Here are the latest developments in global markets:

FOREX: The dollar was recording losses versus a basket of currencies, falling to its lowest in two weeks, as fears over as potential trade war were rekindled following the resignation of US President Trump’s top economic advisor, a free trade proponent.

STOCKS: US markets managed to close higher yesterday, with the Nasdaq Composite gaining 0.6%, the S&P 500 climbing 0.3%, and the Dow Jones rising, though only marginally so. However, a few hours after US markets closed, news hit the wires that Trump’s chief economic advisor Gary Cohn would resign, reviving concerns that a trade war may be looming and sending US equity futures sharply into negative territory. As expected, risk aversion rolled into Asia, with major benchmarks being a sea of red. Japan’s Nikkei 225 and Topix fell by 0.8% and 0.7% respectively, while in Hong Kong, the Hang Seng was down by 1.0%. Europe seems ready to follow suit, with futures tracking all the major indices currently flashing red, pointing to a lower open.

COMMODITIES: Oil prices fell sharply, with WTI and Brent crude trading 0.8% and 0.9% lower respectively, as investors’ risk aversion and the API inventory data weighed on the precious liquid. The private API figures showed a larger-than-expected build in crude stockpiles, which likely generated speculation that the official EIA inventory data later today (1530 GMT) are likely to show similar results. In precious metals, gold prices fell 0.1% on Wednesday, with the yellow metal being unable to sustain the gains it posted on the news that Gary Cohn resigned. It is currently trading near the $1332/ounce mark, and in case trade concerns intensify further, then the safe-haven could extend its gains and head for a test of the $1340 resistance zone.

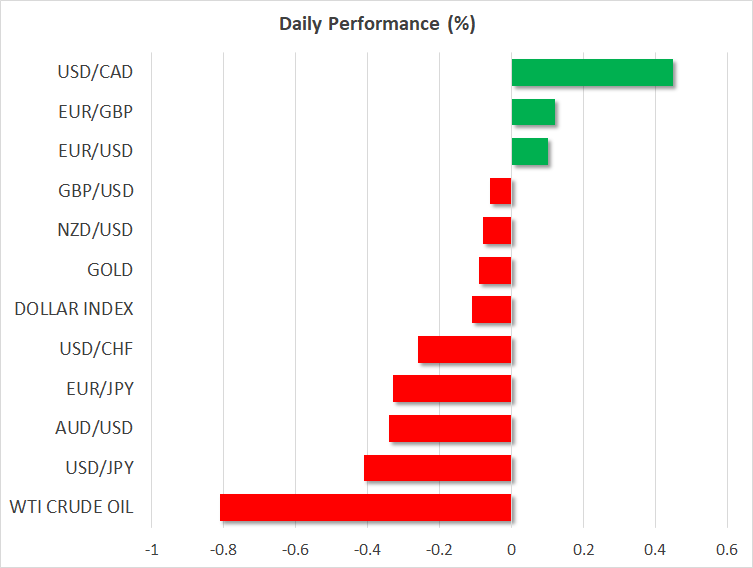

Major movers: Dollar records losses following Cohn’s resignation; loonie relatively close to 8-month low ahead of BoC rate decision

The dollar index was 0.15% down, trading close to 89.41, its lowest since February 20 recorded earlier on Wednesday. The decline in the greenback was fueled by the resignation of Gary Cohn; he served as President Trump’s top economic advisor.

Cohn was reportedly taking initiatives to avert the imposition of tariffs announced by Trump last week and his resignation is leading markets to reassess the risk of a trade war occurring, apparently revising the probability of such an outcome upwards. The fall in Asian equity markets on Wednesday is indicative of risk sentiment falling.

Some argue that policymakers favoring protectionism within the White House also favor a weaker dollar, something which would enhance US exports and act to the detriment of imports.

The safe-haven perceived yen was benefitting from the uncertainty, with dollar/yen falling by 0.4% and touching 105.43 at its lowest, this being not far above last week’s 16-month low of 105.23. The dollar was losing ground versus the Swiss franc as well, which also tends to gain at times of uncertainty.

Euro/dollar was up, though not by much, hitting its highest since February 19 of 1.2434 earlier in the day. On a weekly basis, the pair is up by 0.8%, recovering from the losses induced by the “inconclusive” Italian elections, with the focus turning to the ECB meeting which concludes tomorrow. Pound/dollar was little changed, being roughly 20 pips below the 1.39 level.

Aussie/dollar was 0.35% down, trading around the 0.78 handle. The pair gave back part of Tuesday’s gains that saw it rise to the one-week high of 0.7842; those came on the back of the North Korea denuclearization story that boosted risk appetite. Concerns around trade are seen as the catalyst behind today’s fall in the pair. Australia is a major commodity exporter and potentially stands to lose significantly should a trade war occur. Weaker-than-anticipated GDP figures out of Australia earlier today could have also contributed to negative sentiment for the pair. Kiwi/dollar was not much changed, trading not far below the 0.73 handle.

The Canadian dollar was recording losses versus its US counterpart as the latest developments are seen as increasing the risk that the US will leave NAFTA. Dollar/loonie was up by 0.45% at 1.2931 ahead of an interest rate decision by the Bank of Canada later in the day. This compares to 1.3000, the eight-month high hit on Monday. The Mexican peso was also losing ground versus the greenback; Mexico is one of the three countries participating in NAFTA.

Day ahead: Bank of Canada decision, US data and trade concerns in focus

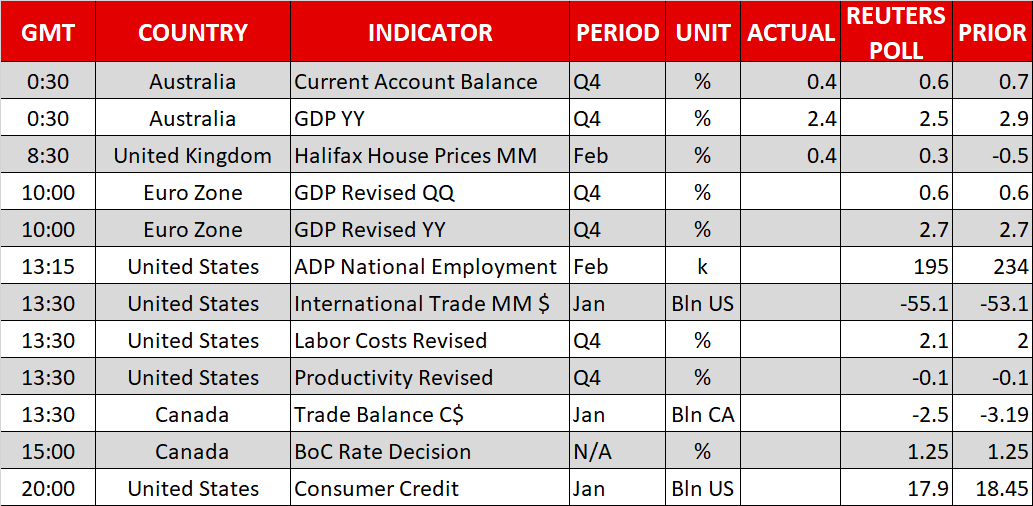

The main event in the FX market today will probably be the Bank of Canada (BoC) rate decision at 1500 GMT. Attention will also fall on the release of the US ADP employment report, as well as any potential updates on the trade front, in light of Gary Cohn’s resignation and the resurging probability of a tit-for-tat trade war.

The BoC is widely anticipated to remain on hold today, having raised interest rates at its latest meeting in January. Investors will scrutinize the accompanying statement looking for clues as to whether the recent softness in economic data and the increasing risk of trade tariffs from the US will delay the Bank’s future hiking plans. If indeed the BoC signals that it will be even more cautious in raising interest rates given these trade uncertainties, then the loonie could extend its recent losses. That said, caution is always warranted: the market may already be anticipating a concerned tone by the BoC, implying that anything other than a dovish statement could prove cause for a rebound in the CAD.

Turning to economic data, the eurozone will release the final estimate of economic growth for Q4 2017 at 1000 GMT, though the final figure is usually not a major market mover.

In the US, the ADP employment report for February is due out at 1315 GMT and expectations are for the private sector to have added 195k jobs in the month. If confirmed, such a print could enhance speculation that the NFP number on Friday may also meet its forecast of 200k and thereby, help the dollar to recover some of its latest losses. The US trade balance for January is also set for release at 1330 GMT, alongside the final estimate of labor costs for Q4 2017.

In energy markets, oil traders will keep their eyes on the weekly EIA crude inventory data at 1530 GMT. Stockpiles are forecast to have risen again, though by less compared to the previous week.

Equity markets will likely continue to be driven by speculation regarding the likelihood of a trade war actually materializing. Even though US Treasury Secretary Steven Mnuchin said yesterday that the US is “not looking to get into trade wars”, the resignation of Gary Cohn and President Trump’s unyielding stance on the imposition of tariffs are keeping that risk very much alive. Markets are still uncertain as to whether these are simply unorthodox negotiating tactics in complex trade talks, or whether the President is indeed set to toughen up on trade, perhaps to appeal to his voting base ahead of the midterm US elections. Until there is more clarity on the subject, price action in equities may remain choppy, and especially sensitive to headlines.

As for today’s speakers, we will hear from Atlanta Fed President Raphael Bostic (voter), as well as New York Fed President William Dudley (voter), at 1300 GMT and 1320 GMT respectively.

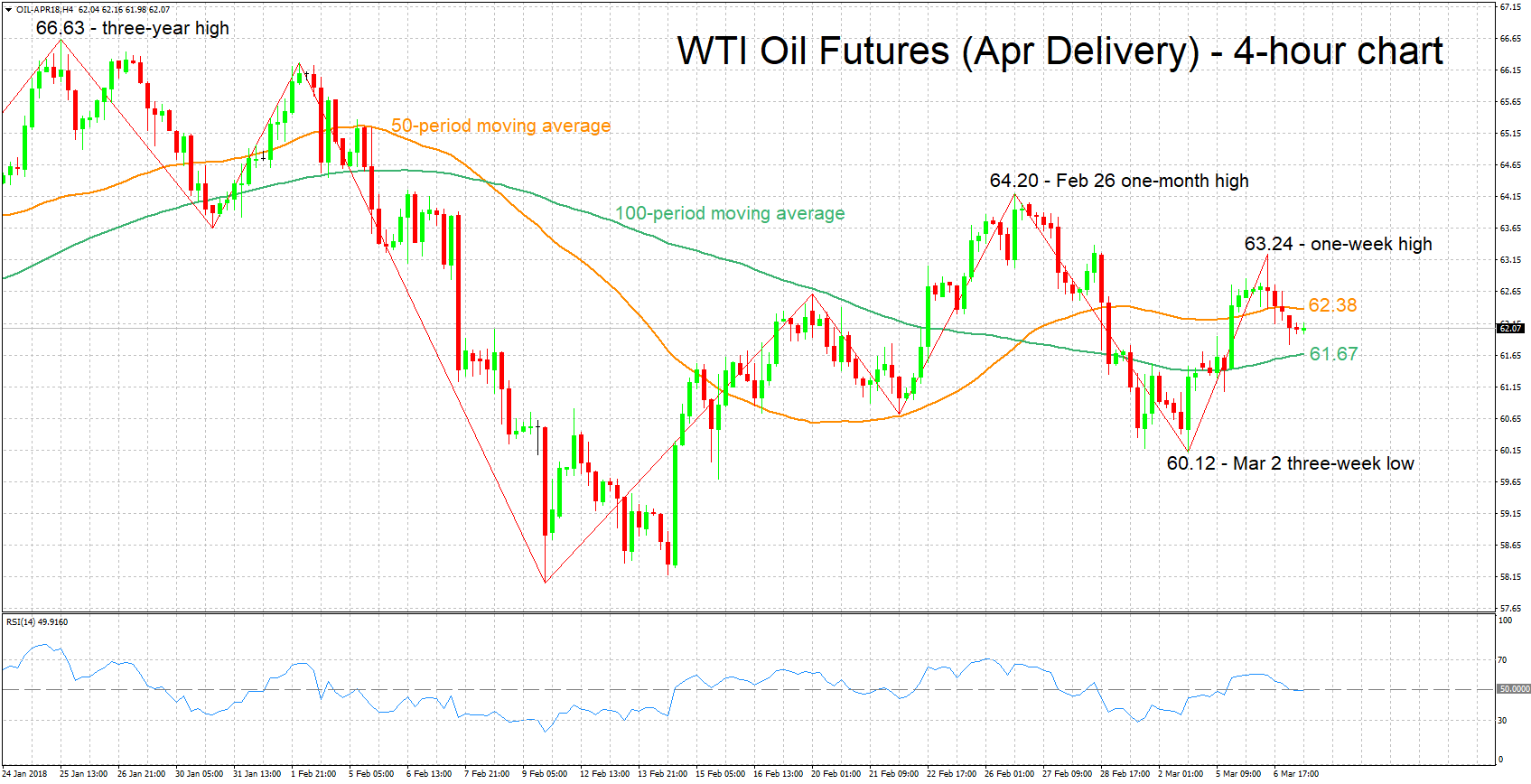

Technical Analysis: WTI oil futures looking neutral in the short-term

WTI oil futures for April delivery retreated a bit after recording a one-week high of 63.24 during Tuesday’s trading. The RSI is at the 50 neutral-perceived level and is currently moving sideways, hinting to the absence of short-term momentum in either direction.

If the Energy Information Administration’s weekly report shows a smaller-than-projected increase – or of course a decrease – in US crude oil inventories, prices could advance. In this case, resistance could come around the 50-period moving average at 62.38. Further above, the focus would turn to yesterday’s high of 63.24.

On the other hand, should crude inventories rise by more than anticipated, then prices might post losses. In this scenario, immediate support could come around the 100-period MA at 61.67, with attention falling to the three-week low of 60.12 from March 2 in case of steeper declines.

{kind=link}