Summary

U.S. Week In Review

- The February jobs report was uniformly negative. Nonfarm payrolls slipped by 92K, labor force participation declined and the unemployment rate ticked up to 4.4%. Yet, increased productivity growth remains a green shoot amid increasingly apparent labor market deterioration. Control group retail sales also suggested that consumer spending remained buoyant in January.

U.S. Week Ahead

- Incoming inflation data are likely to confirm that price growth remains stubborn. We expect real disposable income growth to continue to run behind real consumption growth in January, underscoring that the wind at the household sector’s back has weakened.

U.S. Week in Review

We published a note early this week detailing our thoughts on how the Iran conflict might influence the U.S. economy. Our best judgment is that the effects on domestic inflation are likely to be modest. However, much remains uncertain as brent crude futures currently trade at around $90 per barrel. Even if tail risks do materialize, for example, if the conflict lasts longer than expected or oil shipments cannot travel safely through the Strait of Hormuz, this global supply shock should not materially alter the Fed’s reaction function.

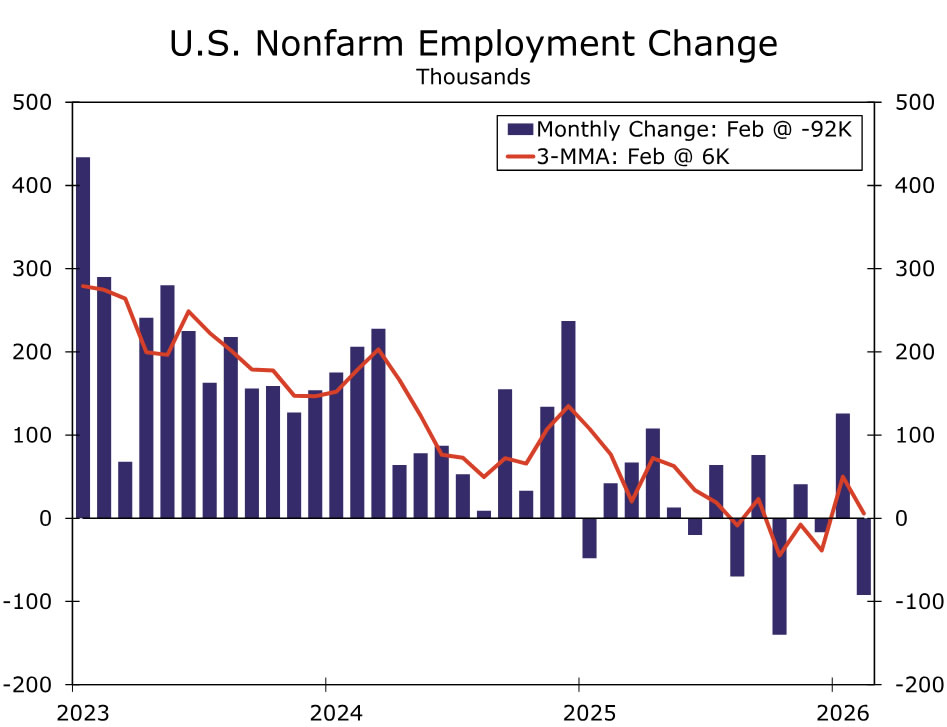

What is top of mind at the FOMC is the underlying stability of the labor market. This morning’s nonfarm payroll report was uniformly negative. The labor market shed 92K jobs in February, a significant downside miss compared to economist expectations. Payrolls over the prior two months were also revised down by a cumulative 69K, bringing the three-month average payroll gain to just 6K. Nearly every major industry shed headcount in February. Even health care & social assistance, this cycle’s mainstay driver of labor demand, experienced giveback. The household survey was similarly weak as the unemployment rate ticked up to 4.4% and the labor force participation slid by half a percentage point to 62.0% on revised population estimates.

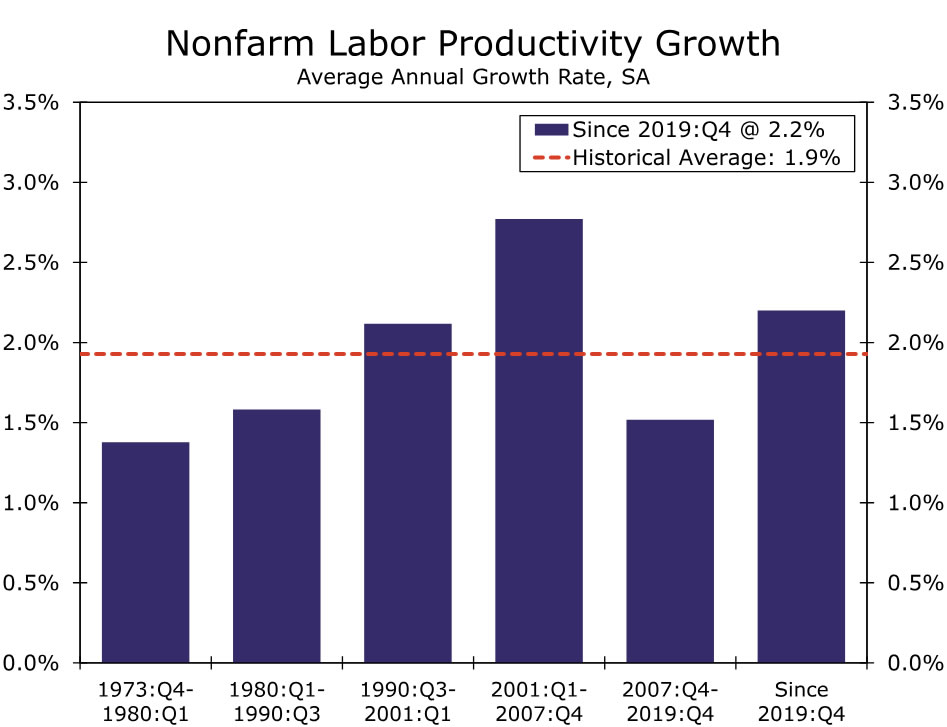

Increased productivity growth remains a green shoot amid increasingly apparent labor market deterioration. Nonfarm business productivity rose at an annualized 2.8% rate in Q4, surpassing economist expectations and adding to the above-average trend observed since the pandemic. Unit labor cost growth also accelerated over the quarter. But through the noise, the underlying trend in productivity-adjusted labor costs remains consistent with the Fed’s 2% inflation target.

Retail sales dipped 0.2% in January. Keep in mind that this week’s print was unusually lagged due to the government shutdown. The underlying details were also a bit stronger than the headline suggests. Stripping out weakness from gasoline stations and auto dealers, control group sales rose 0.4% accompanied by upward revisions to prior data. This does not necessarily mean that we expect consumers to go gangbusters over the next few months; poor winter weather and subdued credit card data point to another weak print in February. However, we do expect retail sales to show more material signs of life as larger tax refunds start to filter through in March.

The ISM indices painted a more resilient picture of economic activity. The February ISM Services index rocketed to its highest point in three and a half years, supported by a broad-based demand improvement across industries. Meanwhile, its manufacturing counterpart remained above 50 for the second straight month, marking the first two-month expansionary string since mid-2022. Firms across the board reported healthier new orders and production. Both sectors also reported growing backlogs to support future activity.

One potentially troubling development was a near-12-point jump in prices paid by manufacturers. Upon further inspection, this leap appears tied to steel and aluminum tariffs raising the cost of industry metals. Recall that the Section 232 tariffs on steel and aluminum have a firmer legal justification than the IEEPA tariffs recently rolled back by the Supreme Court. However, the ultimate transmission of higher metals costs to consumer prices is likely to be minimal.

U.S. Week Ahead

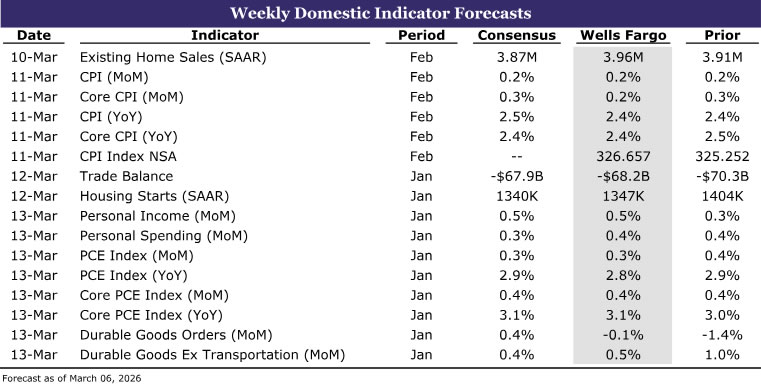

Monday • Existing Home Sales

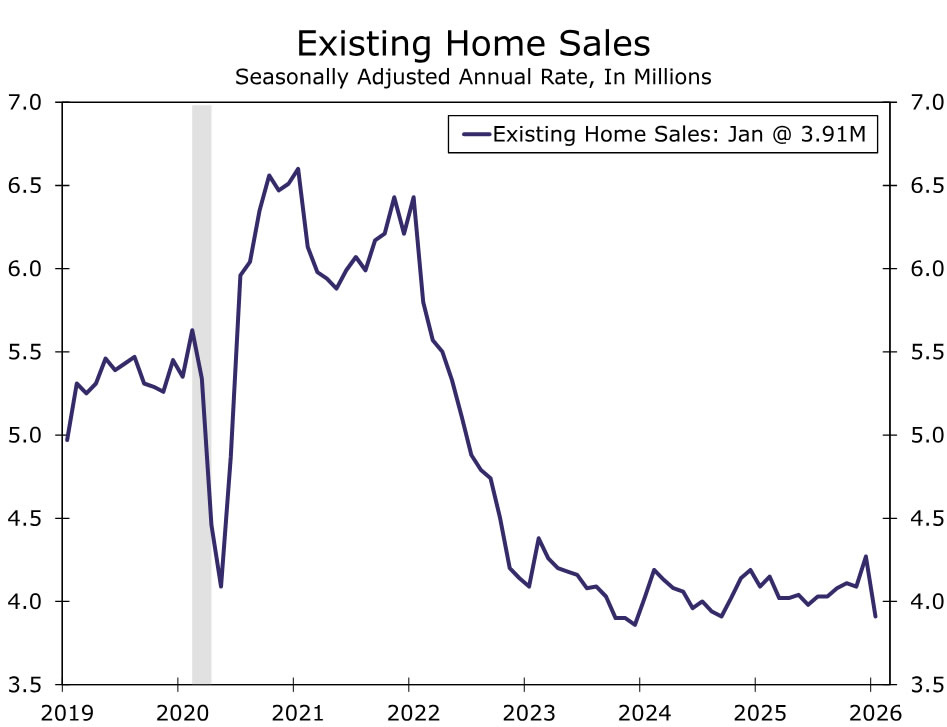

Existing home sales likely regained some footing in February after a weather-related drop in January. We forecast resales strengthened to a 3.96 million-unit annualized pace. Marginally improved affordability and slightly better inventory conditions likely aided sales over the month, but there are numerous headwinds likely to restrain the housing market this year.

After briefly dipping below 6.0%, mortgage rates have moved up to 6.1% according to Mortgage News Daily. Looking ahead, home buyer financing costs are unlikely to fall further. Home price appreciation is also starting to pick up again after moderating over the past year. At the same time, household income growth is under pressure. Homeownership costs thus still consume over 40% of median income, illustrating that affordability conditions are far from favorable. We expect ongoing supply constraints and elevated borrowing costs to continue to weigh on activity, pointing to a gradual, rather than robust, recovery in existing home sales as 2026 unfolds.

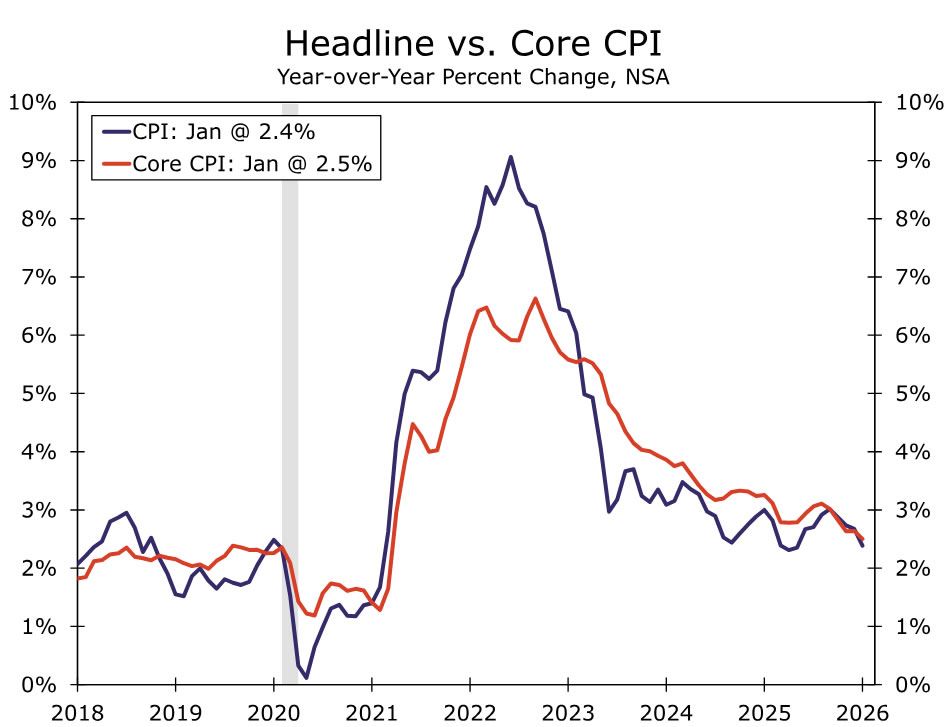

Tuesday • Consumer Price Index

February’s CPI report is likely to underscore that progress on disinflation is stalling out again. We expect the headline CPI rose 0.21% in February, a touch firmer than January. Energy is set to reassert upward pressure on overall prices, as oil and gasoline prices were already rising in February in anticipation of a conflict in the Middle East. Softer food inflation should offer a partial offset, with grocery prices due for a modest decline over the month.

Core CPI is expected to moderate to a 0.19% gain, led by some payback in services after outsized increases in travel and medical care in January. That said, core goods inflation likely firmed, reflecting higher used vehicle prices and ongoing tariff pass-through to consumers. Taken together, we forecast both the headline and core CPI rose 2.4% on a year-over-year basis in February. For more detail, see our February CPI Preview.

Friday • Personal Income and Spending

January’s personal income and spending report should continue to show a consumer that is holding up reasonably well despite persistent uncertainty and deteriorating confidence. We forecast personal income rose 0.5% in January, reflecting still-solid wage growth and annual adjustments to social security payments. Personal spending is expected to increase 0.4%, consistent with continued resilience in services outlays even as growth in discretionary outlays remains muted.

Beneath the headline, inflation remains uncomfortably stubborn. We expect real disposable income growth to continue to run behind real consumption growth in January, underscoring that the wind at the household sector’s back has weakened. That said, favorable tax provisions from the One Big Beautiful Bill Act should provide a meaningful tailwind to household income this spring and help support consumption in the coming months.

{kind=link}