Here are the latest developments in global markets:

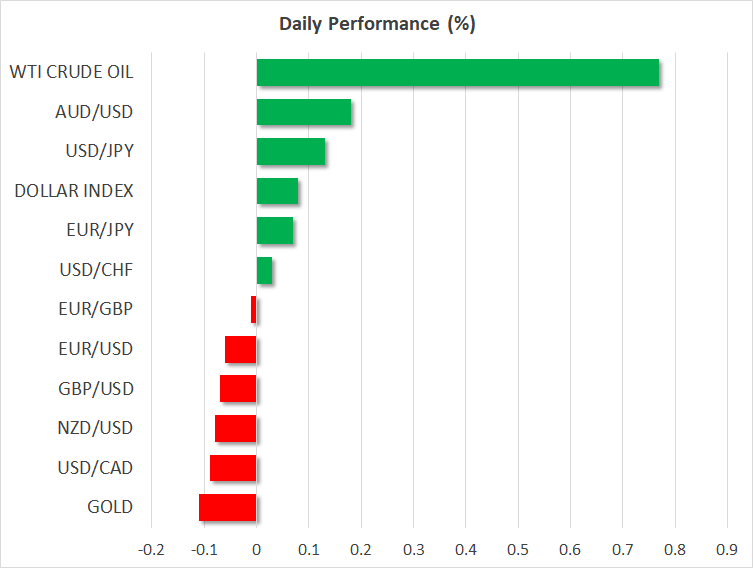

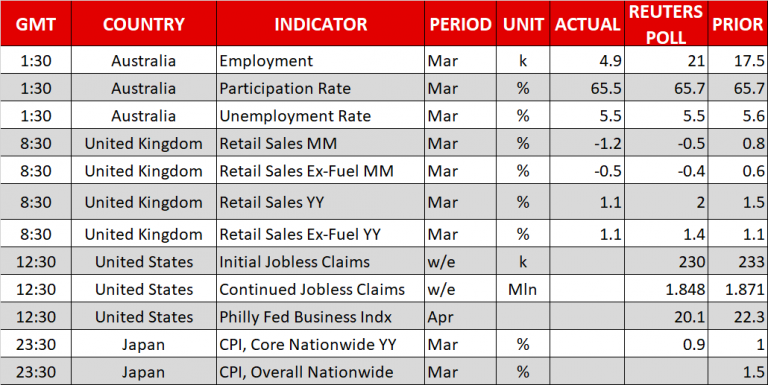

FOREX: Sterling tumbled to a five-day low against the greenback (-0.06%) on Thursday during the early European afternoon as UK retail sales recorded their biggest fall in a year. This follows a strong sell-off on Wednesday when the UK CPI dropped surprisingly to one-year lows, raising doubts on whether the Bank of England will proceed with further rate increases after next month’s widely anticipated rate hike. Dollar/yen was moving slightly higher by 0.13% on the day, last trading at 107.39. Euro/dollar edged down to 1.2367 losing 0.06%. Dollar/loonie was weaker at 1.2617 (-0.06%) following a strong rally towards one-week highs on Wednesday, when the BoC stood pat on interest rates but held a cautious stance on future monetary tightening. Antipodean currencies were mixed, with aussie/dollar being up by 0.15% at 0.7791 and kiwi/dollar being down by 0.08% at 0.7309. Aussie shrugged off today’s weaker-than-expected data on job growth from Australia. Turkish lira took a breather, a day after posting its biggest one-day advance in more than a year after President Tayyip Erdogan declared early elections on June 24. Dollar/lira pared some losses, gaining 0.80%.

STOCKS: European stocks were mixed at 0946 GMT. The blue-chip Euro STOXX 50 was down by 0.02%, the German DAX 30 fell by 0.01% and the British FTSE 100 rose by 0.21%. The Italian FTSE MIB ticked significantly higher by 0.62%. The Japanese Nikkei 225 closed higher, posting an almost two month high, while in Hong Kong the Hang Seng surged by 1.40%. Futures tracking the major US benchmarks are currently flashing red after a mixed session on Wednesday.

COMMODITIES: Oil prices recorded new highs due to a decline in US oil inventories and also after sources signaled that Saudi Arabia would be happy to see the price closer to $100 a barrel. WTI continued the bullish rally and rose by 0.79% to $68.99 per barrel, while Brent surged by 0.64% to $74.12 per barrel. Gold was trading marginally lower by 0.05% to $1,348.2 per ounce.

Day ahead: Initial jobless claims, Philly Fed Manufacturing Index & Japanese inflation next in focus

Data out of the US will dominate the economic calendar later in the day, while early on Friday, the focus will shift to Japanese inflation readings after the US President and the Japanese Prime Minister seemed to have found a common ground on the North Korea front at the end of their two-day meeting in Florida yesterday. However, regarding trade, they failed to unify their opinions as the US President highlighted that he wouldn’t rejoin the Trans-Pacific free-trade partnership (TPP) unless Japan offers a deal he “could not refuse”. In contrast, the Japanese Prime Minister reiterated that a bilateral trade agreement, which the US favors, is not Japan’s desirable option.

In the US, figures on initial jobless claims will be delivered along with the Philadelphia’s Fed Manufacturing index at 1230 GMT. Analysts expect the number of people applying for unemployment benefits for the first time to have increased by 230,000 in the week ending April 13 compared to 233,000 seen in the preceding week, while they expect business conditions in Philadelphia to deteriorate slightly in April. Particularly, they anticipate the Philly Fed manufacturing index to fall from 22.3 to 20.1. This would be the lowest level reached since August.

In Japan, the Statistics Bureau will hand out stats on consumer prices at 2330 GMT (0830 AM on Friday in Japan). Projections are for the nationwide core CPI, which excludes fresh food but includes energy items, to inch down by 0.1 percentage points to 0.9% y/y in March as the winter season comes to an end, remaining far below the BoJ’s price target of 2.0%. A strengthening yen and subdued wages seem to be behind the weakness in inflation that reinforces BoJ policymakers’ stance to hold interest rates at record lows and continue to suppress the yields on Japanese bonds.

In equity markets, earnings releases will continue to attract interest.

As for today’s public appearances, the French President, Emmanuel Macron, and the German Chancellor, Angela Merkel, will be meeting in Frankfurt to discuss on how to reform the Eurozone. It would be interesting to see whether Merkel, who extended her term for the fourth time will remain cautious on Macron’s proposals to turn Europe’s existing bailout fund into a European Monetary Fund given the pressures she faces by her party to refuse any plans that could harm German taxpayers. In the US, permanent FOMC voting members Lael Brainard and Randal Quarles will be talking at 1200 GMT and 1330 GMT respectively. Also of interest might be a news conference (1245 GMT) by IMF Managing Director Christine Lagarde and World Bank President Jim Yong Kim ahead of the Spring Meetings of the two organizations; among notable names attending the meetings is ECB President Mario Draghi.

{kind=link}