{kind=link}

Sunrise Market Commentary

- Rates: Room for consolidation ahead of Wednesday’s FOMC Minutes?

We expect trading to be sentiment-driven and technically in nature today amid an empty eco calendar. Volumes will be low in absence of US traders (President’s Day Holiday). Underlying sentiment remains bearish for core bonds, but we’d argue in favour of some consolidation in the run-up to Wednesday’s FOMC Minutes. - Currencies: USD decline slows, at least for now

The dollar tested key support area’s on Friday, but rebounded later in the session. The econ calendar is thin today. The rebound in equities went hand-in-hand with a weaker dollar recently. Will this link persist? At least this morning, there are tentative signs that it might become less tight

The Sunrise Headlines

- US stock markets ended near opening levels on Friday, but last week’s performance was the strongest in 5 years. Asian risk sentiment is ebullient with China still closed for Lunar New Year.

- A Russian propaganda arm oversaw a criminal and espionage conspiracy to tamper in the 2016 US presidential campaign to support Donald Trump and disparage Hillary Clinton, said an indictment released on Friday.

- China warned it may hit back if the US implements aluminium and steel restrictions as recommended by the Commerce Department on Friday.

- Fitch upgraded the Greek rating from B- to B (positive outlook). Fitch expects reduced political risks, general government primary surpluses and legislated fiscal measures to improve Greece’s general government debt sustainability.

- London’s property market has moved out of its boom phase and home sellers need to be more realistic about their price demands, according to Rightmove. Asking prices were down 1% Y/Y, a sixth consecutive fall.

- Buoyant sales of cars and electronics led Japan’s exports to a 14th straight month of growth in January (12.2% Y/Y). Imports increased by 7.9% Y/Y. The adjusted trade surplus rose more than forecast, to ¥373.3bn.

- Today’s eco calendar contains only second tier EMU eco data. The Eurogroup choses the next ECB vice-president out of Spanish economy minister de Guindos and Irish ECB governor Lane. US markets are closed for President’s Day.

Currencies: USD Decline Slows, At Least For Now

USD decline slows, at least for now

On Friday morning, the dollar remained under pressure, extending the established downtrend. Important USD support in EUR/USD and in the trade-weighted dollar caused USD selling to slow. Gradually, even a modest USD short-squeeze kicked in ahead of the long weekend in the US. US eco data were also again slightly USD supportive, even as we have to admit that didn’t help the dollar much of late. EUR/USD finished the session at 1.2406 (from 1.2506). USD/JPY also rebounded off intraday lows well below 106 and finished the week at 106.21.

Overnight, several Asian markets are closed for the Lunar New Year Holidays. Japanese equities extend their rally. Japanese trade data (both exports and imports) were strong and equities are also supported by a slowing yen rally. USD/JPY tries to regain the 106.50 level. EUR/USD hovers in the low 1.24 area.

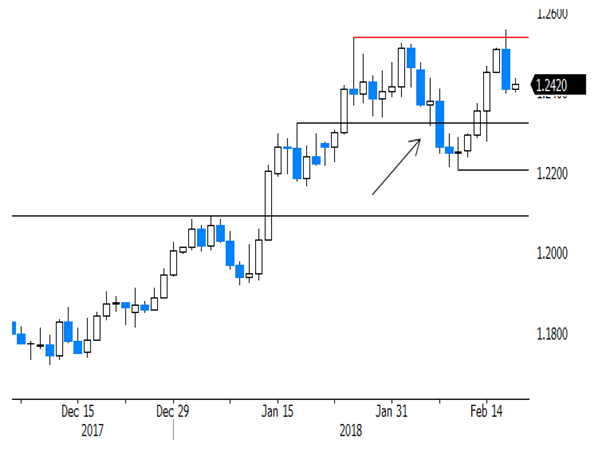

US markets are closed for President’s Day holiday. The EMU eco calendar is thin. At the end of last week, the USD selling finally slowed. With US markets closed, we probably won’t get a clear sign for USD trading. Later this week, the calendar remains uninspiring. The Minutes of the January Fed meeting and CB speeches have most market moving potential. Global risk sentiment remains a factor of importance, too. Of late, the risk rally went hand-in-hand with a USD decline. We look out whether this link holds. There are tentative signs this morning that a positive risk sentiment shouldn’t cause further USD losses. From a technical point of view, EUR/USD 1.2555/98 (correction top, 62% retracement) remains key resistance. A break would indicate more trouble for the dollar. We don’t see a need for such a break because of the economic fundamentals. However, dollar sentiment remains fragile. We keep the working hypothesis for EUR/USD to hold the 1.2598/1.2206 band. A downside break would call of the ST USD alert.

UK retail sales disappointed on Friday, but didn’t hurt sterling much. UK PM May spoke with German Chancellor Merkel. There was no clear result of the talks, but maybe May gained support for some kind of a tailor-made solution. EUR/GBP declined slightly towards the end of the session. Rightmove house prices were higher than expected 0.8% M/M, but the London boom market was said to be over. We expect more consolidation in the 0.8690/0.8930 trading range. The day-to-day momentum became less skeptical on sterling

EUR/USD topside test rejected, for now