{kind=link}

Here are the latest developments in global markets:

FOREX: The dollar index was little changed after recording sharp losses the previous day as investors expected a more hawkish rate outlook by the Federal Reserve. The aussie was on a positive footing versus the greenback after better-than-anticipated employment figures.

STOCKS: The Nikkei 225 finished lower by 0.3% and the Hang Seng was last down by 0.3%; most major Asian benchmarks headed lower though losses were limited. Euro Stoxx 50 futures traded lower by 0.3% at 0713 GMT, with contracts on the Dow, S&P 500 and Nasdaq 100 all being up 0.1%.

COMMODITIES: WTI and Brent crude traded higher by 0.3% and 0.6%, at $56.76 and $62.79 a barrel respectively. Yesterday’s weekly EIA report showed a bigger-than-anticipated drawdown in US crude oil inventories. Gold was slightly higher at $1,256.80 an ounce. The precious metal gained on the back of dollar weakness yesterday, adding 1.0% on the day.

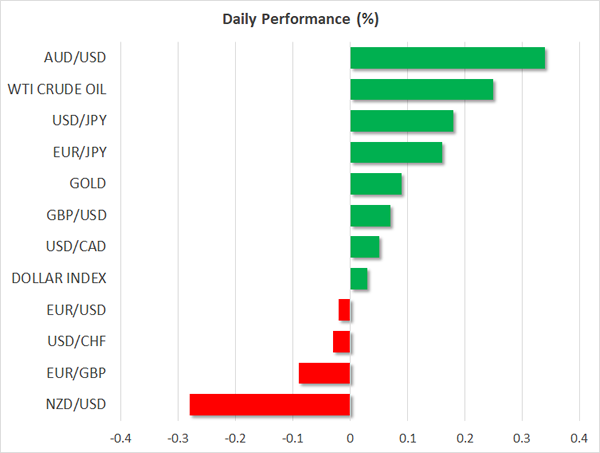

Major movers: Dollar consolidates losses; aussie maintains positive momentum after upbeat employment figures

The dollar’s index against a basket of currencies was marginally higher as European traders were about to get on their desks to begin their trading day. Still, the gauge was not far above 93.33, a one-week low tracked earlier. The US currency suffered losses as the Fed maintained its projections for three more interest rate increases in 2018 and 2019; market participants were anticipating a more hawkish stance. The 25 bps interest rate hike that was expected was of course delivered to drive the fed funds rate to a range of 1.25-1.50%.

Core inflation figures coming in below expectations yesterday also acted as a drag on the greenback, casting additional doubts on whether inflation would soon rise to the Fed’s target of 2% – it should be mentioned that the US central bank though uses the core PCE measure as its gauge for inflation. Not everything was negative for the dollar though, as Congressional Republicans arrived at a deal on final tax legislation on Wednesday, with a vote expected next week.

Dollar/yen was higher by 0.2% at 112.73. Yesterday the pair lost 0.9%. Euro/dollar and pound/dollar were not much changed, consolidating yesterday’s gains that saw the pairs move above the 1.18 and 1.34 handles respectively. Earlier in the day, euro/dollar touched a one-week high of 1.1843.

Aussie/dollar was up by 0.3%, trading not far below 0.7674, the one-month high it hit earlier on the day. Australia’s currency was supported by positive data on employment released during the Asian session. Unlike the aussie, the New Zealand dollar didn’t manage to maintain momentum from previous days. Kiwi/dollar was down by 0.3% at 0.7000, though it still traded relatively close to its highest since late October tracked yesterday.

Besides the Fed, the Chinese central bank also slightly raised rates for its reverse repos and medium-term lending facility, though reaction in the markets to the decision was fairly limited.

Day ahead: European central banks decide on rates; US & UK retail sales attract attention

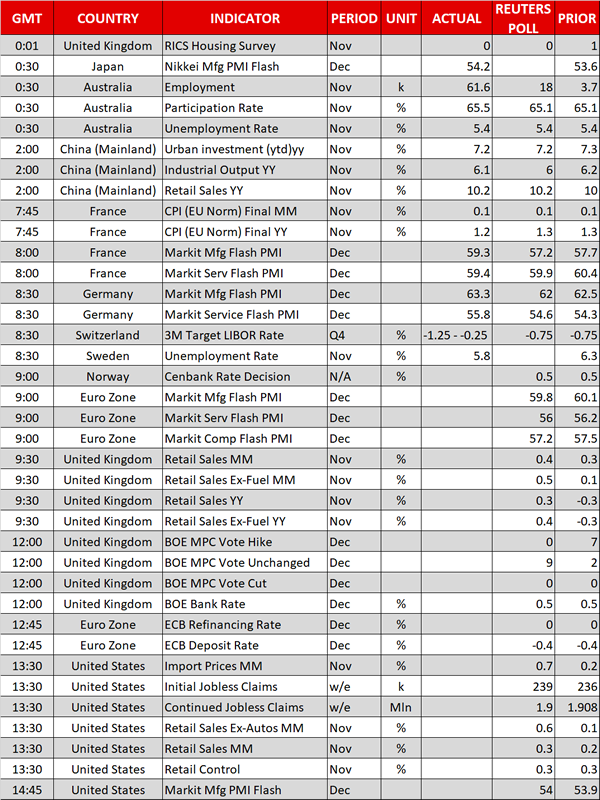

Traders are expected to have a relatively busy day at the office on Thursday as several economic reports out of the US, the UK and the EU will be published, while central bank events would be in the spotlight, with the Bank of England, the European Central Bank, the Norges Bank and the Swiss National Bank making announcements on interest rates and publishing their economic projections.

The Bank of England will be the first in line among its European peers to reveal its rate decision at 1200 GMT. Despite inflation crossing far above the BOE’s target of 2.0%, expectations are for rates to remain flat at 0.50%. However, the markets will be looking forward to the monetary policy statement to identify any updates on the BoE’s plans to tighten monetary stimulus in the coming years.

At 1245 GMT the European Central Bank is anticipated to hold benchmark interest rates unchanged and confirm its decision to halve its asset purchases starting next year. As this is widely expected, investors’ focus would turn to the central bank’s macroeconomic projections on economic growth and inflation. The ECB will likely revise up its growth forecasts, while it will also deliver initial 2020 estimates. Following the decision, the ECB chief Mario Draghi will be holding a press conference at 1330 GMT.

The Swiss National Bank and Norway’s central bank are also completing their meetings on monetary policy today.

In terms of data, Eurozone flash Markit PMI readings for the month of December due at 0900 GMT are forecasted to appear slightly weaker than in November, with the composite index sliding by 0.3 points to 57.2. In contrast, first estimates on the US manufacturing and service PMIs are expected to inch up (1445 GMT).

British and US retail sales are expected to surprise to the upside. Particularly, consumers’ spending in the UK due at 0930 GMT is anticipated to rise by 0.3% y/y in November after falling for the first time in four years, while the monthly US gauge is projected to climb by an equivalent percentage.

In addition, initial jobless claims out of the US will be available at 1330 GMT, with analysts projecting the number of people claiming unemployment benefits to increase moderately by 3,000 in the week ending December 8 to 239,000.

Elsewhere, the Bank of Canada’s chief Stephen Poloz will give a speech at the Canadian Club of Toronto at 1740 GMT. A press conference would follow.

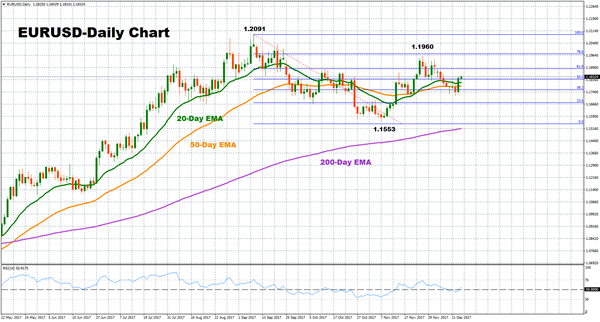

Technical Analysis: EURUSD consolidates gains but short-term risks tilted to the upside

EURUSD is currently neutral as it has been ranging around the 1.1800 key-level over the last four days. However, the bullish cross between the 20 and the 50-day exponential moving average lines as well as the RSI starting to slope upwards may signal that upside movements could emerge in the near-term.

Should the pair head up, immediate resistance could be found at 1.1882, this being the 61.8% Fibonacci mark of the downleg from 1.2091 to 1.1553. Further increases could also target a previous peak at 1.1960. However, if the ECB delivers a dovish message on the eurozone’s economic outlook, prices could decline. In this case, the area around the current level of the 20-day EMA 1.1799 could provide support – notice that price action is currently taking place not far above this level.