Friday March 24: Five things the markets are talking about

Markets remain in "wait and see mode" – Can Trump’s self-proclaimed "infamous" negotiation skill push through his health care bill?

This bill is viewed as a potential bellwether for his ability to impose his economic and political agenda.

Thus far, delayed is better than defeat. Investors regard today’s healthcare bill vote as "the" test for the Trump presidency. The GOP pulled the healthcare bill vote late yesterday afternoon to hold more meetings with the holdout Freedom Caucus. However, there is still lack of clarity in whether the White House has been able to appease the hard-right opponents with an amendment that does away with "essential benefits" clause while preserving the support of the moderates.

Net result, Trump’s reflation trade has struggled this month as the administration remains far from delivering on pro-growth policies that boosted stocks and the dollar.

On the radar, more Fed officials are lined up for today, including Fed Bank of St. Louis President James Bullard, who will speak to the Economic Club of Memphis.

1. Japanese equities lead gains in Asia Pacific, Europe neutral

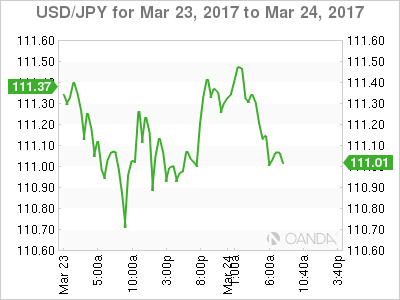

Despite losing -1.3% on the week, Japan’s Nikkei has ended up +0.9% overnight and has moved decisively away from the previous session’s two-month lows. The broader Topix index has also recovered some of this week’s slide as the yen (¥111.18) halted its longest rally outright in six-year.

In Hong Kong, stocks have eked out marginal gains as investors wait for corporate earnings and today’s U.S healthcare bill vote. The benchmark Hang Seng index added +0.1%.

In China, stocks have rallied for a second week as infrastructure spending has offset liquidity fears. The blue-chip CSI300 index rose +0.8%, while the Shanghai Composite Index added +0.6%.

In Europe, equity indices are trading lower as the market remains nervous ahead of U.S healthcare vote. Financials are leaning on Eurostoxx, while commodity and mining stocks are trading higher in the FTSE 100.

Overnight, U.S. stock futures have rallied (+0.2%) now that Republicans said the House was ready to vote on an amended health-care bill.

Indices: Stoxx50 -0.3% at 3,442, FTSE -0.1% at 7,336, DAX flat at 12,035, CAC-40 -0.3% at 5,017, IBEX-35 -0.4% at 10,288, FTSE MIB -0.2% at 20,134, SMI -0.2% at 8,613, S&P 500 Futures +0.2%

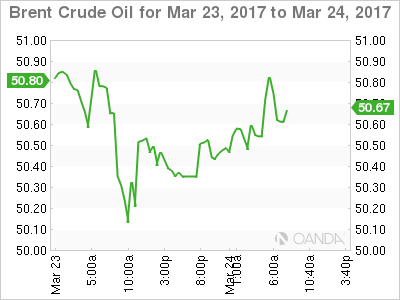

2. Saudi’s cut oil supply to the U.S

Oil prices have edged a tad higher overnight, supported by a fall in Saudi exports to the U.S, however, the market remains under pressure from a supply glut.

Brent crude futures at +$50.69 per barrel are up +13c or +0.3% from yesterday’s close. U.S. West Texas Intermediate (WTI) crude futures are up +18c, or +0.4%, at +$47.88 a barrel.

On the week, Brent is heading for a weekly fall of about -2%, while WTI is off -1.8%.

Support has come from the Saudi’s who indicated that crude exports to the U.S would fall by around -300k bpd between February and March.

Note: Saudi exports are competing with U.S shale production, which is up about +9% in the past 18-months.

Currently, the market believes that OPEC needs to extend its production curbs beyond June or makes bigger cuts or oil prices are at risk of falling much further.

Note: Despite the OPEC-led cuts that began three months ago, Brent has fallen by over -13% now that other producers have stepped up and filled the gap.

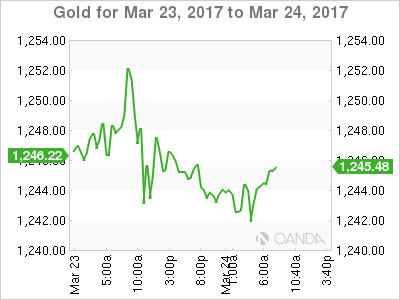

Gold prices have edged lower overnight (-0.2% at +$1,242.31 per ounce) on the back of a stronger dollar. Today’s healthcare vote defeat will affect Trump’s efforts to cut taxes and boost infrastructure and should drive more investors to gold as a safe haven.

3. Global yields need guidance

With market risk sentiment being somewhat fragile given the uncertainty on whether Trump can deliver on stimulus expectations has been supporting U.S treasuries and bunds prices this month.

In the U.S, 10-year yields rose above +2.6% earlier this month and reached a two-year high as investors anticipated the Fed would raise short-term interest rates. They did last week, but its signal of a "gradual" path of tightening policy has debt product better bid. U.S 10’s are trading at +2.43%. German bunds are trading just above +0.5%.

In the U.K, yields on 10-year gilts have backed up +1 bps to +1.19% after data showed yesterday showed that U.K retail sales rose beating expectations.

Elsewhere, the Reserve Bank of New Zealand (RBNZ) held rates steady Wednesday (+1.75%) as expected and maintains a neutral policy stance. In its policy statement, officials expressed more concern over housing inflation while reiterating that the exchange rate should depreciate more to achieve balanced growth.

The yield on Aussie 10’s are little changed at +2.75%.

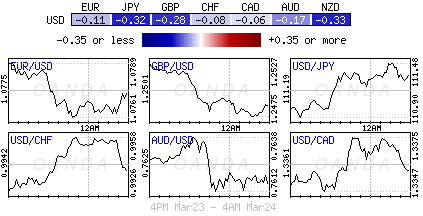

4. Dollar waiting for vote outcome

Currently, FX price action and risk outlook continues to hinge on President Trump’s healthcare bill vote this afternoon (no time set).

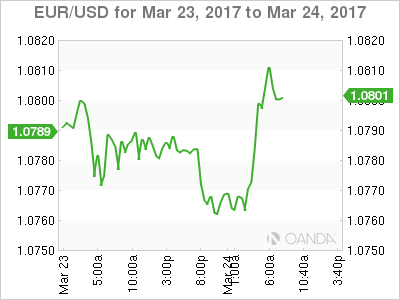

The EUR is trading back above the psychological € 1.0800 handle (€1.0810) supported by today’s EU Manufacturing PMI print (see below) exceeding expectations and rallying further into expansion territory to new multi-year highs.

The pound is a tad lower (£1.2483) in quiet trading. Next week PM Theresa May is expected to begin divorce proceedings from the EU.

USD/Yen has moved off yesterday’s lows to stay above the psychological ¥111.00 handle. It’s the first day that the ‘mighty’ dollar has rallied in eight days.

5. Eurozone Composite PMI Highest in Six Years

Data this morning shows that the Eurozone grew at the fastest pace in six-years in Q1. The PMI for the eurozone’s manufacturers and service providers rose to 56.7 in March from 56.0 in February.

With new orders also surging and businesses hiring additional workers at the fastest pace in a decade, the three monthly average rally may suggest a faster rate of expansion is likely to be sustained over coming months. There were also signs the pickup in activity is fueling inflationary pressures, with prices charged by businesses rising at the fastest rate in six years.

Data like this will have fixed income traders raising their expectations that the ECB should consider moderating its stimulus measures later this year. Market expectations were for a drop.