{kind=link}

U.S. stocks ended mixed overnight after the Fed held its policy rate steady at 4.25–4.50%, in line with market expectations. The dissenting votes from Governors Christopher Waller and Michelle Bowman in favor of a cut came as little surprise, reflecting known dovish leanings. However, Chair Jerome Powell’s tone in the press conference struck a more cautious chord than markets had anticipated.

Powell pushed back against speculation of a near-term pivot, stating firmly, “We have made no decisions about September.” That effectively left the door open, but offered little for those hoping for imminent easing. Powell also warned that while tariff-driven inflation may be transitory, “more persistent” effects couldn’t be ruled out.

Between now and the next FOMC meeting, two additional rounds of jobs and inflation reports will be released—giving the Fed a wider lens to assess policy needs.

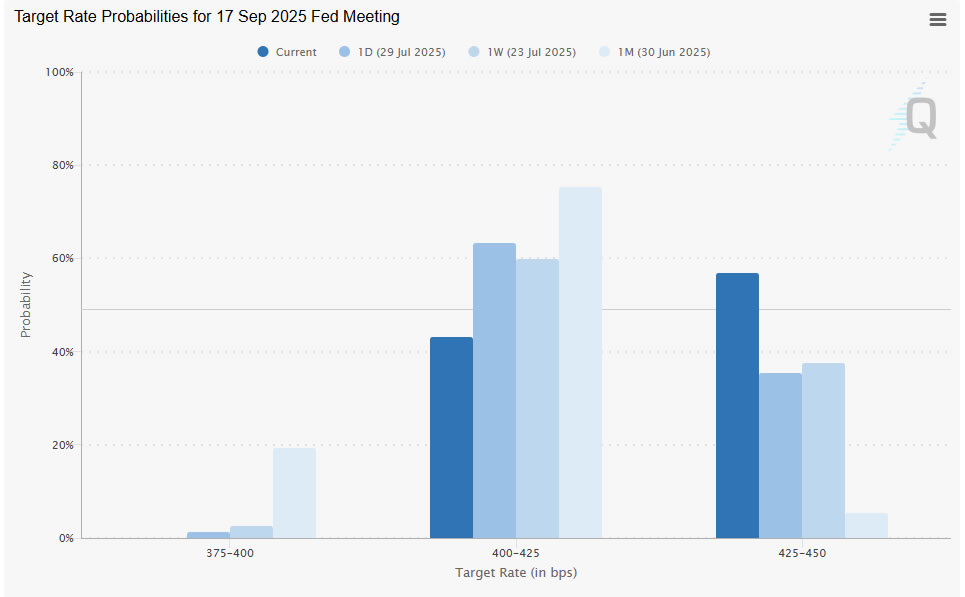

Traders responded by paring back bets for a September cut. Market pricing now sees just a 43% chance of easing at the next meeting, down from 65% a day earlier. The message: the Fed may be approaching the end of its pause, but it’s not ready to blink just yet.

Technically, while S&P 500’s up trend continued this week, it’s clearly continuing to lose upward momentum as seen in bearish divergence condition in D MACD. 6500 psychological level is likely to cap upside and bring consolidations. That’s slightly above a major fibonacci level of 61.8% projection of 3491.58 to 6147.43 from 4835.04 at 6476.35. Break of 6281.71 support will indicate that a near term correction has already started towards 55 D EMA (now at 6110.15).