{kind=link}

Politics and central bank events will be the main drivers in the markets this week, with economic data taking a back seat. FOMC policy decisions and press conference is one of the main highlights. Fed is expected to finally announce unwinding of its USD 4.5T balance sheet. But spotlight will first be on BoE Governor Mark Carney’s speech at IMF in Washington. Markets will look to Carney for his view on the chance of a November hike. Meanwhile, Germany and New Zealand will have their general elections the coming weekend. Talking about elections, Japan Prime Minister Shinzo Abe might announce to dissolve the Lower House and call for a snap election. UK Prime Minister Theresa May will deliver a Brexit speech in Italy on Friday. And there could be more verbal exchanges out of UK and EU ahead of the fourth round of Brexit negotiation starting next week. And, let’s not forget also US President Donald Trump will address the United Nations in New York on Tuesday when North Korea tensions are still present. Trump is given a chance to confront North Korean representative face-to-face.

Merkel’s CDU maintains lead according to latest poll

Ahead of the German election on September 24, latest poll reported by Bild am Sonntag showed that Chancellor Angela Merkel’s Christian Democratic Union (CDU) is maintaining solid lead at 36%. Rival Social Democratic Party (SPD) follows at 22%. Meanwhile, far right anti-immigrant Alternative for Germany (AfD) is staying as the strongest among the "small parties", at 11%, staying in the third place. The Left, Free Democrats (FDP), and the Green are at 10%, 9% and 8% respectively. It’s believed that with double digit support, AfD will very likely enter German parliament after the election. That will be the first presence of a right-wing party in the Bundestag in over half a century. According to the poll, 58% said that Merkel’s policies were partially responsible for the rise of the nationalist party AfD. Meanwhile, as FDP is likely to re-enter into the Parliament, FDP, Greens and the CDU could eventually form a so called "Jamaica coalition".

Kiwi to stay volatile on polls

New Zealand dollar trades mildly higher today but indecisiveness could remain ahead of the general election on September 23. The election is described by many as the closest contest in more than a decade. And so far, reactions show that Kiwi will dip whenever the opposition Labour Party is running ahead in polls. On the other hand, Kiwi will be lifted if ruling National Party is leading. Markets generally perceive that a change of government to Labour as a negative event. And analysts noted that the markets are not against the Labour, but just against change.

Japan PM Abe considering to call for snap election

In Japan, it’s reported that Prime Minister Shinzo Abe is considering to dissolve the Lower House and call for a snap election, as early as in late October. Abe’s approval rating sunk earlier this year and broke 30% mark in July on alleged scandals of government favoritism. However, the rising tensions with North Korea helped and lifted the rating back above 50%. A cabinet reshuffle in August also helped improved his popularity. Abe will be ending his term as ruling Liberal Democratic Party president next September. But an early election at the current time would help the party in extending theirs power beyond that.

Looking ahead

FOMC policy decision and press conference on September 20 will be a major focus. The Fed would formally announce the schedule of the long-awaited normalization of its US$ 4.5 trillion balance sheet. At the Addendum to the Committee’s Policy Normalization Principles and Plans released in June, Fed indicated how it intends to gradually reduce the balance sheet. We expect more details including the formal start day would be announced this week. Inflation has remained persistently soft despite the upside surprise in the August data. We believe some members would raise concerns that weak price levels might last longer than previously anticipated. There might be downward revisions in the inflation forecast in 2018. Meanwhile, there are some speculations that the Fed might reduce its average Fed funds rates projections.

RBA would release the minutes on September 19. The central bank left the cash rate unchanged at 1.5% in September. While remaining confident over the economic outlook, the members warned of the recent appreciation in Australian dollar. We do not expect much news from the minutes. BoJ will also meet this week and it will likely be a non-event.

Here are some highlights for the week ahead:

- Monday: Eurozone CPI final; Canada foreign securities transactions; US NAHB housing index

- Tuesday: RBA minutes, Australia house price; German ZEW economic sentiment; Canada manufacturing sales; US housing starts and building permits, current account, import price

- Wednesday: New Zealand current account; Japan trade balance; German PPI; UK retail sales; US existing home sales, FOMC rate decision and press conference

- Thursday: BoJ rate decision; New Zealand GDP; Swiss trade balance, SECO economist forecasts; ECB bulletin; UK public sector net borrowing; US jobless claims, Philly Fed survey; Canada wholesale sales

- Friday: Eurozone PMIs; Canada CPI, retail sales; US PMIs

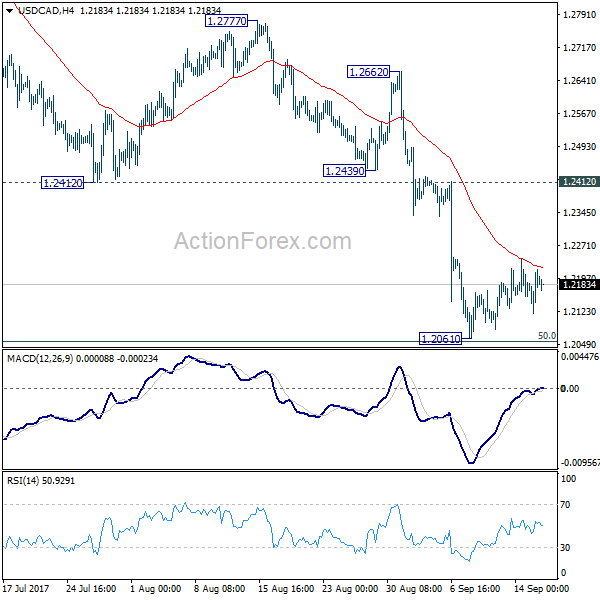

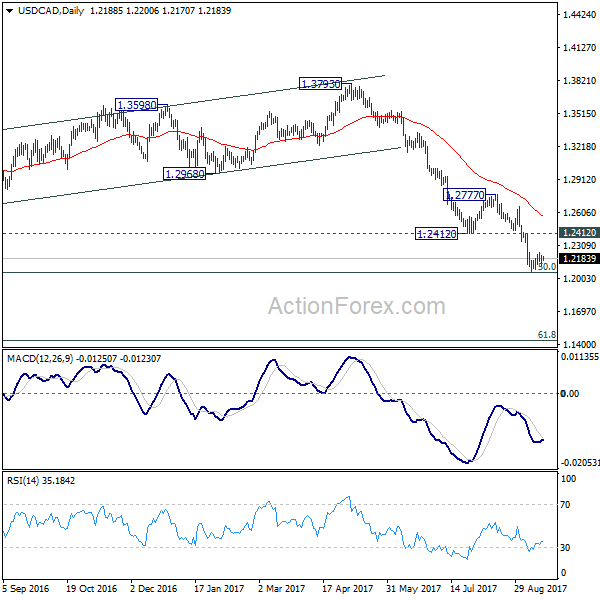

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2175; (R1) 1.2234; More….

Intraday bias in USD/CAD remains neutral as consolidation from 1.2061 temporary low continues. The corrective price actions so far suggests that larger decline is not completed yet. And firm break of 1.2049 key fibonacci level will pave the way to next fibonacci level at 1.1424. Still, we’d remain cautious on strong support from 1.2048 to bring sustainable rebound. But still, break of 1.2439 support turned resistance is needed to be the first sign of trend reversal. Otherwise, outlook will remain bearish.

In the bigger picture, current downside acceleration is raising the chance that whole long term rise from 0.9406 (2011 low), and that from 0.9056 (2007 low) is completed at 1.4689. Focus is now on 50% retracement of 0.9406 to 1.4869 at 1.2048. As long as this level holds, we’d still favor that case that fall from 1.4689 is a correction. However, firm break of 1.2048 will indicate that fall fro 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Sep | -1.20% | -0.90% | ||

| 9:00 | EUR | Eurozone CPI M/M Aug | 0.30% | -0.50% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Aug F | 1.50% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI – Core Y/Y Aug F | 1.20% | 1.20% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jul | 4.46B | -0.92B | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 67 | 68 | ||

| 20:00 | USD | Net Long-term TIC Flows Jul | 42.3B | 34.4B |