Here are the latest developments in global markets:

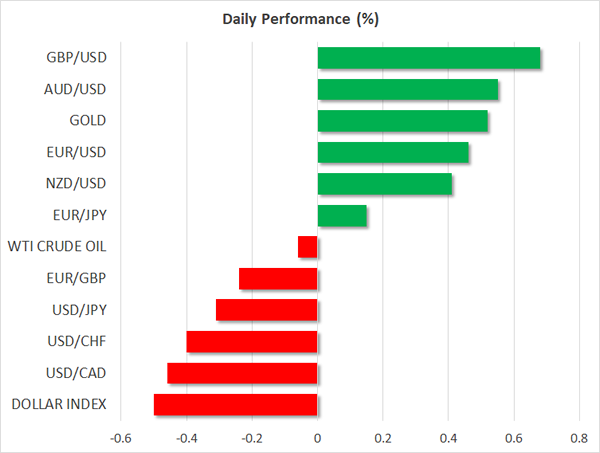

FOREX: The dollar index traded 0.5% lower on Friday, after experiencing heightened volatility earlier on Thursday.

STOCKS: Asian markets were mixed. Japan’s Nikkei 225 and Topix closed 0.2% and 0.3% lower respectively, while in Hong Kong, the Hang Seng was up by an astonishing 1.3%, reaching a fresh all-time high. In Europe, futures tracking the Euro stoxx 50 suggest the index could open 0.3% higher. In the US, the Dow Jones and the S&P 500 continued to march higher, closing at new record highs, though the Nasdaq composite was not as fortunate, ending marginally lower. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently in the green.

COMMODITIES: Oil prices tumbled yesterday, as the greenback regained some poise. Both WTI and Brent crude are lower today as well, albeit only slightly. Despite this pullback, both oil benchmarks are still trading near multi-year highs. In precious metals, gold pulled back yesterday as well, though it recovered most of its losses today, up nearly 0.5%, last trading near the $1355/ounce zone.

Major movers: Euro/dollar trades like a rollercoaster after ECB and Trump’s remarks

Euro/dollar experienced a highly volatile session yesterday. It surged initially on euro strength following the ECB policy decision, only to give back all its gains to trade even lower a few hours later, as the USD gained on some remarks from President Trump. Then, the pair rebounded again early on Friday, as the dollar went back on the defensive.

Kicking off with the ECB, it kept both its policy and its forward guidance unchanged and as such, attention quickly shifted to President Draghi’s press conference. The ECB chief commented on the euro’s appreciation, noting that “recent exchange rate volatility is a source of uncertainty”, but his warning was probably milder than some may have expected. Investors likely anticipated a much more concerned message, and since his tone was only moderate, that may have given them the “green light” to reenter long-euro positions, driving euro/dollar briefly above 1.2500. As for policy signals, Draghi noted repeatedly the progress in Eurozone’s economy, keeping the door open for the Bank to scale back its QE later this year. Interestingly enough, however, he practically eliminated the possibility that the ECB could raise interest rates this year.

Euro/dollar turned down later on Thursday, as the USD surged following remarks from US President Trump that he wants a “strong dollar”. Coming one day after Treasury Secretary Mnuchin said “a weak dollar is good for us”, his comments may have helped to alleviate concerns that the US administration is aiming at a weaker currency. Importantly, President Trump is set to speak again today in Davos, at 1300 GMT. Traders are likely to focus on any further comments on the USD, as well as any hints on protectionism and the latest trade standoff with China.

In Norway, the Norges Bank kept its policy unchanged yesterday as well, providing practically no new policy signals for investors.

Overnight, Japan’s inflation data for December had very little market impact. Even though the headline CPI rate rose, the core rate remained unchanged. This suggests that the progress in the headline print is owed mainly to transitory factors, and enhances the view that the BoJ is unlikely to alter its ultra-loose policy framework anytime soon.

Day ahead: UK & US deliver preliminary GDP growth figures; Canadian inflation pending

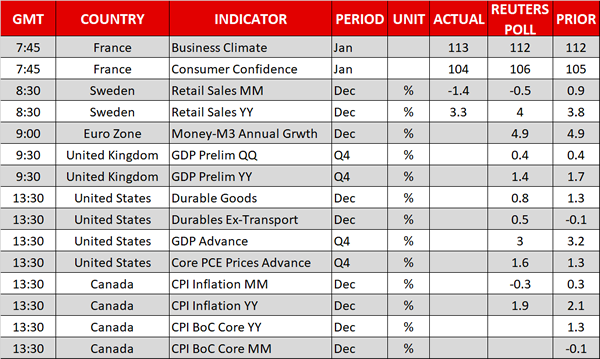

The dollar and the pound will be in the spotlight during the European trading hours as the US and the UK are scheduled to deliver preliminary readings on GDP growth, while in Canada, inflation numbers are expected to shake the loonie. In Australia, markets remained closed for the Australia Day holiday.

At 0930 GMT, the UK National Office for Statistics will publish flash GDP growth stats for the final quarter of 2017, with analysts predicting a slower expansion of 1.4% y/y compared to 1.7% seen in the previous quarter. This would be the lowest growth rate seen since 2013. A surprise to the upside would raise the odds for a rate hike but the general opinion is that the BOE would rather keep rates unchanged at its next policy meeting on February 8 as consumer spending remains subdued in times of high inflation and slow-growing wages.

In the US, initial GDP growth estimates due at 1330 GMT are said to come weaker as well. Expectations are for growth to slow down by 0.2 percentage points to 3.0%, but to remain among the highest levels recorded in 2017. Stronger-than-expected results would help the dollar to erase part of its recent dips. Data on the US durable goods orders for the month of December will be also available along with the GDP report.

Elsewhere, CPI inflation will be in focus in Canada at 1330 GMT. Particularly, analysts forecast the headline inflation rate to slip from 2.1% to 1.9% on a yearly basis in December, while in monthly terms they see consumer prices falling by 0.3% for the first time after rising for four consecutive months. Note that the BOC has raised interest rates at its last policy meeting on January 17 and an unexpected increase in inflation could motivate BOC policymakers to apply further monetary tightening.

In oil markets, the US Baker Hughes oil rig count might bring some volatility to oil prices at 1800 GMT.

Regarding public appearances, the BOE chief, Mark Carney and the BOJ chief, Haruhiko Kuroda will participate at a panel discussion at the World Economic Forum in Davos, Switzerland at 1400 GMT. The US President, Donald Trump will also address the event later in the session after his remarks provided a boost to the dollar on Thursday.

In stock markets, Honeywell International Inc. and Gentex Corporation are among companies to report quarterly earnings before the US market open today.

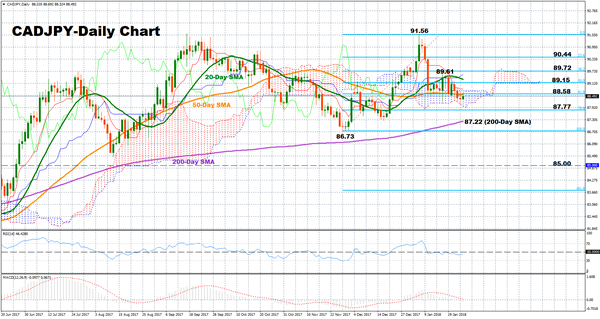

Technical analysis – CADJPY neutral inside Ichimoku cloud

CADJPY stalled its downtrend off a four-month high of 91.56 reached in early January and is currently trading neutral inside the Ichimoku cloud. For the near-term period, the market sends weak bearish signals as the RSI is located slightly below 50, while the MACD has marginally fallen below its trigger line.

Should the pair move lower, support is likely to be found at 87.77, the 78.6% Fibonacci of the upleg from 86.73 to 91.56. The market could also meet the 200-day simple moving average (SMA) at 87.22 before it targets a two-month low at 86.73. Any close below this level would extend September’s downleg towards the 85.00 key level.

On the flip side, if prices rise, immediate resistance could come from the 61.8% Fibonacci at 88.58. However, the pair needs to break above the previous high at 89.61 to turn bullish, while in the best scenario the market could crawl back to the 90.00 key area, shifting focus to 91.56.