{kind=link}

Sunrise Market Commentary

- Rates: Front end US yield curve rises further

The main item on today’s agenda is the US non-manufacturing ISM which is expected to remain very strong. In theory, that’s negative for US treasuries, but we don’t expect a strong reaction. The front end of the US yield curve continues to underperform, discounting already two rate hikes for 2018 going into next week’s FOMC meeting. - Currencies: Dollar rebound stalls despite rising interest rate support

The dollar profited temporary from the tax bill approval in the US Senate yesterday, but the rally stalled as US equities turned south. Today’s eco data probably won’t cause a big directional USD move. Even so, the ongoing rise in ST US yields is making USD shots expensive and should protect the USD downside going into the payrolls and next week’s Fed meeting

The Sunrise Headlines

- US stock markets ended varied with Nasdaq (-1%) underperforming as a last-minute change to Senate Republicans’ tax-overhaul plan may mean higher taxes for corporations, including IT firms. Asian bourses trade mixed overnight.

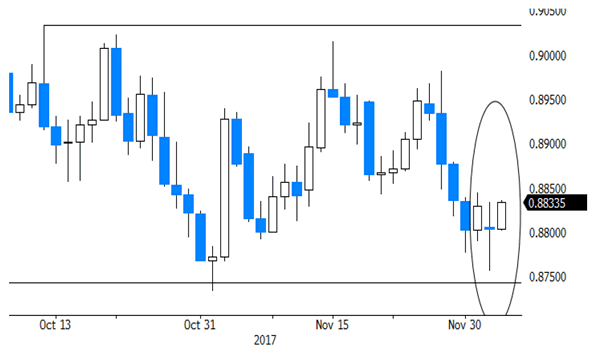

- A carefully choreographed divorce deal between London and Brussels was derailed at the eleventh hour after Northern Ireland’s hardline Unionists rejected Theresa May’s agreement to potentially keep the province aligned with EU law after Brexit. EUR/GBP rose back above 0.88.

- Growth in China’s services sector activity picked up to a three-month high in November (PMI: 51.9), buoyed by a solid rise in new business, though the rate of expansion remained moderate and weaker than the long-run trend.

- The Reserve Bank of Australia kept its policy rate unchanged at 1.5%, but a shift in the inflation language signalled that the central bank is arguably offering a less dovish tone. AUD/USD rises from 0.76 to 0.7650.

- The Reserve Bank of New Zealand’s new assumption that global inflation will stay lower for longer means it is more exposed to the risk of prices picking up, Acting Governor Spencer said. NZD/USD moves higher towards 0.69.

- European Finance Ministers shifted power from the north of the continent to the south, providing a boost to opponents of austerity policies. They chose Portugal’s FM Centeno to lead the Eurogroup to succeed Dijsselbloem.

- Today’s eco calendar contains November services PMI’s in EMU (final), the UK and the US (ISM). EMU retail sales are also up for release

Currencies: Dollar Rebound Stalls Despite Rising Interest Rate Support

Dollar rebound stalls despite higher ST yields

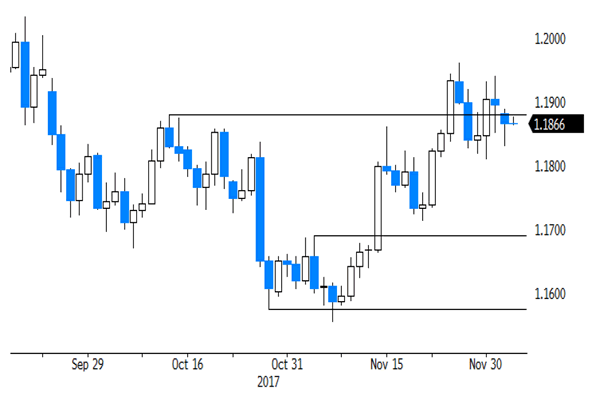

European (and US) markets initially reacted in a positive way to the approval of the US tax bill. European equities jumped higher. ST US yields rose further and the dollar extended cautious gains. USD/JPY tested the 113 area. The gain of the dollar against the euro was again more limited. Later in US dealings, tax optimism dwindled, reversing most of the intraday ‘reflation trade’. The dollar returned a big part of the early gains. USD/JPY closed the session at 112.41 (from 112.17 on Friday). EUR/USD finished the day at 1.1866 (from 1.1896). Asian equity indices show a mixed picture. A new setback in US tech stocks also affects (parts of) the Asian markets. The dollar ‘bottoms’ after the late session setback in the US yesterday evening. USD/JPY trades in the 112.60 area. EUR/USD is changing hands near 1.1870 area. The RBA as expected left its policy rate unchanged at 1.50%, but expects that a stronger labour market could see some lift in wage growth over time. Better than expected retail data also supported the Aussie dollar. AUD/USD trades in the mid 0.76 area. The kiwi dollar made some modest gains after RBNZ’s Spencer indicated that the bank could give more weight to output employment and financial stability.

The eco calendar contains the final EMU (services) PMI’s, EMU retail sales and the US non-manufacturing ISM. EMU PMI’s are expected to confirm the strong growth momentum (57.5 for the composite PMI). Retail sales are expected to have declined in October (-0.7% M/M and 1.6% Y/Y). We don’t expect the EMU data to have a lasting impact on the euro. The US non-manufacturing ISM is expected to ease slightly from 60.1 to 59, still a very high level. Last week’s manufacturing ISM showed a similar pattern. We have no reason to take a different view from the consensus. Of late, markets mostly reacted rather muted to (US) activity data. Investors are more sensitive to price data.

The dollar showed a mixed picture last week, rebounding against the yen but holding relatively soft against the euro. Yesterday, the pattern initially continued, but the USD rebound was aborted by a new up-tick in US equity volatility later in the session yesterday. The US 2-yr yield continues an astonishing rise (currently above 1.80%!), but it was only of little help for the dollar of late. Even so, it should at least help to put a floor for the US currency as USD shorts are becoming ever more expensive. We don’t expect a really big directional move ahead of next week’s Fed policy decision/statement.

That said, except for high profile negative news from the US (or negative risk sentiment) we see no reason for EUR/USD to rise beyond the 1.1961/1.20 area. The downside of USD/JPY looks better protected, but the rebound might slow if it isn’t supported by developments on other markets.

From a technical point of view: EUR/USD set a post-ECB low mid-November, but dollar momentum wasn’t strong enough. EUR/USD regained the 1.1880 MT correction top, opening the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. For now, there is no clear technical signal. The USD/JPY momentum deteriorated early November. USD/JPY dropped below the 111.65 neckline, but there was no aggressive follow-through selling. Last week the pair even succeeded a nice rebound, calling off the downside alert. The pair again hovers in the 110.84/114.73 consolidation range. We amend our ST bias on the pair from negative to neutral.

EUR/USD: rally aborted, but no clear trend yet

EUR/GBP

Sterling hit by last-minute Brexit failure

Brexit headlines caused a rollercoaster ride for sterling yesterday. UK PM May met with EU Commission president Juncker. EUR/GBP initially hovered in the 0.8825 area. Around noon there were press headlines from several sources that EU’s Barnier had indicated that negotiations on the separation issues were headed for a breakthrough. Sterling jumped higher across the board as markets assumed that Brexit negotiations could move to the content of the new relationship between the UK and the EU post Brexit. However, at a joined press conference, UK PM May and EC’s Juncker said that progress had been made, but no final agreement was reached. Sterling reversed most of the intraday gains. EUR/GBP finished the session at 0.8803. GBP closed the session at 1.3480.

Overnight, BRC UK retail sales rebounded to 0.6% Y/Y. However, it doesn’t help sterling. The UK currency remains under pressure. Markets are disappointed on yesterday’s last minute failure to reach a separation deal. Both parties are still trying to reach a deal to be proposed to the EU summit next week. Yesterday’s failure is the perfect illustration of the difficult balancing act that PM May faces and will continue to face during the next stages of the negotiations. Today, the UK services PMI will be published. A slight decline from 55.6 to 55 is expected. The report probably will only be of intraday significance for sterling trading. The focus remains on Brexit. Sterling remains in the defensive, unless there is hard evidence of a deal.

MT view/technical picture: A BoE driven sterling rebound ran into resistance early last month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral mid-November. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: downside test rejected as Irish border deal fails last minute