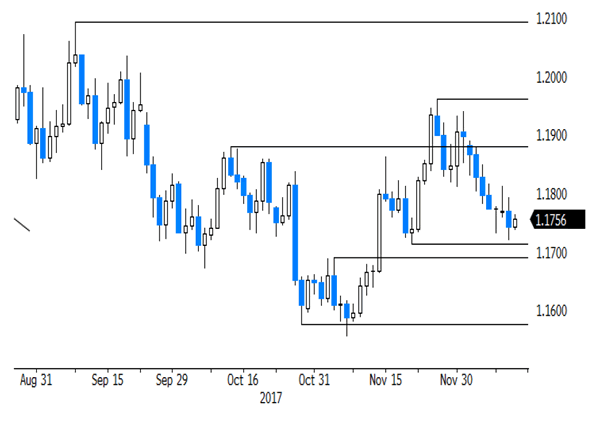

Markets showed no clear trend in Europe yesterday. A strong NFIB small business confidence and a higher than expected PPI finally tilted the intraday balance in favour of the dollar. EUR/USD even touched a minor ST correction low but moves remained modest ahead of today’s Fed decision. The dollar rally slowed at the end of the day as the US equity rally stalled. EUR/USD closed the day at 1.1742. USD/JPY failed to sustain earlier gains and finished almost unchanged at 113.55.

Asian equities opened mixed, but found a better bid later in the session. Most indices are currently trading in positive territory. Japan core October machine orders were strong (5.0% M/M), but it doesn’t help Japanese equities. They underperform as USD/JPY lost further ground. The US currency is in the defensive across the board as the Republican party lost the Senate vote in Alabama, reducing its majority in the Senate to a slim 51-49. USD/JPY spiked to the 113.15 area upon the US election headlines. The pair trades currently again near 113.30. EUR/USD also rebounded overnight and trades near 1.1760.

The eco calendar contains EMU production data and US CPI. US headline CPI is expected to rise 0.4% M/M and 2.2% Y/Y (from 2.0%). Core CPI is expected at 0.2% M/M and 1.8% Y/Y (unchanged from October). The report might cause some intraday jitters in case of a surprise, but investors will remain cautious to place directional bets just hours before a key Fed meeting. The Fed is largely expected to raise its policy rate by 25 bps. We expect the dots to confirm a scenario of 3 rate hikes 2018 and 2 hikes in 2019. We don’t see a strong reason for Fed governors to lower their rate expectations. Eco data remain strong and the chances on additional fiscal stimulus are growing. Dots indicating three rate hikes next year should be slightly supportive for the dollar. However, of late, interest rate markets already moved closer to this Fed scenario. It might nevertheless help to solidify USD downside protection. However, we don’t expect a spectacular jump higher. For that the happen, markets probably need further confirmation on a next rate hike in March. Even so, EUR/USD should be able to break 1.1713 support. Aside from the Fed decision, there will be plenty of headlines on the outcome of the Senate vote in Alabama. We don’t expect this issue to have a lasting impact on markets.

From a technical point of view: EUR/USD set a post-ECB low mid-November, but the dollar’s momentum wasn’t strong enough. EUR/USD settled in a directionless sideways consolidation pattern in the 1.17/19 area. A return below 1.1713 would signal an improvement in the ST USD momentum. The payrolls were unable to force this break. EUR/USD still gives no clear directional signal. Next support comes in at 1.1554 (November low). USD/JPY’s momentum deteriorated early November, dropping below the 111.65 neckline. No aggressive follow-through selling occurred though. Over the previous two weeks, the pair succeeded a nice rebound, calling off the downside alert and returning to the 110.84/114.73 consolidation range. We amended our ST bias from negative to neutral. We maintain the view that a sustained break north of 115 won’t be easy.

EUR/USD: USD to extend gradual rebound after Fed decision?

EUR/GBP

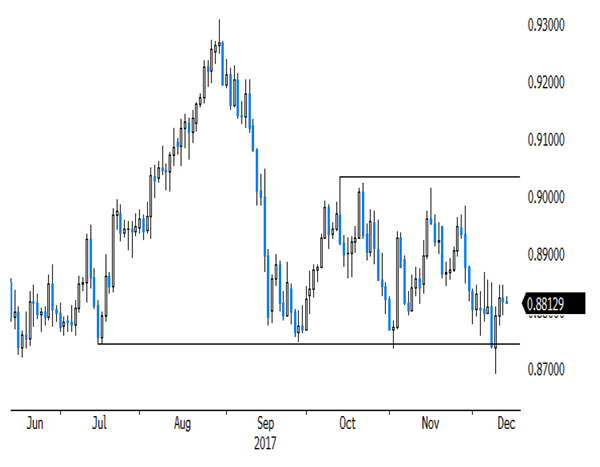

EUR/GBP settled in the 0.88 area

Sterling showed a diffuse picture yesterday. Headlines from UK government members suggesting that last week’s Brexit was not legally binding caused quite some nervousness amongst EU officials. Sterling started with a slightly negative bias, but the move had no strong momentum. UK headline inflation was higher than expected at 3.1% Y/Y. Sterling showed some nervous swings after the publication of the report, but still didn’t capture a clear trend. EUR/GBP finally declined to the 0.88 area, partially inspired by the intraday decline of EUR/USD. The pair closed the session little changed at 0.8816. Cable developed an erratic trading pattern in in the mid-1.3318.

Politics/Brexit will continue to create headlines today. UK policy makers apparently turn a bit more cautious in their comments ahead of this week’s EU summit. In the UK Parliament, the voting on the UK separation bill continues. It will be interesting to see whether the UK Parliament will get a more important role in the final approval of the Brexit agreement. UK labour market data will be published. Employment is expected to decline (-40k). Average earnings ex-bonus are still expected at a low 2.2%. Sterling momentum eased since Friday’s Brexit deal. We don’t see a trigger from a sustained GBP-rebound anytime soon.

Recent developments pushed EUR/GBP lower in the 0.8690/0.9033 consolidation pattern. EUR/GBP tested 0.8693 support (62% retracement) on Friday, but the test was rejected. Next support comes in at 0.8653. We assume that the 0.8653/90 area won’t be easy to break short-term. We hold a neutral bias on EUR/GBP short-term. We consider a return to the bottom of this range as an opportunity to reduce sterling long exposure against the euro

EUR/GBP rebounds in the established trading range despite Brexit deal