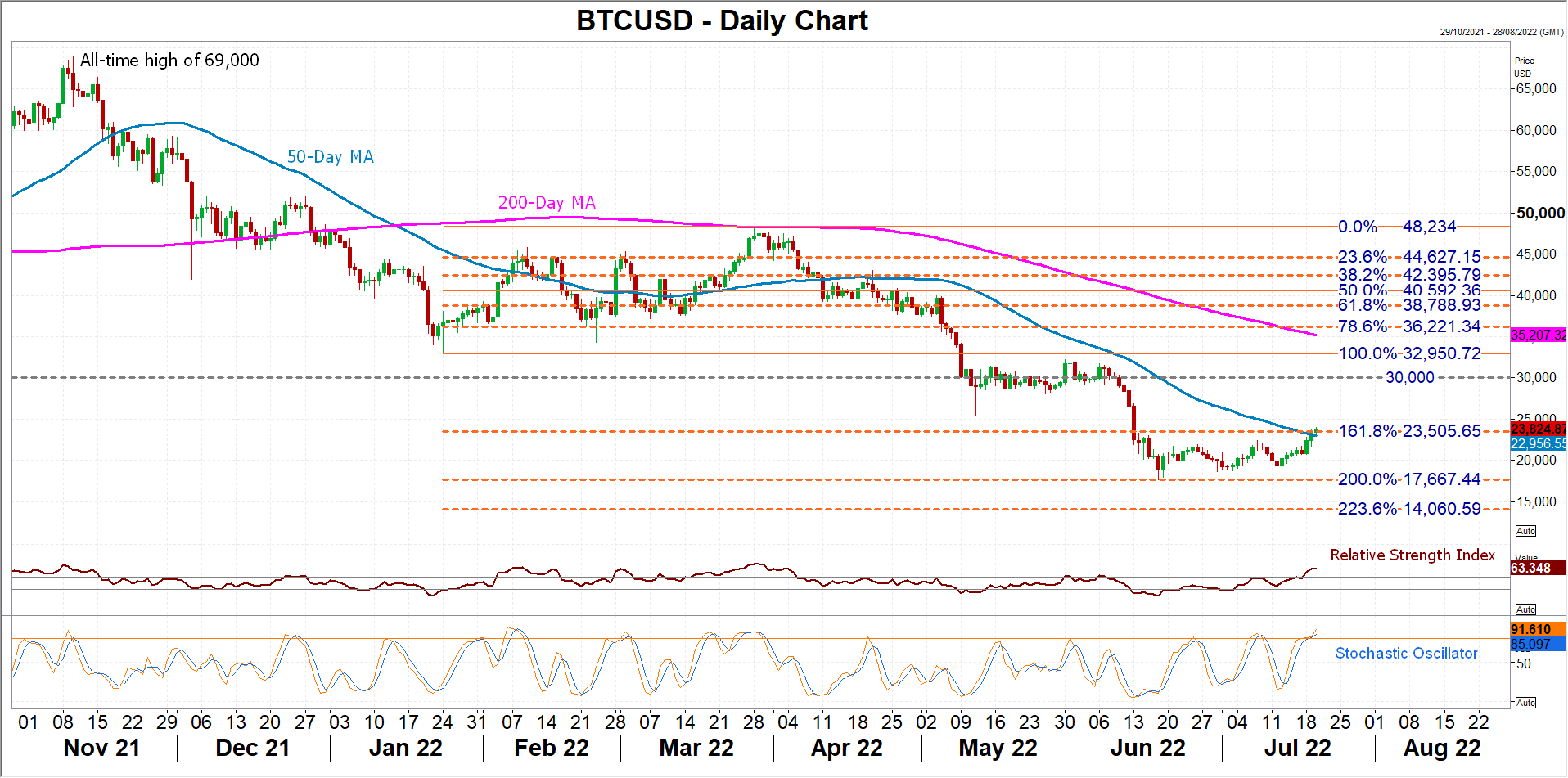

BTCUSD is struggling to maintain positive momentum on Wednesday as the week-long rally appears to have stumbled after getting caught between the 50-day moving average (MA) and the 161.8% Fibonacci extension of the January-March upleg at 23,505.65. The price earlier hit an intra-day peak of 23,940.99 – a one-month high. But the grind higher is slowing amid the heavy resistance region.

Still, the momentum indicators suggest there is scope for a further recovery, even though there is also the risk of a downside correction over the near-term horizon. The RSI continues to climb above 50 but has yet to reach the 70 overbought level, while the stochastics have already entered the overstretched territory. Both the %K and %D lines are pointing up and a bearish cross between the two is not imminent, suggesting that any negative correction would be several sessions away.

If the price is able to convincingly break above the 161.8% Fibonacci, the next major resistance point isn’t likely to be met until the 30,000 psychological level. Overcoming this hurdle too would clear the path for the 200-day MA just above 35,200.

However, if the upswing loses further steam and the price turns lower, there should be some support at the 200% Fibonacci, which corresponds with the 1½-year low of 17,592.78 set in June. If this trough is breached, the bears would probably next target the 223.6% Fibonacci of 14,060.59.

Overall, the short-term bias remains bullish for now even if there is some risk of a downside reversal. But in the bigger picture, BTCUSD would likely need to climb above 30,000 for the current bearish outlook to switch to a more neutral one.

{kind=link}