{kind=link}

Here are the latest developments in global markets:

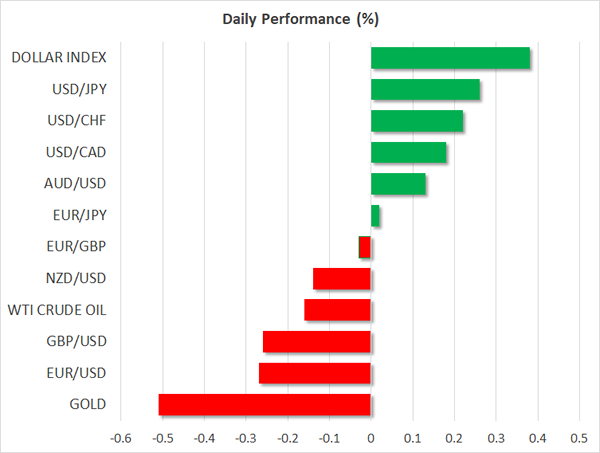

FOREX: The dollar index traded 0.4% higher on Tuesday, drawing some support from an uptick in the yields of longer-dated US Treasuries. The index rebounded on Friday after touching a fresh 3-year low, and has continued recovering since.

STOCKS: US markets remained closed yesterday in celebration of the President’s Day holiday. Earlier on Friday, the S&P 500 and the Dow Jones closed marginally higher, though the Nasdaq Composite fell 0.2%. Moreover, futures tracking the S&P, Dow, and Nasdaq 100 are currently in negative territory, suggesting that the turbulence in equity markets may still have some room to run. In Asia, most major indices were flashing red today. Japan’s Nikkei 225 and Topix closed 1.0% and 0.7% lower respectively, while in Hong Kong, the Hang Seng fell by 0.8% on its first day back from holidays. Chinese markets remain closed for the Lunar New Year festivities. In Europe, futures tracking the Euro STOXX 50 were little changed.

COMMODITIES: Oil prices were mixed today, as the two major benchmarks moved in different directions. While WTI gained almost 0.2%, Brent crude declined by roughly 0.4%. Although oil prices have recouped some of their losses in recent days, the outlook surrounding the oil market continues to be clouded by the continued surge in US production. On Friday, the US Baker Hughes oil rig count showed a further increase in the number of active oil rigs, providing a fresh signal that US output likely increased further from its record-high 10.27 million bpd. In precious metals, gold was 0.5% lower on Tuesday, as the recovery in the greenback made the dollar-denominated metal appear less attractive.

Major movers: De Guindos nominated for ECB Vice President; SPD votes on coalition government

Monday was relatively quiet in terms of price action, with most FX pairs seeing range-bound trading as US and Canadian traders were away on holiday. There were a few interesting news developments though, most notably the nomination of Spanish Economy Minister Luis de Guindos to succeed Vitor Constancio as the ECB’s Vice President.

While De Guindos is not anticipated to rock the boat in terms of policy, the nomination of a Southern European as ECB vice-chief has stoked speculation that the next ECB President after Draghi may be from central Europe, perhaps German or French. This is significant, since nations like Germany and France have traditionally favored a tighter policy stance. Thus, if somebody like Bundesbank chief Jens Weidmann is nominated to replace Draghi, then the ECB could well sail in a more hawkish direction over time.

Staying in Europe, today in Germany, the members of the SPD will begin voting in a postal ballot on whether their party should proceed with forming a coalition government with Merkel’s CDU. The results are not expected until March 4, the day that Italy will also head to the polls to elect its next government.

Sterling/dollar is nearly 0.3% lower today, extending the hefty losses it posted on Monday and Friday. A cocktail of soft UK retail sales, a recovering dollar, and some comments from the EU’s top Brexit negotiator are the culprits behind the pair’s recent underperformance. On Friday, EU chief negotiator Michel Barnier said the UK’s red lines close the door to a Swiss or Norwegian model for Brexit, enhancing the narrative that these talks are still far from bearing fruit.

Elsewhere, the minutes from the Reserve Bank of Australia’s (RBA) latest policy gathering released overnight packed few surprises. Policymakers reiterated the key risks they see as clouding the economy’s outlook, such as the high levels of household debt and the subdued growth in wages. Aussie/dollar stumbled after the release, but recouped its losses to trade even higher in the following hours.

In trade news, the US Commerce Department recommended on Friday that the US imposes heavy tariffs on steel and aluminum imports. If enacted, such measures would probably escalate further the trade tensions between the US and China, not least because China has already warned it may retaliate to such an action.

Day ahead: Business & consumer confidence surveys and bi-weekly milk auction on the horizon

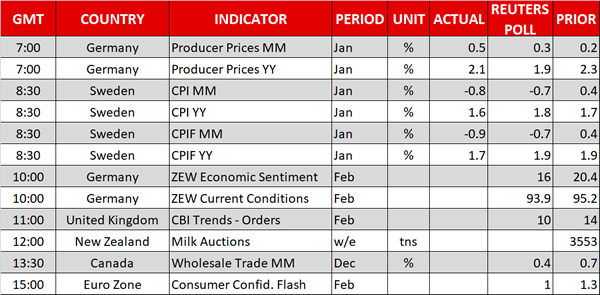

The ZEW institute’s surveys gauging economic sentiment and current conditions in Germany, eurozone’s largest economy, will be made public at 1000 GMT. Both releases are expected to reflect a decline in February after January’s surge. A related survey from the European Commission’s Directorate General for Economic and Financial Affairs covering the whole of the euro area – February’s flash consumer confidence – is scheduled for release at 1500 GMT. It also projects a dip in consumer confidence after rising to its highest since 2000 in January.

Out of the UK, the Confederation of British Industry’s monthly order book balance, gauging factory activity, will be released at 1100 GMT. The measure is anticipated to further ease in February; in December it touched a near 30-year high as British manufacturers were supported by strong export demand.

The bi-weekly milk auction is due around 1400 GMT; the release is tentative, lacking a specific time of release. Dairy products are New Zealand’s largest goods export earner, thus kiwi pairs will be eyed as the reading goes public.

Canadian wholesale trade data for the month of December are scheduled for release at 1330 GMT.

Swedish central bank Governor Stefan Ingves will be talking about the economy and monetary policy at 1730 GMT.

As the earnings season continues, Walmart and Home Depot will be among companies releasing results in the US.

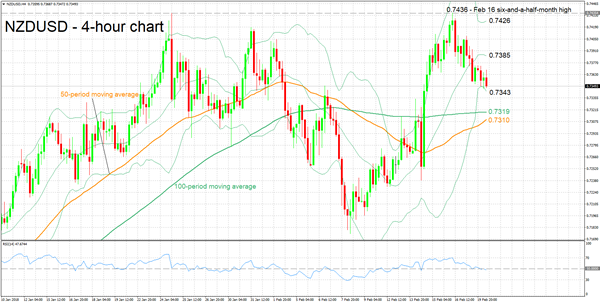

Technical Analysis: NZDUSD hits 6-day low; looks bearish to neutral in short-term

NZDUSD recorded a six-day low of 0.7347 earlier on Tuesday. This compares to last week’s (February 16) six-and-a-half-month high of 0.7436.

The RSI has been declining following last week’s high, though it seems to be consolidating around the 50-neutral perceived level at the moment, painting a bearish to neutral picture in the short-term.

Stronger-than-expected dairy prices out of today’s auction could lend some support to the pair, with price advancing potentially meeting resistance around 0.7385, this being the middle Bollinger line, a 20-period moving average line.

A weaker than anticipated release on the other hand, could see the pair extending its declines. The lower Bollinger band at 0.7343 could be providing support at the moment, with a downside violation shifting the focus to the area around the 100-period MA at 0.7319.