- Recession is not our base case, but we believe the risk distribution has shifted decisively to the downside, as oil briefly broke above $110/barrel and remains volatile. The U.S. economy does not enter the current oil price shock from a position of robust strength. With headline inflation on its way back above 3% as soon as this month, higher oil prices add a new headwind at a moment when the U.S. economy’s margin for error is narrow.

- Recessions ultimately reflect broad and persistent declines in activity. An oil price shock becomes recessionary when it turns a slowing expansion into a self-reinforcing downshift: real income falls, consumption growth slows, investment contracts, hiring weakens, and income declines further.

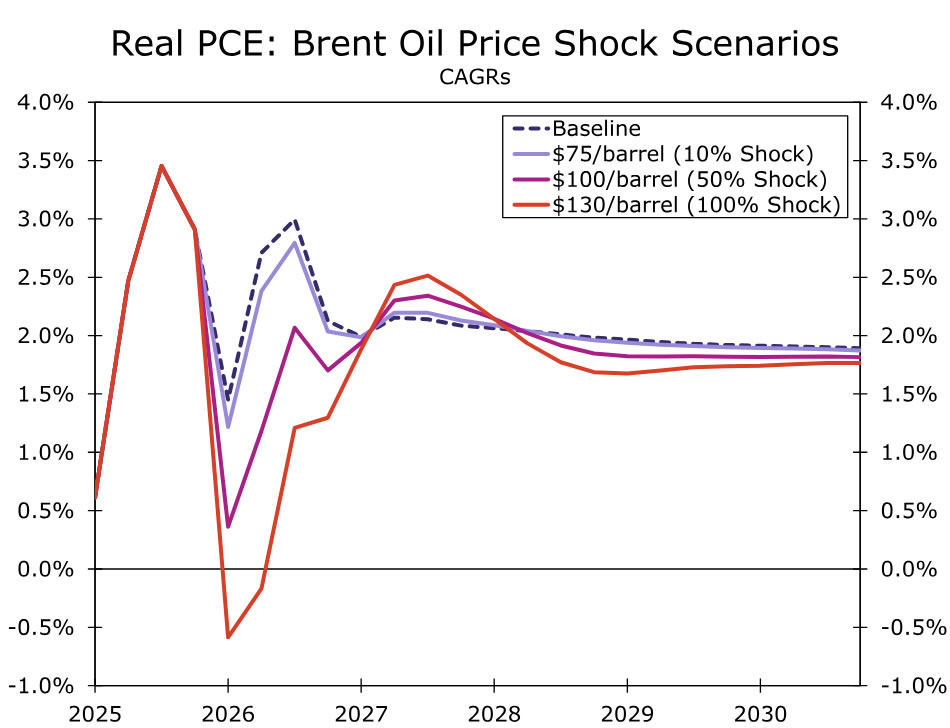

- Our model simulations suggest that a 50% sustained increase in oil prices would reduce annual average growth of real personal consumption expenditures (PCE) by a full percentage point—more than offsetting the expected boost to consumer spending from the One Big Beautiful Bill’s household tax cut provisions.

- In an additional modeling exercise, sustained oil prices at $130/barrel, which is a ~100% increase from the pre-conflict baseline, would lead to back-to-back contractions in quarterly PCE in the middle part of this year.

- Higher oil prices tend to provide a boost to business fixed investment, primarily through increased energy-sector spending. This energy investment impulse is layered on top of a structural capex boom tied to the generative AI build-out, which has been relatively insensitive to energy costs and broader macro volatility.

- Moderate increases in oil prices tend to reallocate growth, rather than eliminate it: consumer spending slows, but investment accelerates, helping to stabilize aggregate demand. However, this offset is neither full, nor immediate.

- As a net energy exporter, the U.S. economy can better weather higher oil prices than many other countries, but sustained prices north of $130/barrel would materially raise the risk of recession.

The Economy Is Vulnerable to an Oil Shock Right Now

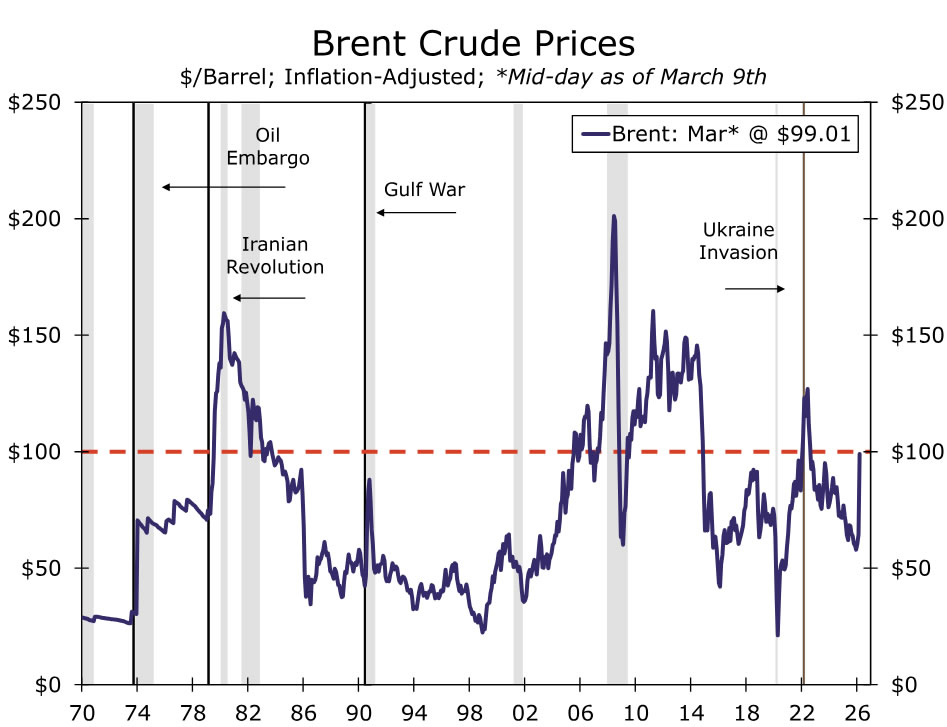

With intraday oil prices nearly hitting $120/barrel over the past day (and then receding almost as fast), we know some folks are wondering about potential downside economic risks. So let’s talk about it. To be clear, it seems very premature to notably alter recession odds at this juncture (given the volatility of oil prices mentioned a moment ago, that seems practical). But that shouldn’t stop us from talking about risks associated with big upswings in oil (Figure 1) and providing a roadmap of sorts.

The reality is the U.S. economy does not enter the current oil shock from a position of robust strength. Payroll growth remains soft at best, the unemployment rate is modestly above most estimates of full employment, and real income growth was already under pressure before energy prices moved higher. With headline inflation on its way back above 3% as soon as this month, higher oil prices add a new headwind at a moment when the margin for error is narrow.

As we flagged in our FAQ last week, the longer prices stay elevated, the greater the downside economic hit becomes. Stated differently, the left tail grows fatter the longer prices rise and stay elevated. So from our lens, the relevant question for markets is no longer whether higher oil prices are “bad for U.S. growth,” but what conditions would be required for an oil shock to push a fragile expansion into outright recession?

Recessions ultimately reflect broad and persistent declines in activity. An oil shock becomes recessionary when it turns a slowing expansion into a self-reinforcing downshift: real income falls, consumption growth slows, investment contracts, hiring weakens, and income declines further.

The Three Conditions that Typically Turn an Oil Spike into a Recession

1) The jump in oil prices is high enough to force real income to contract

- A sustained rise in energy prices mechanically weakens real income growth, especially when wage growth is already slowing and hiring is soft, as it happens to be right now.

2) The shock persists long enough to spread beyond energy

- One-off spikes hit sentiment and headline inflation, but recessions usually require months of pressure that force households to change behavior and businesses to revise staffing and capex plans. Put differently: the economy can “absorb” a spike; it struggles with a new, sustained higher plateau.

3) Spillovers tighten broader financial conditions

- The most dangerous pathway is not just the direct energy price spike—it’s the second-order effect: higher inflation expectations, weaker sentiment, and tighter financial conditions that make investment harder and ding household consumption, particularly for the higher income cohorts currently driving spending growth. Market concerns about growth have the potential to become self-fulfilling by choking off the confidence/wealth channel and turn what has already felt like a recessionary environment for many Americans into an actual recession.

Modeling the Consumer Impact: Some Wiggle Room, but Not Limitless

Most households devote a relatively small share (less than 3%) of their budgets directly to gasoline and other energy goods, but these are expenditures that are difficult to curtail when prices rise. As seen in Figure 2, our model simulations suggest that a 50% sustained increase in oil prices would reduce the annual average pace of real personal consumption expenditures (PCE) by a full percentage point—more than offsetting the expected boost to consumer spending from the One Big Beautiful Bill’s household tax cut provisions.

Even so, a larger oil price shock would need to be sustained to generate a contraction in aggregate consumer spending that is typically associated with recession. While real retail and wholesale sales are near stall speed, broader consumption has remained more resilient in recent months, supported by the growing dominance of services spending, demographic dynamics (e.g., more spending on healthcare), and income concentration among higher income households. In an additional modeling exercise, sustained oil prices at $130/barrel, which is a ~100% increase from the pre-conflict baseline, would lead to back-to-back contractions in quarterly PCE in the middle part of this year.

Modeling the Investment Impact: A Partial Offsetting Boost

Higher oil prices tend to provide a boost to business fixed investment, primarily through increased energy-sector spending. Rising prices improve project economics, lift cash flow for producers and incentivize new drilling, infrastructure, and related capital outlays.

In the current cycle, this investment impulse is layered on top of a structural capex boom tied to the generative AI build-out, which has been relatively insensitive to energy costs and broader volatility. As a result, moderate increases in oil prices tend to reallocate economic growth, rather than eliminate it: consumer spending slows, but investment accelerates, helping to stabilize aggregate demand.

However, this offset is neither full, nor immediate. The hit to household purchasing power occurs quickly, while investment responds with a lag. More importantly, the investment response does not scale one‑for‑one with oil prices, meaning we would not expect the pick-up in energy-related investment spending to offset fully the loss in household purchasing power.

Bottom Line: Recession Risks Elevated

Oil shocks do not automatically produce recessions. They become recessionary when they persist, compress real incomes, and trigger spillovers that feed back into employment and financial conditions. The key takeaway for markets is the non-linearity of the risk: moderate oil price increases slow growth; sufficiently high and sustained prices can overwhelm the offsets and tip the economy into recession. The question is not whether oil matters—but how high, and for how long. As a net energy exporter, the U.S. economy can better weather higher oil prices than many countries. But, sustained prices north of $130/barrel would materially raise the risk of recession.

A Practical “Recession Checklist”:

- Oil stays elevated long enough to push up headline inflation and produce outright declines in real incomes.

- Consumption rolls over in back-to-back quarterly declines, which our model suggests can occur around $130/barrel.

- Financial conditions tighten in a way that hits investment spending and higher income consumption, turning the current bifurcated consumption pattern into a broader downshift.

- Prices climb to a level where the boost to energy-related capex no longer offsets the broad hit to household spending.

When all four are checked—especially #2 plus #3—the probability of recession rises materially.

{kind=link}