- The Bank of England kept the Bank Rate unchanged at 3.75%.

- In a hawkish surprise, the decision was taken unanimously.

- We continue to pencil in two more rate cuts but kick them further down the road to July 2026 and February 2027.

- Gilt yields traded higher following the decision and also drove a move higher in Bund yields.

The Bank of England (BoE) kept the Bank Rate unchanged at 3.75% as expected. The decision was unanimous, something we have not seen since 2022. This was a hawkish surprise, as two members, probably Taylor and Dhingra, were expected to keep their votes for cut. The statement also leaned to the hawkish side, as “The MPC is alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which will be greater the longer higher energy prices persist.”.

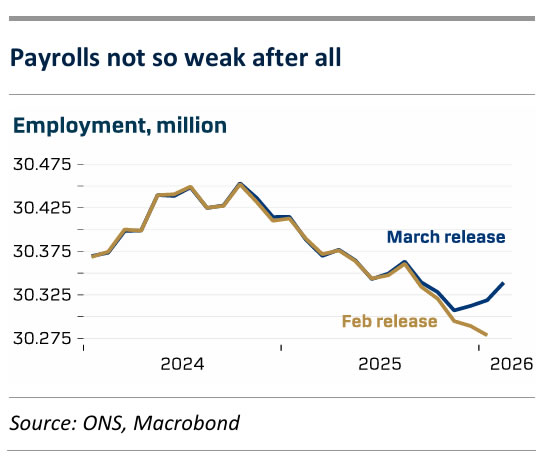

For now, the war in the Middle East blurs the disinflationary path in the UK, which makes the next move from the BoE more uncertain. This morning did bring some comforting news to MPC members from the labour market, suggesting the UK economy can handle a potential delay of the final part of the cutting cycle. The labour market report shows a significantly more upbeat jobs situation with payrolls increasing 20K in February and recent months also lifted markedly. At the same time, January unemployment declined markedly, which erases the worst fears from the weak November/December prints. Also encouraging to the BoE, wage pressures are abating suggesting a still smaller underlying price pressure. That said, the MPC notes that CPI inflation is now expected around 3% in Q2 rather than 2.1% in the February Report.

BoE call. We judge it most likely that energy markets will continue to blur the inflation picture over the coming months. Even if energy prices normalise through April and May, the BoE will likely not know enough about second round effects by mid-June. We deem it more likely they wait for the July meeting to cut rates again. By then, they can also support such a call with a fresh take on the economy in a new outlook report. We call for two more rate cuts, in July 2026 and February 2027.

Market reaction. 2-year Gilt yields traded some 20bps higher on the back of the decision and at the time of writing, investors price in two hikes through the remainder of 2027. It remains to be seen what a more hawkish BoE means for the UK economy, which is probably also why EUR/GBP did not move much.

kept the Bank Rate unchanged at 3.75% as expected. The decision was unanimous, something we have not seen since 2022. This was a hawkish surprise, as two members, probably Taylor and Dhingra, were expected to keep their votes for cut. The statement also leaned to the hawkish side, as "The MPC is alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which will be greater the longer higher energy prices persist.".){kind=link}