{kind=link}

Dollar is under selling pressure again in early US session after weaker than expected inflation data. Headline CPI rose 0.5% mom, 2.2% yoy in Septembers, up from 0.4% mom, 1.9% yoy in August, but missed expectation of 0.6% mom, 2.3% yoy. Core CPI rose 0.1% mom, 1.7% yoy, comparing to August’s 0.2% mom, 1.7% yoy. More importantly, core CPI missed consensus of 0.2% mom, 1.8% yoy. Retail sales came in slightly better than expected and rose 1.6% in September. Ex auto-sales rose 1.0%. Dollar was sold off earlier this week after FOMC minutes showed policymakers are concerned with sluggishness in inflation. It’s resuming that selloff now and that should keep Dollar as the weakest one for the week.

Euro turned mixed on ECB report

Euro trades lower today on media report that ECB is going to half asset purchase target. Markets seems to be dissatisfied with it and in particular, policymakers are divided on how long would the program be extended. The current EUR 60b per month pace could be lowered to EUR 30b per month, starting January. Separately, President Mario Draghi reiterated that interest rate will remain at the current record low "well past" the end of the asset purchase program. He emphasized that the "’well past’ is very, very important in anchoring rate expectations." ECB is widely expected to "recalibrate" its asset purchase program this month on October 26.

Released from Europe, Swiss PPI rose 0.5% mom, 0.8% yoy in September. German CPI was finalized at 0.1% mom, 1.8% yoy in September.

Sterling to end as the strongest one for the week

Much volatility is seen in Sterling this week and the pound could end the week as the strongest one. A German newspaper Handelsblatt quoted unnamed source that EU could give that extension to UK under the conditions that the latter will fullfil all obligations as a member country. However, UK will be required to give up its voting rights. If it’s true, more time will be allowed for business and citizens of both UK and EU to adjust to the changes.

Meanwhile, BBC reported that a draft paper was submitted to the 27 EU states by European Council President Donald Tusk. The paper indicates that free trade talks could start as soon as December. It’s near impossible that EU officials will give a "go" signal for trade discussion at the October 19/20 summit due to lack of "sufficient progress" in the negotiations. But opening up the case for start trade agreements in December could give UK the "carrots" for being more decisive on closing issues like the divorce bill.

China trade surplus narrowed

Released from China, trade surplus surprisingly narrowed to a 6-month low of US$28.5B in September, from US$42B a month ago. The market had anticipated a milder drop to US$39.5B. Growth in exports improved to 8.1% y/y from 5.5% in August, while growth imports accelerated significantly to +18.7% from July’s +13.3%.

Notwithstanding a disappointing headline, the report continued to paint a healthy picture on China’s economic outlook. A stronger-than-expected imports growth underpinned domestic economic strength. Exports growth, despite missing consensus, still picked up from the same period last year.

More importantly, a narrowing trade surplus could tame the US’ complaint of China’s currency manipulation. This should help the government maintain a stable and modestly strong renminbi as CCP’s 19th national congress approaches. More in Strong Domestic Demand Despite Weak Surplus Headline.

Elsewhere

New Zealand Business NZ manufacturing index dropped to 57.5 in September. Japan M2 rose 4.1% yoy in September.

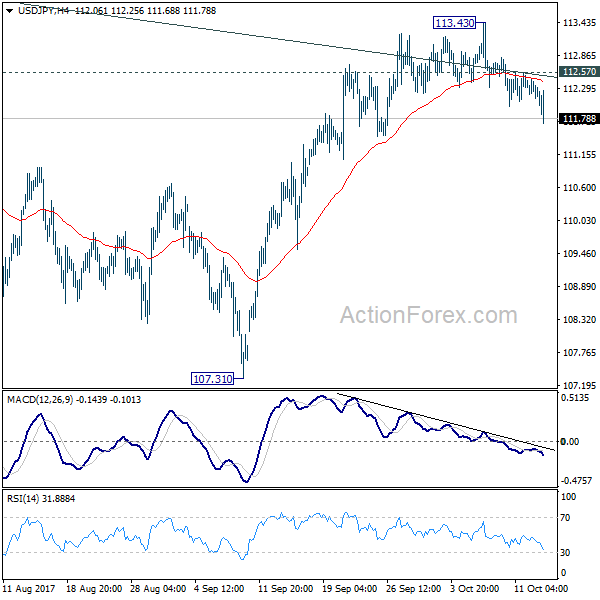

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.10; (P) 112.31; (R1) 112.49; More…

USD/JPY’s fall from 113.43 short term top extends in early US session and intraday bias remains on the downside. Deeper decline would be seen to 55 day EMA (now at 111.35) first. On the upside, above 112.57 minor resistance will turn intraday bias neutral first. But risk will stays on the downside as long as 113.43 resistance holds.

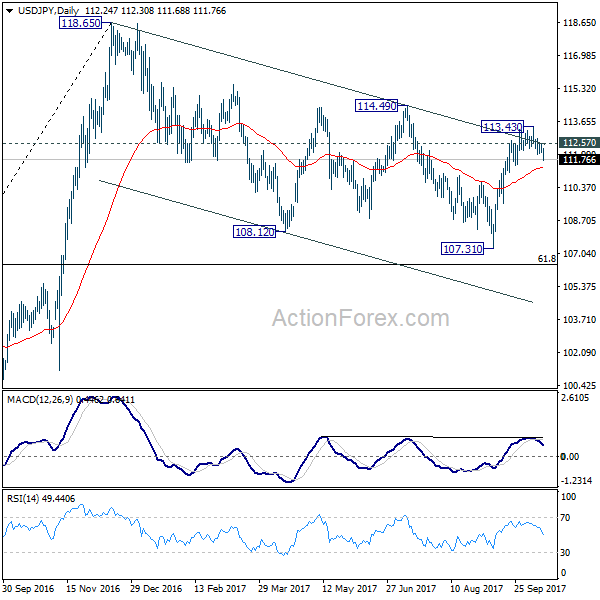

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It’s unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don’t expect a break there on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business Performance of Manufacturing Index Sep | 57.5 | 57.9 | ||

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Sep | 4.10% | 4.00% | 4.00% | |

| 00:30 | AUD | RBA Financial Stability Review | ||||

| 03:30 | CNY | Trade Balance (USD) Sep | 28.5B | 38.1B | 42.0B | |

| 03:30 | CNY | Trade Balance (CNY) Sep | 193B | 266B | 287B | |

| 06:00 | EUR | German CPI M/M Sep F | 0.10% | 0.10% | 0.10% | |

| 06:00 | EUR | German CPI Y/Y Sep F | 1.80% | 1.80% | 1.80% | |

| 07:15 | CHF | Producer & Import Prices M/M Sep | 0.50% | 0.30% | 0.30% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Sep | 0.80% | 0.60% | 0.60% | |

| 12:30 | USD | CPI M/M Sep | 0.50% | 0.60% | 0.40% | |

| 12:30 | USD | CPI Y/Y Sep | 2.20% | 2.30% | 1.90% | |

| 12:30 | USD | CPI Core M/M Sep | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Core Y/Y Sep | 1.70% | 1.80% | 1.70% | |

| 12:30 | USD | Advance Retail Sales Sep | 1.60% | 1.50% | -0.20% | -0.10% |

| 12:30 | USD | Retail Sales Less Autos Sep | 1.00% | 0.90% | 0.20% | 0.50% |

| 14:00 | USD | U. of Michigan Confidence Oct P | 95.1 | 95.1 | ||

| 14:00 | USD | Business Inventories Aug | 0.50% | 0.20% |