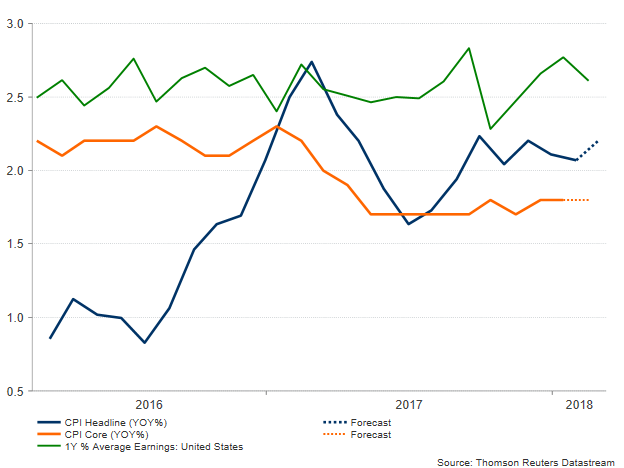

Flashing back a month earlier, an upward surprise in consumer prices caused a sharp but temporary reaction to the markets, with stocks sinking and government bond yields surging. While the consumer price index is not the Fed’s favorite inflation measure, and someone could expect the figures to be more informative rather than a market-driver, the numbers popped up in times when investors were already worrying that the economy would start generating more noticeable inflation. Indeed, in February, speculation that price growth could pick up speed increased after the Nonfarm Payrolls (NFP) wage component reached its highest pace since 2009 in yearly terms. Therefore, an upbeat CPI at that time was enough to add fuel to the fire and cause another market turbulence. This time, however, things are different, as Friday’s NFP report did not raise inflation fears but lifted risk appetite as wage growth eased. Therefore, it would be interesting to see whether CPI figures will gain further positive momentum as the forecasts suggest, reviving concerns over inflation ahead of the FOMC policy meeting next week.

According to analysts, the headline CPI due on Tuesday at 1230 GMT is expected to have risen by 2.2% year-on-year in February, above the 2.1% growth seen in January when price pressures were indicated in almost every single industry included in the index. In monthly terms, however, the gauge is expected to lose steam, falling from 0.5% to 0.2%. Excluding volatile items such as food and energy, the core measure is anticipated to remain steady at 1.8% y/y and slip from 0.3% to 0.2% m/m. Although, the index is not the one affecting monetary decisions – that would be the Personal Consumption Expenditure Index – is still a key indicator of inflation trends and any unexpected spike in the numbers on Tuesday could give an early indication of what the February PCE index could be, when it is released at the end of March. Still, the PCE would only be available days after the FOMC members conclude their policy meeting on March 21. Hence, the CPI numbers could affect discussions on inflation during the two-day gathering.

On the monetary front, markets are widely pricing a rate hike coming next week with a probability of 88.8% based on the CME FedWatch tool. They are also betting on two more rate rises by the end of this year, probably delivered in June and September, while the Fed chief Jerome Powell’s rosy outlook on the US economy, expressed recently in front of the US Congress, opened the door for a fourth rate hike this year before Friday’s slowdown in wages curbed somewhat those expectations. Other Fed members also had optimistic views on the US economic performance and the path of future interest rates following Powell’s testimony, with the Dallas Fed President, Robert Kaplan, saying last Tuesday that three rate increases is a “reasonable” base case as the economy is right around full employment which should add further pressures on inflation. Esther George, the Kansas Fed President and a reliable hawk argued a few days later that “given the economic momentum, the Fed should continue to raise interest rates and carefully calibrate its policy to lean against a potential buildup of inflationary pressure or financial market imbalances”. However, it is worth noting that these comments were made before Trump signed the implementation of import tariffs on steel and aluminium on several countries (except Canada and Mexico) last week, therefore policymakers might reconsider their growth prospects given that government’s levies on materials and a potential tit-for-tat retaliation from other countries could dent benefits arising from the corporate tax cuts. On the consumers’ front, higher import tariffs could translate into higher prices. While this is what policymakers want at the moment, they would not welcome the measures if these weigh on consumer spending.

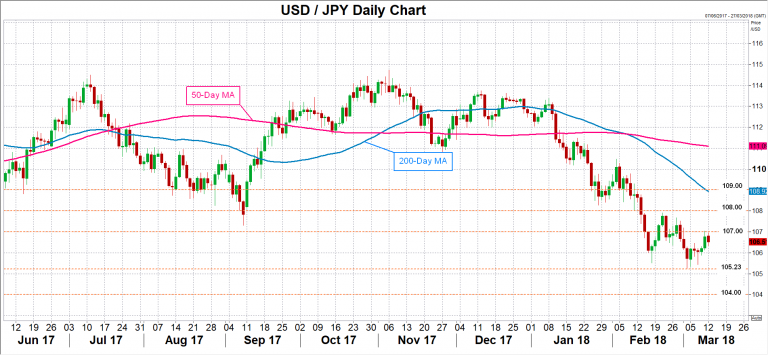

Turning to forex markets, in the wake of stronger than expected CPI readings which could raise inflation expectations, dollar/yen could revisit the 107 handle and even touch the previous high of 107.90 posted on February 21. If there is a significant deviation above the forecasts, the 108 and the 109 psychological levels could also come into view. In the alternative scenario, disappointing CPI prints could send the market down to the 106 key-mark, while in the worst case the pair is not unlikely to cross below the 16-month trough of 105.23, opening the way towards the 104 key-level.

{kind=link}