The last quarter of 2018 was a tough one for oil producers as fears over a global growth slowdown and concerns on plentiful production sent prices to 1 ½-year lows. To reverse the slump, OPEC and non-OPEC members clinched a deal to cut output as of January 1 despite previously increasing levels, with the market responding immediately, sending prices higher by 18% since the start of the new year. But moving ahead, the outlook remains fragile as some issues still need to be sorted out.

Supply troubles

Last Tuesday, Saudi Arabia, the world’s top oil exporter, said that it would voluntarily cut March production to around 9.8 million bpd, 500,00 bpd more than it had initially pledged under the latest 1.2mln bpd output cut deal signed with its OPEC plus counterparts in December. On the same day, the IEA’s monthly report revealed that compliance among OPEC members was estimated around 86% with Kuwait and UAE reducing production more than promised as well. On the negative side the non-OPEC group scored on average at a minimal 25%, with Russia, the second biggest oil producer after the US, making only 18% of its pledged output cut.

While the low compliance rates by non-OPEC members is not a new tendency, the miss in targets could lead to a dull and unsatisfactory rally in oil prices, potentially putting the Saudi Arabian government at risk of falling short of its 2019 budget targets if prices fail to rise towards its $80-$85 breakeven point according to the IMF estimates – especially when a more evidently slowing global economy threatens demand growth and steeper output cuts could be less desirable at a time when political tensions in other key oil areas are already restricting deliveries.

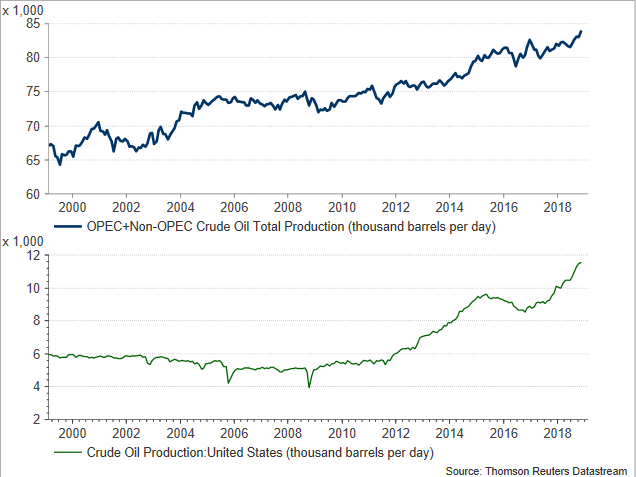

Oversupply in the US has been long disturbing OPEC’s plans for higher prices and it will probably continue doing so in the next two years as domestic production is expected to hit new highs in 2019 and 2020. It is also worth noting that new pipelines at the vital Permian Basin in Western Texas are anticipated to start operating in the second half of 2019, adding more bearish supply pressure to oil markets.

OPEC and its allies will gather next in Vienna on April 17-18 to review the pact. Taking the above into account and aiming to keep supply and demand in balance, the group could renew the output cut agreement if prices are not on desired levels by that day.

Meanwhile, the Paris-based IEA raised its supply growth forecasts for 2019 to 1.8 mln bpd from 1.5 mln bpd previously, while keeping demand growth predictions steady at 1.4 mln bpd.

Sanctions waivers expire

In geopolitics, Iran is keeping a hard line on its nuclear program despite US sanctions hurting the economy badly. Crude oil exports in January dropped to the lowest since 2014 and analysts predict real GDP to decline by 3.6% in 2019 after contracting by 1.4% in 2018. Yet conditions could have been worse in the absence of US waivers to eight importers of Iranian oil such as China, Japan and India. But at the beginning of May, the six-month exemption expires, and the Trump administration will likely take a glance at oil prices before making any decision. Since the US favours lower prices, only a significant drop from current levels (below $50/barrel) could see the US reducing the number of waivers. Alternatively, a spike above $80 could allow for more Iranian oil in the markets, with the US extending the waivers.

Oil-rich Venezuela has been also sanctioned by the US last month as the administration tries to limit financial support for the president Nicolas Maduro. However, diminished supply from the country, which has been weighing well before the recent political turmoil began, seems to have caused little reaction to the oil market so far. Nevertheless, developments in the area will continue to attract interest.

US-China trade war to weigh on demand

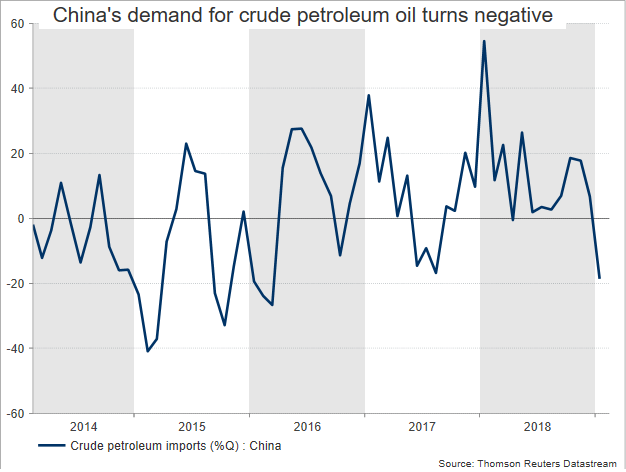

The months-long US-Sino trade war is the hottest topic in oil markets. China has already started to feel the pinch from US tariffs and undoubtedly further escalation in tensions would only bring more harm to the world’s second largest oil consumer and therefore to oil demand.

Although headlines early on Friday created impression that last week’s trade negotiations in Beijing made a hole in the water, both sides appeared satisfied during the weekend, with the US President twitting that big progress has been made “on many fronts”. China reported improvement as well, saying that a consensus in principle on some key areas has been reached. Still, with neither side giving specific details on what has been agreed, some caution remains on storage as discussions move to Washington. The US administration is expected to keep pressure on China until it forces Beijing to reform its regulatory practises – especially those that force technology transfers to China. Should talks complicate before the March 1 deadline, blocking the path for a constructive summit between Trump and Xi Jinping as soon as next month, US import tariffs on $200 billion Chinese products are set to rise from 10% to 25% unless President Trump decides to move the deadline forward, which is not unlikely given the recent headlines over a 60-day extension and the data volatility in the US and elsewhere. But even if Washington shows sympathy, allowing more time for negotiations to progress, the business sentiment is not expected to get any better as companies will wisely avoid moving on with their investment plans until the dark clouds clear.

Meanwhile in the markets

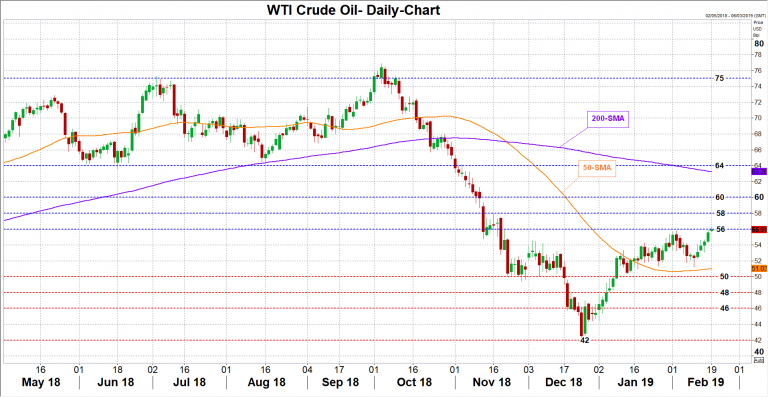

WTI crude oil has turned higher after hitting a 1 ½ -year low of 42.36, with the price currently pushing hard to overcome resistance at 56 that could allow for more buyers to enter the market. Should tensions in the Middle East intensify restricting the flow of deliveries, WTI crude could see resistance coming at 58 and then at 60. Crawling higher, significant interest is expected to gather around the previous 64 support level, though only a close above 75 would shift the outlook to a bullish one.

In the negative scenario, extensive pumping in the US and a steeper global economic slowdown triggered by an even more aggressive trade war could send the price down to the 50 support mark. Piercing that floor, bearish action could pause within the 48-46 area, while steeper declines could also challenge the 42 bottom.

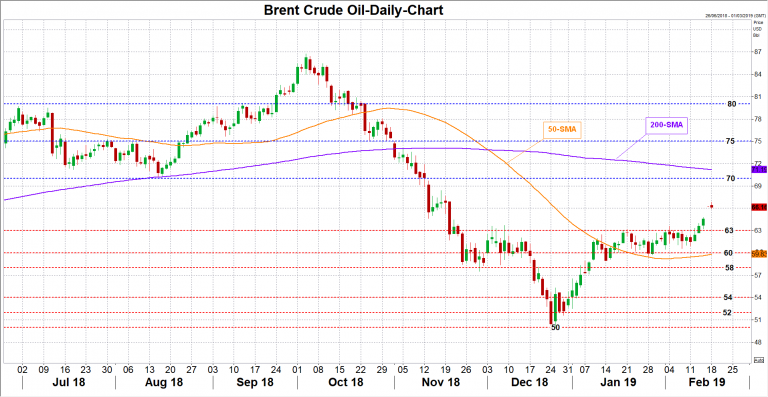

The London-based Brent is printing three-month highs above the 66 level but investors are waiting to confirm the rally’s sustainability above the 70 mark where the price rebounded in late-August. Should the price shoot even higher surpassing the 200-day moving average currently at 71 and the 75 barrier, resistance could run up to 80.

On the downside, the market could face a wall in the 60-63 congested area before testing support near 58. An extension lower would likely see negative momentum slowing somewhere between 54-52, while beneath that, the bears would need to break the bottom at 50 to keep the market under their control.

{kind=link}