The economic calendar is packed with data releases from the United Kingdom this week, starting with the latest inflation report at 06:00 GMT on Wednesday. Sterling has taken a heavy beating this year, underperforming even the war-ravaged euro despite a flurry of rate increases from the Bank of England. Until there is some good news from Ukraine that boosts stock markets and hammers energy prices, it is difficult to call for a trend reversal.

Ransacked

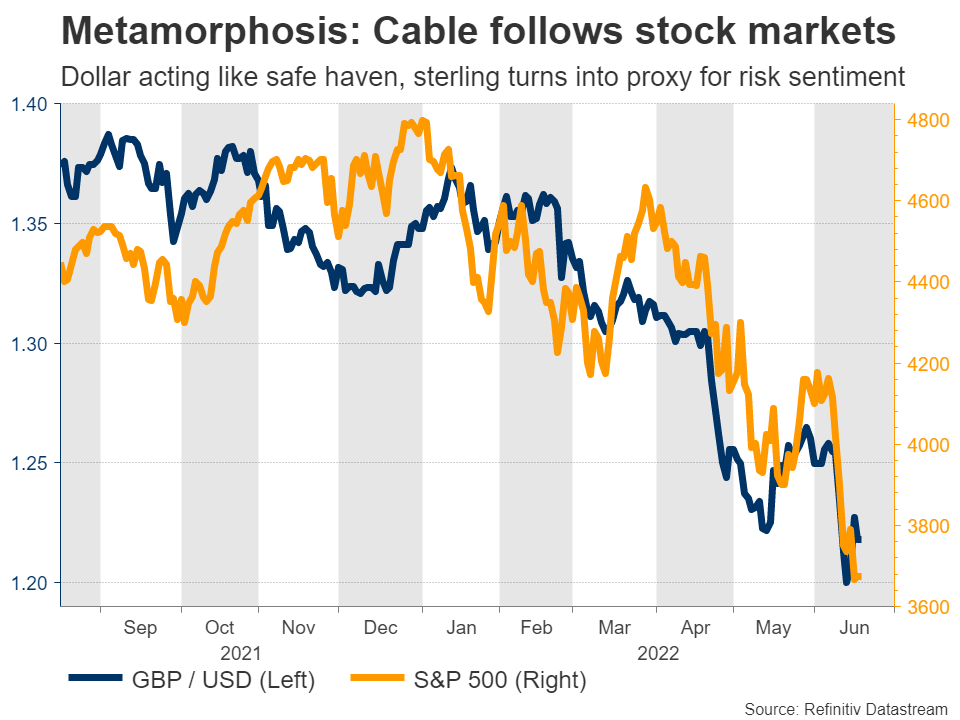

The British pound has been devastated. It has lost almost 10% of its value against the almighty US dollar and roughly 2% versus the euro this year alone, even though the Bank of England has raised interest rates at every single policy meeting.

Most of this lackluster performance boils down to the strong relationship between the pound and stock markets. The 60-day rolling correlation between Cable and the S&P 500 index currently stands at 0.93, so the two assets have moved in the same direction 93% of the time over the last couple of months.

Sterling is essentially trading like a proxy for global risk sentiment, which has been terrible lately. Surging energy prices and a sharp drop in business confidence that typically foreshadows an economic slowdown have also played a role in the pound’s dreadful performance.

Upcoming data

Turning to this week’s releases, the show will get started on Wednesday with the inflation stats for May. Forecasts suggest inflation reached 9.1% in yearly terms. On the bright side, this would be only a minor acceleration from the 9.0% recorded in April.

As for any surprises, the risks surrounding this inflation print seem tilted to the upside. The S&P Global PMI for the month pointed to another record increase in prices charged by services companies, so the official inflation forecast seems like a ‘lowball’ estimate.

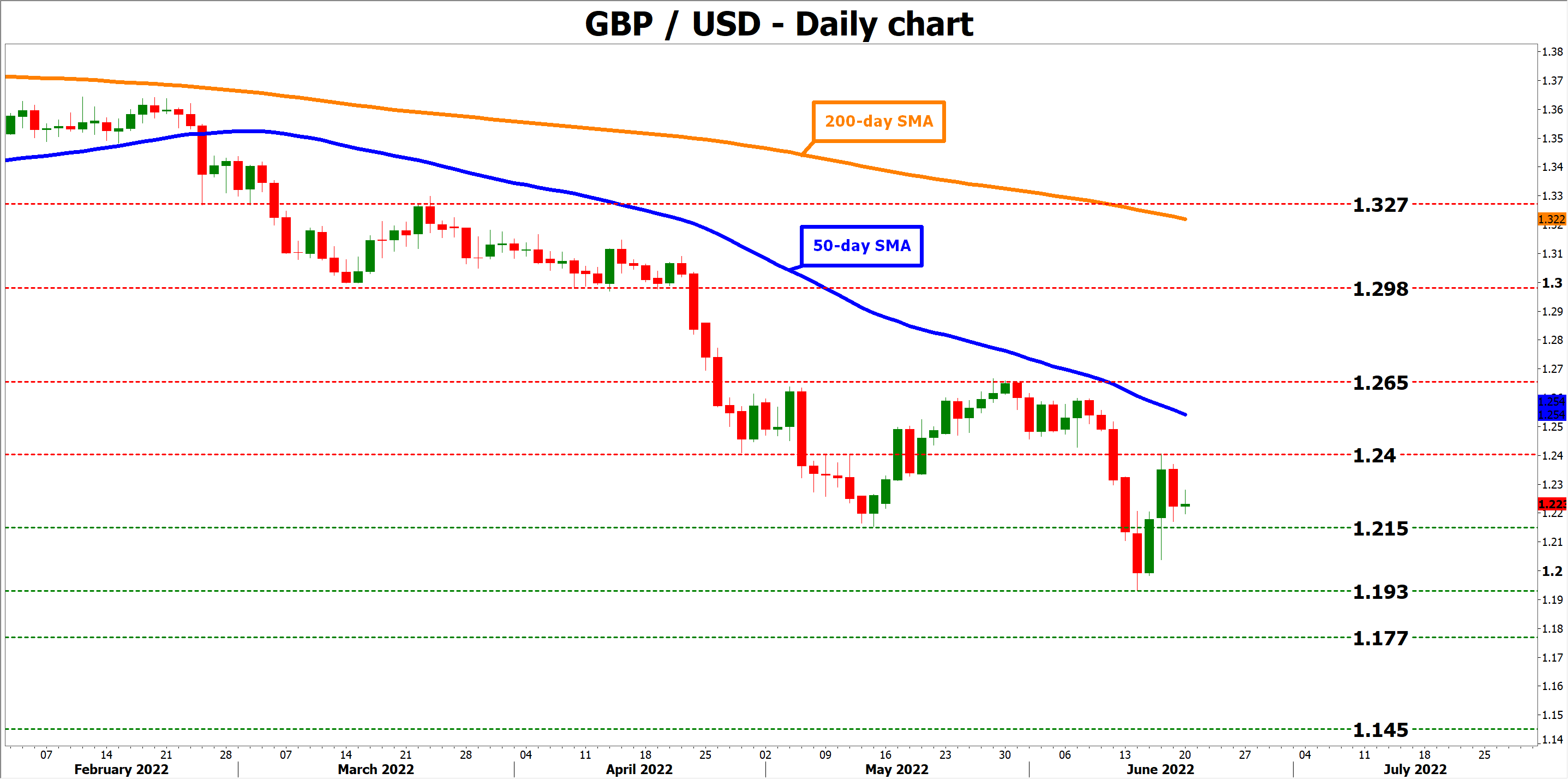

An upside inflation surprise could lend some support to sterling, on expectations that the BoE might accelerate the pace of rate increases. Taking a technical look at Cable, in this case the pair could edge higher for another test of the 1.2400 region.

Then on Thursday, the preliminary PMIs for June will hit the markets ahead of the latest retail sales on Friday. The PMIs are expected to have fallen further while retail sales are seen turning negative on a monthly basis. A soft dataset could cause the pound to give back any inflation-related gains, with downside moves in Cable likely to encounter initial support around 1.2150.

Big picture

All told, the outlook for the pound remains cautiously negative. It’s just difficult to call for any massive recovery while sentiment in stock markets remains so weak and energy prices so high.

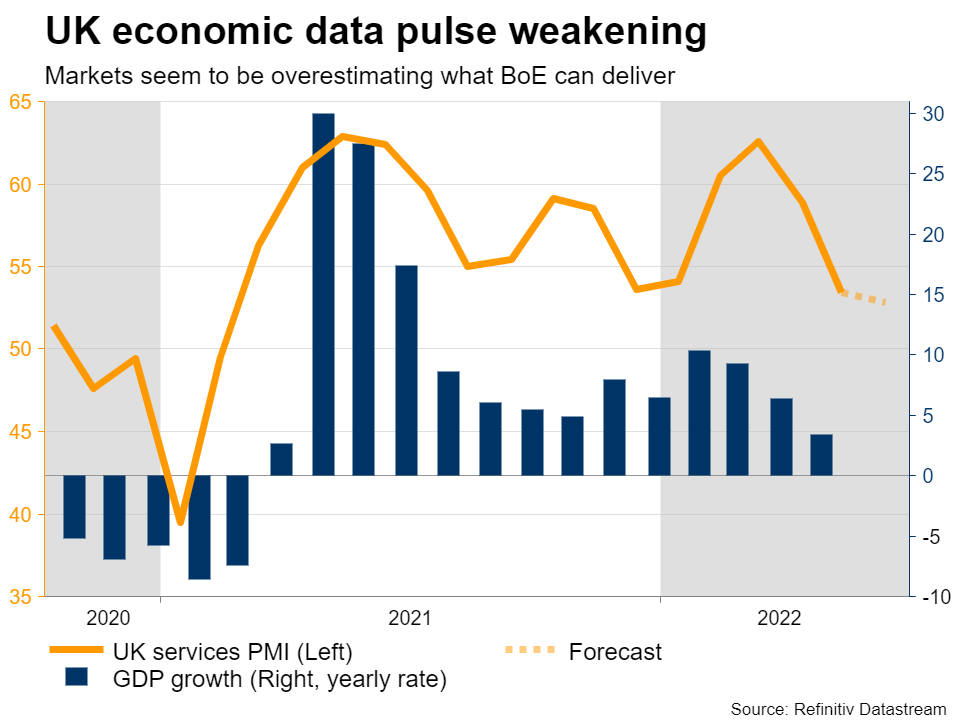

Traders also seem to be overestimating what the Bank of England can deliver. Market pricing currently suggests that the Bank Rate will close the year at 3%, from 1.25% currently. This implies the central bank will step up its game and raise interest rates by 50 basis points at three of its next four meetings.

The BoE has not raised rates by 50 bps so far in this cycle while the UK economy was firing on all cylinders – why would it so now that it is losing momentum and whispers of recession are growing louder? There is plenty of scope for disappointment embedded into current market pricing, which implies downside risks for sterling.

Political risk is back on the menu too, with reports that the UK is planning to abandon plans of the Brexit deal it negotiated with the European Union amid disagreement over the rules governing trade in Northern Ireland.

A trend reversal in the pound can be taken seriously only if it is accompanied by a major event that spreads joy in the markets and revives risk appetite – ideally with oil prices coming down as well. Some positive news around the Ukraine conflict could do the trick. Until then, the trend remains negative.

{kind=link}