{kind=link}

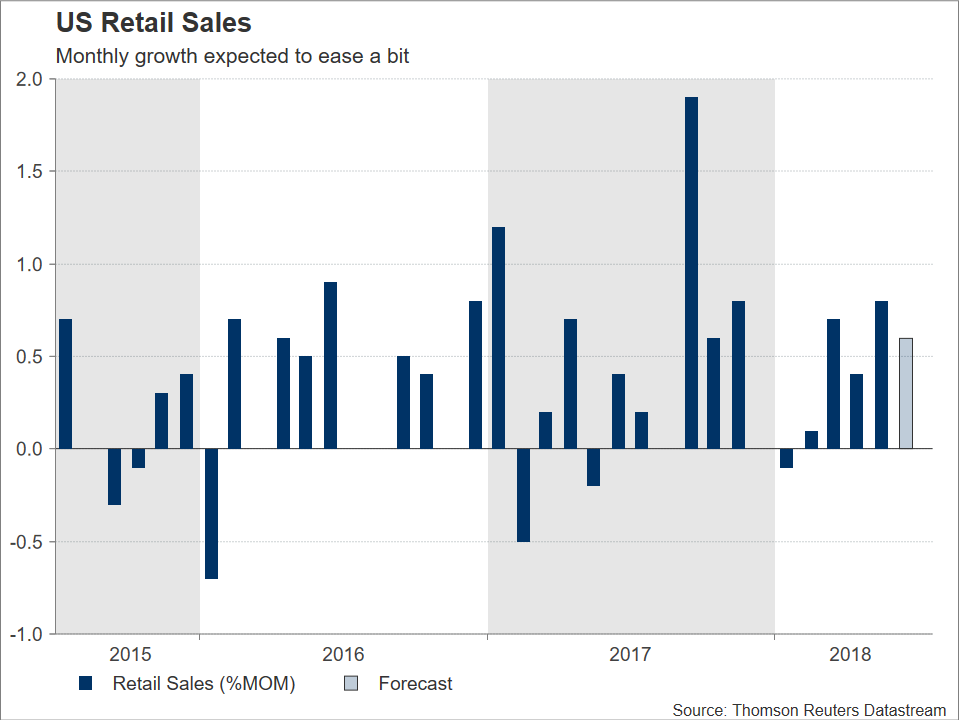

US retail sales data for June will be hitting the markets on Monday at 1230 GMT. Upbeat readings have the potential to boost market expectations for the delivery of two more rate hikes by the Federal Reserve by year-end, consequently boosting the dollar, and vice versa.

Retail sales are anticipated to grow by 0.6% m/m in June, a weaker pace relative to May’s 0.8% which constituted the largest advance since November 2017 and lent credence to expectations for robust US economic growth during Q2. Additionally, core retail sales, this being the measure of sales that excludes automobiles and which more closely aligns with the consumer spending component of GDP, is projected to expand by 0.4% on a monthly basis, again reflecting a slowdown compared to May’s 0.9%.

Consumer spending accounts for more than two-thirds of the US economy. Retail sales may not be perfectly correlated with consumption, but are still viewed as giving an insight on consumer spending numbers, a factor which increases the significance of the prints. Based on core retail sales data over the two previously reported months, economists projected consumer spending to have expanded by at least 3.5% on an annualized basis so far in Q2. This positively compares to the 1% growth during the first quarter.

Robust figures on Monday, besides adding to the conviction for strong growth during Q2 – Atlanta Fed’s GDPNow model estimates Q2’s annualized rate of expansion at 3.9% at the moment – are also likely to add to views for the delivery of two additional 25bps rate increases by the US central bank as the year unfolds, something which would put the total number of hikes during 2018 at four. Such an outcome is expected to support the greenback versus other currencies; the opposite holds true as well. Currently, markets have fully priced in an additional hike during 2018, while they assign a bit less than equal odds for a second one, according to Fed funds futures.

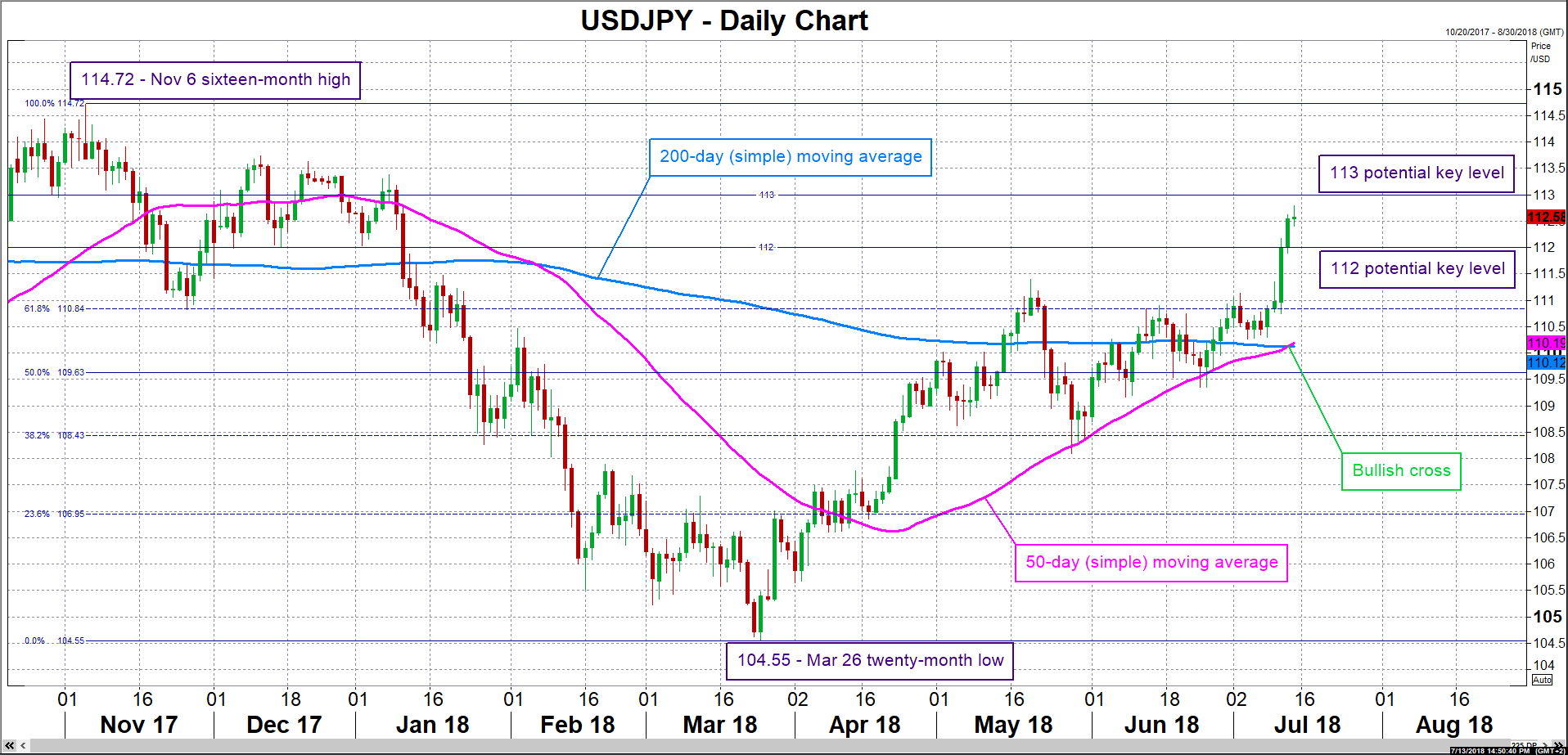

Focusing on USDJPY, the pair is trading at elevated levels, having reached a fresh six-month high of 112.79 during Friday’s trading. There are signs of an overbought market though, rendering a reversal in the near-term a possibility. Nevertheless, stronger-than-forecasted retail sales data on Monday are likely to boost the pair, with resistance to advances potentially taking place in the area around the 113 handle, a rather congested one in the past. An upside break would turn the attention to the 16-month high of 114.72 recorded in early November. Conversely, a downbeat release is expected to lead to a falling USDJPY, with support possibly occurring at the 112 round figure. Further below and in the event of steeper losses, the focus would turn to the region around the 61.8% Fibonacci retracement level of the November 6 to March 26 downleg at 110.84.

In terms of positioning on the dollar/yen pair, flows on the back of trade developments should also be considered; rising concerns over a full-blown trade between the US and China will probably benefit the safe-haven perceived yen, and vice versa. Lastly, July’s New York Fed manufacturing survey will be made public alongside the retail sales figures, while data on May business inventories are slated for release on the same day at 1400 GMT.