Here are the latest developments in global markets:

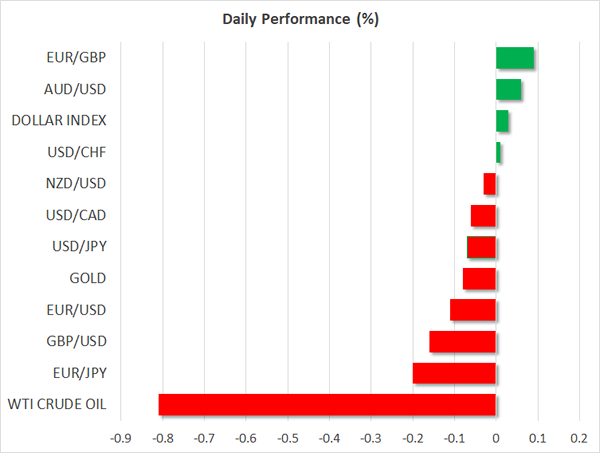

FOREX: The dollar index traded virtually unchanged on Monday, after recovering somewhat on Friday on the back of robust US employment data.

STOCKS: US equity indices collapsed on Friday. The Dow Jones led the plunge, closing lower by 2.5%, while the S&P 500 fell 2.1%. The Nasdaq composite was down by 2%. These gigantic corrections came after the US jobs data for January showed wages accelerating notably, spurring speculation that US interest rates may rise faster than previously anticipated and triggering a surge in US bond yields. As yields rise, bonds begin to offer a better and “safer” return, thereby curbing demand for stocks. This negative sentiment rolled over into Asian trading on Monday, with Japan’s Nikkei 225 and Topix indices being down 2.5% and 2.2% respectively. In Europe, futures tracking the Euro STOXX 50 are currently in negative territory.

COMMODITIES: Oil prices dipped on Monday, with WTI and Brent crude both falling 0.8%, extending the losses they posted on Friday. A stronger US dollar and the broader risk-off market sentiment are being cited as the catalysts for the selloff. The increase in the US Baker Hughes oil rig count on Friday probably didn’t do oil prices any favors either, as it confirmed that US production continues to rise. In precious metals, gold is marginally lower. The dollar-denominated metal tumbled on Friday too, as the greenback recovered.

Major movers: Yields rise on inflation woes, dollar regains ground after jobs data

The dollar regained some lost ground on Friday, following the stronger-than-anticipated US employment report for January. Nonfarm payrolls came at 200k, beating the forecast of 180k, while last month’s print was also revised higher. The unemployment rate held steady as anticipated, though the surprise came from average hourly earnings, which accelerated by much more than expected to reach 2.9% in yearly terms.

The pick-up in wages is monumental for the Fed. Accelerating wages are broadly considered to be a precursor to an acceleration in inflation, as higher wages feed into more spending and therefore higher prices. Considering that inflation has long been the missing piece of the puzzle in an otherwise robust US economy, this development increases the likelihood that the FOMC may deliver three 25bps rate hikes this year, and even opens up the possibility for a fourth. Indeed, markets have now almost fully priced in three hikes in 2018, according to the Fed fund futures.

Now as for the dollar, although it did regain some poise after the US data, it did not advance as much as one would have expected given the strength of the prints. The currency once again seemed unable to draw support from the bond market, where the yields on 10-year US Treasuries surged by 7bps on the day, last trading near 2.86%. The relatively subdued recovery in the greenback is yet another confirmation of just how negative the sentiment surrounding the currency is right now.

Elsewhere, dollar/loonie skyrocketed on Friday. Besides the strong US jobs figures, the surge was fueled by some comments from Canadian Prime Minister Justin Trudeau, who said that his country is willing to walk away from NAFTA. His remarks follow media reports in recent weeks that Canadian officials anticipate the US to pull out of NAFTA soon, and underscore that these negotiations have yet to bear fruit. A potential breakdown in these talks would probably weigh notably on the loonie, as well as the Mexican peso.

Day ahead: US, UK & Eurozone PMIs in focus; Powell takes over as new Fed chair

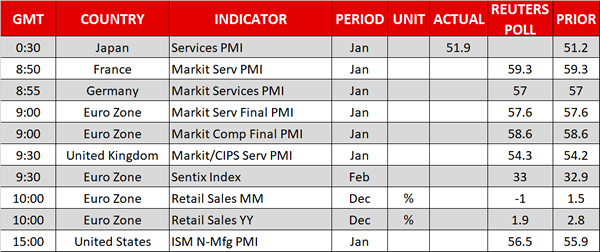

Out of the Eurozone, final PMI readings for the month of January will be released at 0900 GMT, while figures on the Sentix index and retail sales will follow at 0930 GMT and 1000 GMT respectively.

According to forecasts, the Eurozone composite Markit PMI is expected to stand at record highs in January as was initially estimated, rising by 0.5 points to 58.6. However, the euro might show little reaction to these data – unless the index surprises to the upside or downside – as flash estimates tend to be more important for the currency.

On the other hand, the block’s retail sales are said to slow down in December, with analysts anticipating the measure to decline by 1.0% on a monthly basis, driving the yearly gauge lower to 1.9% growth from 2.8% seen in November.

The Sentix index which tracks the six-month economic outlook is projected to inch up by 0.1 points to +33 in February, underlying investor’s strong confidence in the region. The index is fluctuating among the highest scores seen since August 2007.

In the UK, January’s CIPS/Markit PMI for the service industry is expected to come at 54.3 in January, slightly above the previous mark of 54.2. Considering that the services sector accounts for the vast majority of UK GDP, market participants will likely keep a close eye on this print as they try to gauge the economy’s momentum ahead of the Bank of England meeting on Thursday.

Meanwhile in the US, market watchers will be waiting for the ISM non-manufacturing PMI due at 1500 GMT. Following encouraging manufacturing PMI records last week which remained close to the strongest prints seen since 2004 despite a pullback in January, the non-manufacturing PMI is projected to improve to 56.5 in the aforementioned month, compared to 56.0 in December.

Regarding today’s public appearances, Jerome Powell, Janet Yellen’s successor, will be sworn into the position of the next Fed chair at 1400 GMT. Projections are for Powel to follow Yellen’s footsteps by tightening monetary policy even further this year. Later on, the ECB chief, Mario Draghi, will comment on the draft resolution of the European Parliament concerning the 2016 annual ECB report in the European Parliament Plenary in Strasbourg, France at 1600 GMT.

In stock markets, earnings releases will remain in the spotlight.

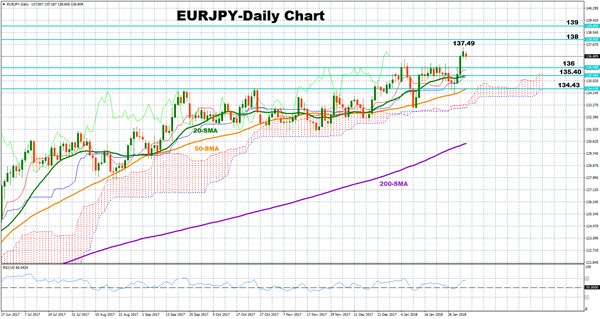

Technical analysis – EURJPY holds at 2 ½ -year highs; maintains bullish bias

EURJPY managed to break above the 137 key-level on Friday, stretching towards a fresh 2 ½ -year high of 137.49. Today, the pair returned to the 136 area but it continues to hold a bullish bias.

Prices remain above the Ichimoku cloud and the moving average lines, which are positively sloped, supporting that the market might maintain its positive trend both in the short and the medium-term. The RSI is also in bullish territory above 50 but has no specific direction, signaling that the pair might consolidate for a while before it resumes its uptrend. The Ichimoku indicators also support this view, with the Tenkan-sen and the Kijun sen being flat.

If the market extends to the downside, immediate support could come from the 136 psychological level, which was a frequently congested area since the beginning of the year. Then the 20-day simple moving average line (SMA) at 135.40 could come into view, while a substantial close below this level could increase bearish actions towards the 50-day SMA at 134.43.

To the upside, the previous top at 137.49 is expected to provide resistance, opening the way towards the 138 and 139 handles.

{kind=link}