Here are the latest developments in global markets:

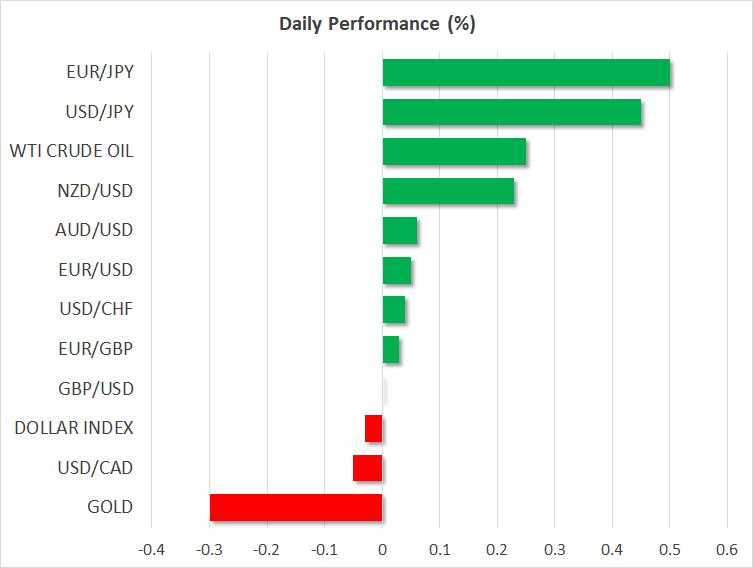

FOREX: The yen was recording significant losses versus other major currencies on the back of elevated risk sentiment spurred by a possible meeting between US President Donald Trump and North Korea’s Kim Jong Un.

STOCKS: US markets closed higher on Thursday, as the imposition of “watered down” US tariffs amplified expectations that the tensions will not escalate into a trade war, but may instead remain relatively contained. The S&P 500 led the charge, climbing 0.5%, while the Dow Jones and the Nasdaq Composite followed in its tracks, each gaining 0.4%. Futures tracking the S&P, Dow, and Nasdaq 100 are currently in negative territory, but only marginally so. Asian markets were a sea of green, as risk appetite was boosted by news that US President Trump agreed to meet with North Korea’s leader, helping to curb geopolitical risks. In Japan, the Nikkei 225 and the Topix rose by 0.5% and 0.3% respectively, while in Hong Kong, the Hang Seng was nearly 1.0% higher. In Europe though, futures tracking the major indices were all flashing red, with the exception of Spain’s IBEX 35.

COMMODITIES: Oil prices were a little higher on Friday, with WTI crude and Brent gaining 0.2% and 0.3% respectively, both benchmarks recovering some of the losses they posted on The fall in prices is being attributed to the gains the dollar posted yesterday, though concerns surrounding the surge in US production may have contributed to the down-move as well. Today, investors will look to the Baker Hughes oil rig count (1800 GMT) for a fresh indication on whether US supply continues to soar. In precious metals, gold was 0.2% lower on Friday, posting losses for the third consecutive day. The stronger dollar and the deescalating tensions in the Korean peninsula are likely the “culprits” behind the yellow metal’s pullback.

Major movers: Yen records losses on improving risk sentiment

The dollar was notably higher versus the safe-haven yen, touching an eight-day high of 106.94 at its peak. US President Donald Trump showing willingness to meet with North Korea’s Kim Jong Un by May was the catalyst behind the positioning by market participants, with the move seen as further easing tensions between the two parties and giving traction to the denuclearization talk from earlier in the week. At 0733 GMT, dollar/yen traded 25 pips below the aforementioned high and at a distance to last week’s 16-month low of 105.23.

Overall risk appetite got a boost on the news, with Asian equities rising across the board.

The Trump administration proceeded with the imposition of tariffs on steel and aluminum, exempting though Canada and Mexico though, and leaving the door open for other countries to be exempted. The administration’s stance was viewed by markets as more moderate than previously and was seen as reducing the odds for a global trade war.

Abating geopolitical worries seem to be driving sentiment for now, but trade concerns could well make a comeback.

Earlier on Friday, the Bank of Japan completed its meeting on monetary policy, keeping policy unchanged. The Japanese currency showed limited reaction to the decision. In the press conference that followed, BoJ Governor Haruhiko Kuroda recognized that the trade policy of the US poses risks to the global economy.

Euro/dollar was roughly flat at 1.2314 after losing 0.8% on Thursday in the aftermath of the ECB’s respective meeting on monetary policy. The Bank dropped its pledge to increase its asset purchases if needed, something which initially supported the euro. However, ECB chief Mario Draghi later played down the significance of the decision, while adding that inflation in the euro area remains muted. The euro was another currency posting considerably gains versus the yen during Friday’s trading. Euro/yen was 0.5% up at 131.41, making up for a significant portion of yesterday’s losses.

Elsewhere, pound/dollar was practically unchanged at 1.3813.

In emerging markets, the yuan didn’t react much versus the greenback to stronger-than-anticipated inflation figures that saw annual CPI rise to its highest in four years (PPI slightly surprised to the downside). It is interesting that markets shrugged off a warning by China that it will take “strong” measures against US tariffs. Dollar/yuan was 0.1% down at 6.3350 after previously recording a one-week high of 6.3526.

Day ahead: US payrolls & wage data and Canadian jobs figures on the agenda; potential tariff retaliations eyed

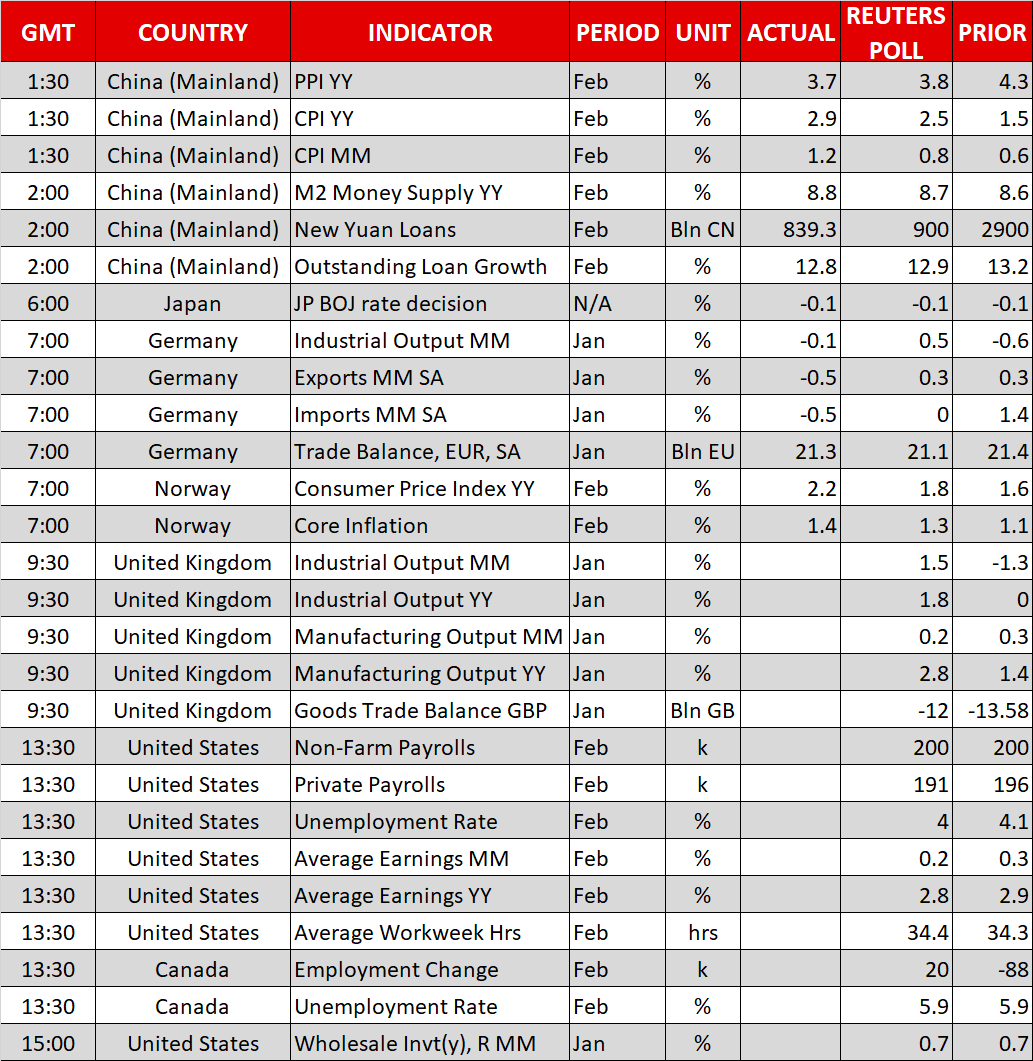

The main event today will be the US employment report for February at 1330 GMT. Nonfarm payrolls are anticipated to have risen by 200k, exactly as much as in the previous month, the unemployment rate is projected to have ticked down to 4.0%, while average hourly earnings are expected to have slowed to 2.8% in yearly terms, from 2.9% previously. Given the recent market narrative that US inflation may be set to pick up speed soon, investors may pay special attention to the earnings figures, as wage growth is broadly considered a precursor to inflation.

In case these data come out stronger than anticipated – particularly on the wages front – markets are likely to begin pricing in a higher probability that the Fed may deliver four quarter percentage point rate hikes this year, from the three that are already priced in. The dollar could come under renewed buying pressure in this scenario, as the yields on US bonds will likely surge. A disappointment, on the other hand, would likely dampen inflation concerns, and possibly generate some skepticism as to how many hikes the Fed will deliver this year, thereby weighing on the greenback.

Canada will also release its own employment data for February at 1330 GMT. The unemployment rate is forecast to have held steady at 5.9%, while the net change in employment is anticipated to have rebounded, following a sharp decline before. Such prints would likely be encouraging news for the Bank of Canada – which maintained a fairly cautious bias on Wednesday in the face of trade uncertainties – and could help the loonie to recover some of its recent losses.

In the UK, industrial output prints for January are due out at 0930 GMT and expectations are for the figure to have risen by 1.5% in monthly terms, following a 1.3% fall last month.

In equity markets, the “trade war” theme will probably continue to dominate price action. Following the official imposition of US tariffs yesterday, it will be interesting to see how major economies like the EU and China will respond, as both have already noted they will retaliate in kind. The magnitude and scope of these responses could well serve as a gauge of whether trade tensions are likely to escalate further, or whether they may subside somewhat.

In energy markets, investors will look to the release of the Baker Hughes oil rig count at 1800 GMT, for a fresh indication on whether US oil production continues to soar. Despite the latest EIA data showing that US output reached a fresh record high last week, the rig count has barely risen over the past couple of weeks, suggesting that the supply increase is slowing down. If that pattern continues today, then some of the downward pressure on oil prices could ease as investors might speculate that US production is close to peaking.

In terms of policymaker appearances, there are four on the agenda. In Europe, ECB Executive Board members Benoit Coeure and Sabine Lautenschlager will deliver remarks at 0830 and 0845 GMT respectively. A few hours later across the Atlantic, the Presidents of the Chicago Fed and the Boston Fed, Charles Evans and Eric Rosengren, will be speaking at 1340 and 1545 GMT respectively. Neither of them holds voting rights within the FOMC in 2018.

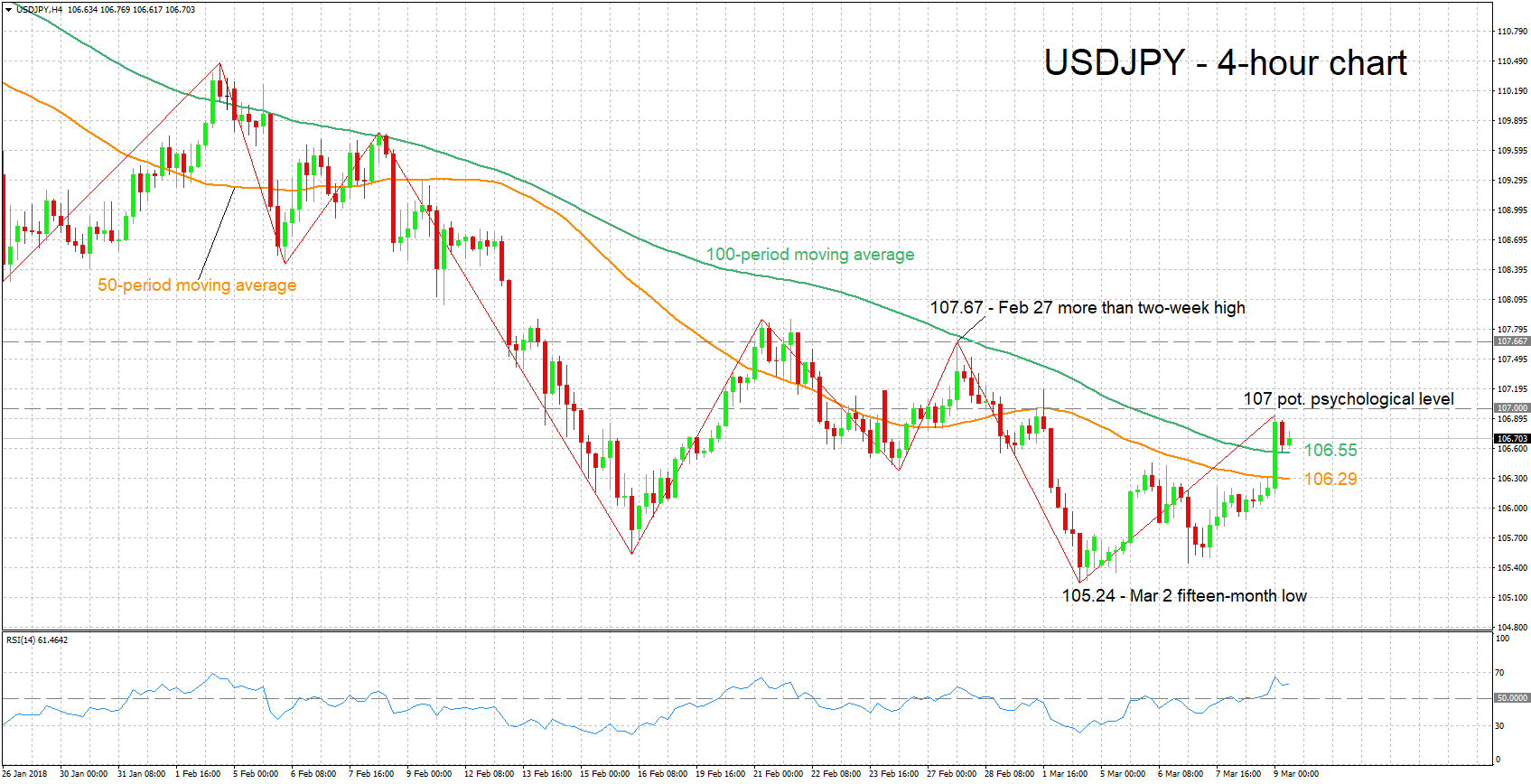

Technical Analysis: USDJPY records 8-day high; NFP report could fuel or bring to a halt the bullish sentiment

USDJPY recorded an eight-day high of 106.94 earlier on Friday. The RSI indicator has crossed above the 50 neutral-perceived level and continues rising, projecting a bullish picture in the near-term. The nonfarm payrolls report due later in the day has the capacity to dictate the pair’s short-term direction.

A stronger-than-expected report, especially on the front of wage growth, is expected to boost the pair. The range around the 107 handle which was congested in the past (with 107 potentially holding psychological significance as well) could act as a barrier to the upside in this case. A break above this area would turn the attention to the more-than-two-week high of 107.67 for additional resistance.

On the other hand, disappointing figures are anticipated to lead to losses for the pair. In this scenario, support might come around the current levels of the 100- and 50-period moving averages at 106.55 and 106.29 respectively.

{kind=link}