Stagflation risks have risen since the FOMC last met in January. Higher inflation and a weaker labor market is the FOMC’s worst nightmare as it puts the dual mandate in tension. How will Chair Powell and company balance these risks?

We expect the FOMC to hold rates steady and maintain maximum flexibility. It goes without saying the conflict in Iran has a highly uncertain outlook, with oil prices gyrating wildly in response to the uncertainty. Looking past the geopolitical whirlwind, key data from the monthly jobs report whipsawed over the inter-meeting period, with strong job gains and lower unemployment in January offset by a train wreck of a February jobs report. On net, labor market conditions appear little changed: lukewarm and still muddling along.

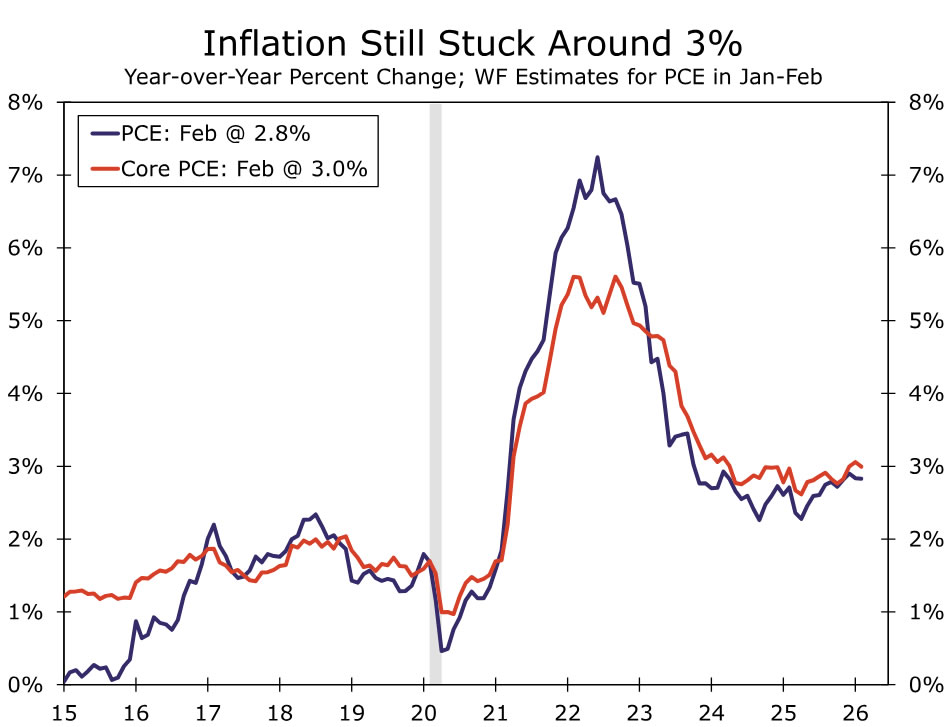

There has been no further progress toward 2% inflation over the inter-meeting period. Recent data point to PCE inflation remaining stuck right around 3% (chart). The energy shock will strengthen headline inflation and have a small pass-through to core but also crimp economic growth.

Fed speak has been mixed. Governors Miran and Waller are likely unconvinced that the labor market is stabilizing and probably want to “look through” the supply-side oil shock—a view for which we have plenty of sympathy. But, with inflation entering its sixth year and counting above 2%, there are signs some of the Committee’s hawks are digging in amid yet another inflationary shock.

The post-meeting statement probably won’t change dramatically. We expect it to highlight additional uncertainty in the outlook due to the Iran conflict. We also would not be surprised if the language around “some signs of stabilization” in unemployment is tweaked to be a bit more pessimistic.

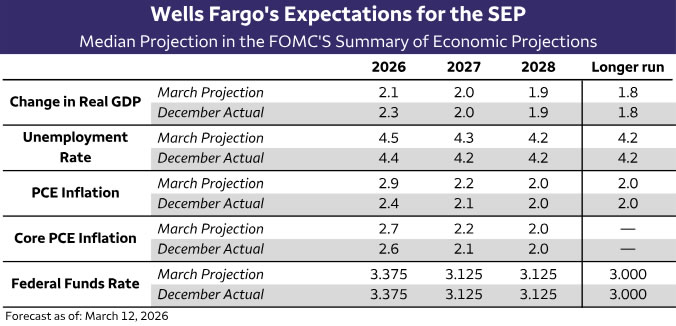

The SEP will shift in a stagflationary direction: We expect the FOMC’s inflation projections to be revised up, in part due to higher energy prices and in part due to recent strength in some core PCE components. The slightly stickier picture of inflation is likely to carry through to 2027 and keep the anticipated return to 2.0% two years away. GDP projections for 2026 are likely to be lower but still consistent with above-trend growth. Median estimates for the unemployment rate are likely to edge up as the low hire/low fire environment drags on. Our point estimates for the March SEP can be found in the table on the next page.

“First, do no harm” keeps median dots unchanged. It would take two dots moving down to drop the 2026 median from 3.375% to 3.125% and three moving higher to shift the median projection up to 3.625%. With estimates for inflation drifting up but growth projections shifting down, we think the net impact will be no change to the median dots. From a balance of risks standpoint, our hearts lie with a downside surprise in the dots. Yet our heads think it will be very difficult for the dots to surprise in the dovish direction as inflation worries escalate, even if it is a supply shock that monetary policy is poorly equipped to solve. Our own forecast remains for two 25 bps rate cuts in June and September.

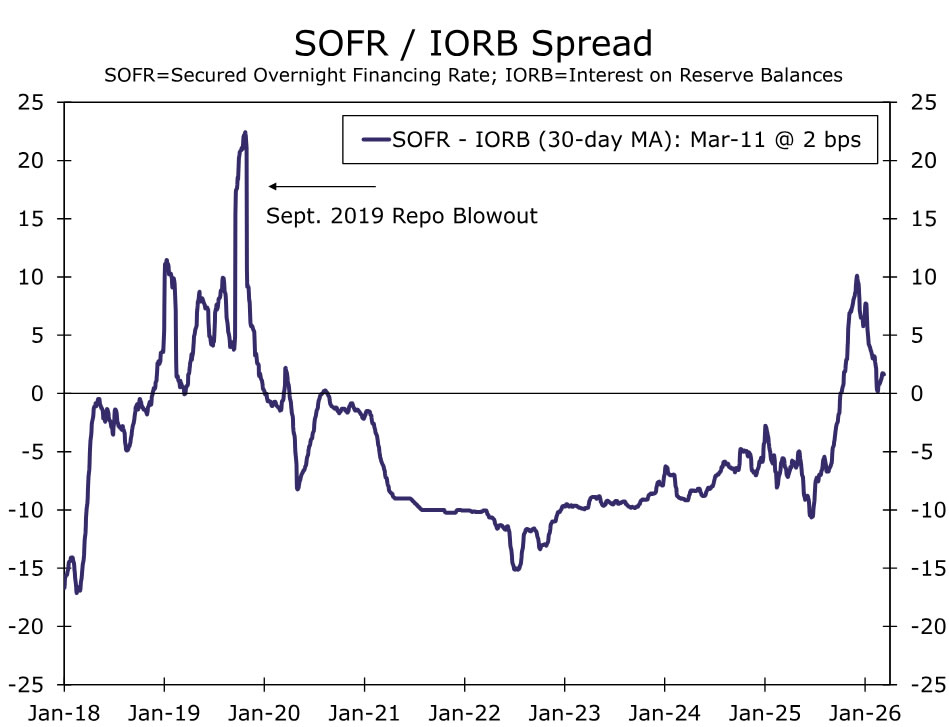

We expect the Fed to slow reserve management purchases to a $20-$25 billion/month pace. This would be a slowdown from the current $40 b/mo pace and has been well-telegraphed by Fed officials. The downshift is in response to funding markets returning to a more stable equilibrium (chart). Since the Fed has been buying exclusively Treasury bills, this should not have a material impact on longer-term interest rates.

{kind=link}