Sunrise Market Commentary

- Rates: US yields clear technical hurdles

US yields cleared technical resistance at the 5- and 10-yr tenors last week, suggesting more upward potential medium term. Today’s PCE inflation data are less important than usual as they could be derived from Friday’s GDP release. The eco calendar heats up later this week with the Fed meeting, Trump’s State of the Union and payrolls. - Currencies: Dollar decline halts, at least for now

The USD sell-off eased at the end of last week as US president Trump in some way ‘confirmed’ the US strong dollar policy. This week the focus turns, amongst others, to the Fed policy decision. The Fed turning more optimistic on growth or on inflation, might help to put a floor for the dollar. For now there is no sign of a trend reversal in the USD yet.

The Sunrise Headlines

- US stock markets set another round of record highs on Friday (+1%) and are heading for their best month in over two years as earnings from corporate America continue to impress. China underperforms in Asia overnight.

- Britain is seeking powers to vet new EU laws agreed by the rest of the bloc during the transition period after Brexit day, in a demand that risks setting the UK on a collision course with Brussels.

- There are a number of factors preventing the BoJ from reaching its 2% inflation target but wages and prices are gradually rising and it is getting closer, the governor of the central bank Kuroda said on Friday.

- China’s economic growth will likely slow to 6.5-6.8% this year, a senior official at the country’s top economic planner wrote in the Beijing Daily, while warning about the risks of "Black Swan" and "Gray Rhino" events.

- The ECB has to end its quantitative easing as soon as possible, according to ECB Governing Council member Knot, who said there’s not a single reason anymore to continue with the program.

- Miloš Zeman will serve a second and final term as Czech president, after defeating his pro-EU rival Drahoš in an election that underscored the strength of the backlash against the EU’s multi-cultural and liberal values in central Europe.

- Today’s eco calendar contains US personal income & spending data and PCE inflation numbers. ECB’s Lautenschlaeger and Coeure are scheduled to speak

Currencies: Dollar Decline Halts, At Last For Now

Dollar decline slows going into Fed decision

The dollar entered calmer waters on Friday. US president Trump’s address at the WEF on Friday brought little news on international trade or for the dollar. US data, including Q4 GDP were OK, but failed to inspire trading. EUR/USD drifted back lower in the 1.24 big figure. The yen remained well bid as markets saw a hawkish spin in comments from BOJ’s Kuroda. USD/JPY rebounded off the intraday lows as the BOJ indicated that there was no change in its inflation assessment. USD/JPY finished the day at 108.58 (109.41 on Thursday).

Asian equities opened strong this morning, but the rally loses momentum throughout the session. USD/JPY moves in the upper half of 108. EUR/USD trades close to and mostly just north of 1.24.

US spending and income data will be published today. The data are less relevant for markets as the US Q4 GDP report is already published. Investors will look forward to US president Trump’s State of the Union and Fed’s policy decision on Wednesday and to the early month US eco data, including the payrolls on Friday. Will the Fed upgrade its assessment on growth or on inflation? The tone of US president Trump’s speech might again be a bit more protectionist than in Davos.

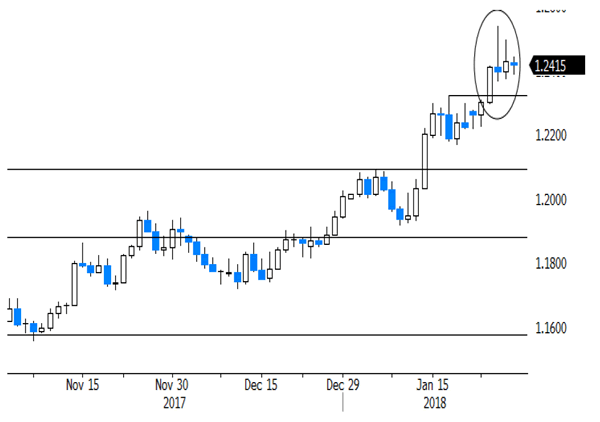

The dollar decline slowed at the end of last week. This process can continue going into the Fed meeting. A modest USD comeback is possible if the Fed turns more optimistic and the US data remain strong. There is no clear technical sign of a sustained USD rebound yet. EUR/USD 1.2537/1.2596 remains the first topside reference. A return below 1.2323 would indicate that the pressure on the USD is easing. A sustained return below 1.2165 would call off the ST alert on the USD.

On Friday, sterling received temporary support from better than expected Q4 growth, but the gain could not be sustained. EUR/GBP finished the session at 0.8780. Today, the EU27 ministers meet to finalize the directives for the Brexit negotiations. There is again more political noise on Brexit in the UK. The sterling rebound lost momentum at the end of last week. The downside test of EUR/GBP was rejected. We put the risk for EUR/GBP to return back higher in the 0.8690/0.9033 range. Intermediate resistance comes in at 0.8928

EUR/USD: rally halted, but no technical sign of a trend reversal