Here are the latest developments in global markets:

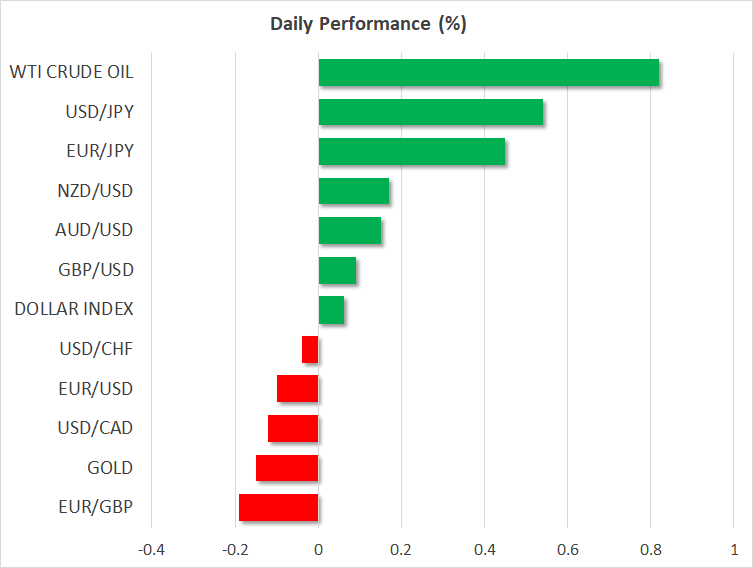

FOREX: Trump’s decision to exempt the US’ close trade allies Canada and Mexico from hefty import tariffs on steel and aluminum yesterday, while leaving the door open to other countries, and the announcement that he has accepted the invitation to meet the North Korean leader, Kim Yong Un, continued to support the dollar during the European trading session. The dollar index retained its gains from yesterday, last trading at 90.24 (+0.07%), whilst dollar/yen was enjoying gains at 106.77 (+0.54%) ahead of the eagerly awaited nonfarm payrolls report as risk appetite returned to the markets. The BoJ’s decision to maintain its ultra-easy monetary policy until inflation reaches 2.0% didn’t bode well for the yen either. Euro/dollar was stuck at today’s lows, last seen at 1.2298 (-0.08%) as the response out of the EU regarding the US’ import tariff implementation ranged from threats of retaliation to hopes of exemption. Pound/dollar was lacking direction at 1.3817 (+0.04%) after hitting a low of 1.2779 late yesterday since neither Britain was exempted from the US’ protectionist measures. British industrial figures were not good news either today, with all relevant indicators coming in worse than expected. Euro/pound extended losses to 0.8898 (-0.19%). The antipodean currencies were in the green despite China’s warnings to impose strong measures to counter US tariffs, with aussie/dollar and kiwi/dollar changing hands at 0.7802 (+0.15%) and 0.7272 (+0.17%) respectively, however, versus the yen both currencies posted larger gains. Dollar/loonie was fluctuating near today’s lows, last seen at 1.2881 (-0.14%).

STOCKS: European stock indices opened lower on Friday as EU industries dependent on aluminum and steel would potentially feel the pain arising from US import tariffs if the bloc fails to secure an exemption. Still, optimism that the region could eventually be granted an exemption by the US restricted steeper declines. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.05% and 0.12% respectively, led by losses in industrials and financials. The German DAX 30 tumbled by 0.45%, with industrial output data failed to improve sentiment. Particularly, German industrial production decreased by 0.1% in January, less than in December but missed expectations for an expansion of 0.5%. The Italian FTSE MIB dropped by 0.47%, the French CAC 40 retreated by 0.20%, while the British FTSE 100 edged down by 0.04%. US stock futures on major Wall Street indices were slightly weaker.

COMMODITIES: Oil prices were up on the day, underpinned by the progress in the Korean story which lifted Asian equities and overall sentiment. Yet, the market was on track to post losses for the second week. WTI crude rose to $60.62/barrel (+0.88%) and Brent climbed to $64.21/barrel (+1.0%). In precious metals, gold was trading weaker at $1319.76/ounce (-0.18%).

Day ahead: US nonfarm payrolls next to challenge dollar; Canadian labor data also in focus

Day ahead: US nonfarm payrolls next to challenge dollar; Canadian labor data also in focus

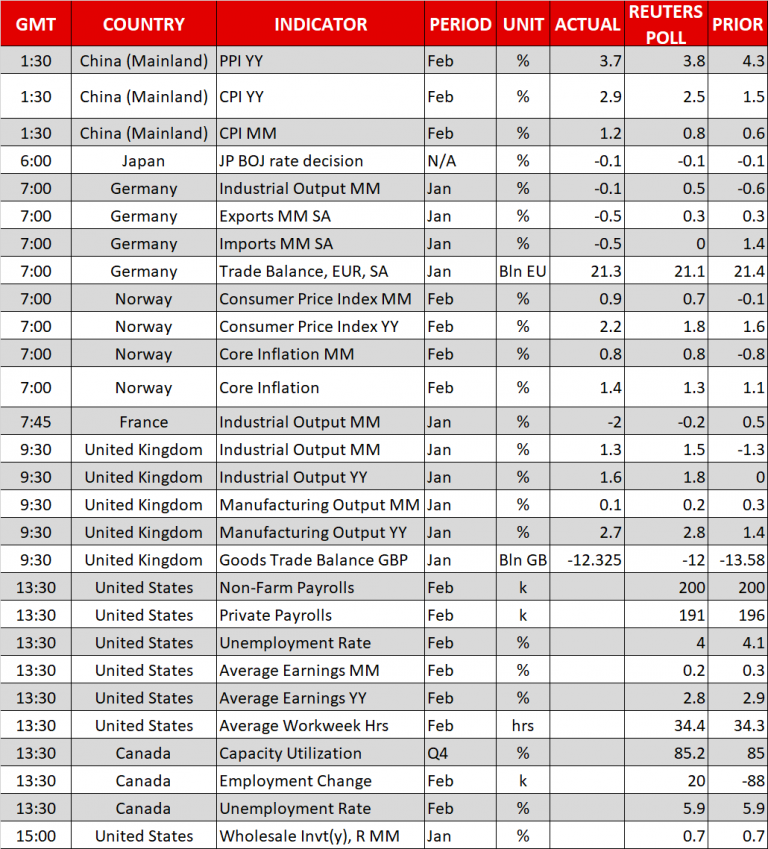

The US nonfarm payrolls report will come into center stage at 1330 GMT to move the dollar amid eased geopolitical risks in the Korean peninsula and easing worries over trade. Analysts predict the economy to have added 200,000 new job positions both in the public and private sectors in February (excluding the farm industry), the same as in January, while they expect the unemployment rate to inch down to 4.0%, hitting a fresh 17-year low. However, as in previous releases, the focus will turn to wage numbers as the Fed is eagerly waiting for higher wage growth to pick up and boost inflation before it continues with its pace of gradual rate increases. Growth in average hourly earnings, though, is expected to slow down to 2.8% y/y from 2.9% seen in the preceding month.

In case the data surprise to the upside, especially on the wage front, the chances that the Fed may deliver four rate hikes before the year’s end could increase, raising long positions on the dollar and consequently pushing the currency higher. On the other hand, if the NFP report disappoints, traders could doubt whether inflation has the strength to reach the Fed’s 2.0% target anytime soon, sending the dollar lower.

The US will also see the release of wholesale inventories and the weekly Baker Hughes oil rig count at 1500 GMT and 1800 GMT respectively.

In Canada, employment figures will also attract attention at 1330 GMT. After a deep fall of 88,000 in the number of employees in January, forecasts are now for a rise of 20,000. The unemployment rate though is expected to stay unchanged at 5.9%.

On the trade front, it would be interesting to see the US’ plans for countries such as China and the EU, given their recent warnings for a tit-for-tat retaliation against US protectionism.

Turning to today’s public appearances, the Presidents of the Chicago Fed and the Boston Fed, Charles Evans and Eric Rosengren, will be speaking at 1340 and 1545 GMT respectively. Neither of them holds voting rights within the FOMC in 2018.

{kind=link}