Tuesday July 11: Five things the markets are talking about

Capital markets continue to watch for cues on monetary policy.

Questions on the U.S inflation outlook are certain to be front and center for Fed head Janet Yellen tomorrow – she is due to testify on the semi-annual Monetary Policy Report before the House Financial Services Committee.

Inflation data will in fact cap this week with Friday’s consumer price report where minimal pressure is the market consensus. Also on Friday, U.S retail sales is expected to show a minimal gain once again, held down by weak auto sales.

Currently, global equities are little changed, unlike bonds, which are extending their slump triggered by more ‘hawkish’ rhetoric from central banks.

Normalization of monetary policy is holding the ‘big’ dollar firm and limiting its downside.

1. Stocks mixed results

Asian markets mostly climbed overnight supported by technology companies who mirrored gains in their U.S counterparts.

In Japan, the Nikkei stock index ended up +0.6%, buoyed by the weaker yen (¥114.32), while Australian shares erased losses and ended slightly higher.

In Hong Kong, stocks extended this week’s rally, posting their best day in four months overnight, bolstered by strong gains among financial sector stocks. The Hang Seng Index rose +1.5%, while the China Enterprises Index gained +2.0%.

In China, stocks diverged, with the blue-chip index hitting a fresh 18-month high as investors favoured solid fundamentals, while small-caps extended a fall on expectations more equity issuance would soften valuations. The blue-chip CSI300 index rose +0.5%, while the Shanghai Composite Index lost -0.3%.

In Europe, stocks opened higher, but have since turned due to little major news. Crude prices are again dragging down energy stocks in the FTSE 100 as investors turn their attention to Fed Chair Yellen’s comments in Congress tomorrow and upcoming U.S reported earnings.

U.S stocks are set to open little changed.

Indices: Stoxx50 flat at 3,477, FTSE -0.6% at 7,324, DAX +0.2% at 12,472, CAC-40 flat at 5,168, IBEX-35 -0.2% at 10,491, FTSE MIB +0.4% at 21,268, SMI -0.5% at 8,894, S&P futures flat

2. Oil steadies but outlook remains weak, gold lower

Oil prices have steadied overnight after almost a week of sharp falls, but the outlook remains weak amid oversupply issues.

Benchmark Brent crude is down -10c at +$46.78 a barrel, while U.S light crude is -5c lower at +$44.35.

Signs of strong short-term demand are capping losses for now – gas demand tends to increase in the northern hemisphere in the summer as U.S drivers take to the road.

Fundamental and technical dynamics for crude have not changed; the world is awash with crude supply.

Note: Brent prices are -17% below their 2017 opening despite a deal OPEC to cut production from January.

On Friday Baker Hughes data showed that U.S energy firms added +7 oil drilling rigs last week, marking a 24th week of increases out of the last 25 and bringing the total count up to +763, the most since April 2015.

Note: U.S oil production has risen over +10% since mid-2016 to +9.34m bpd.

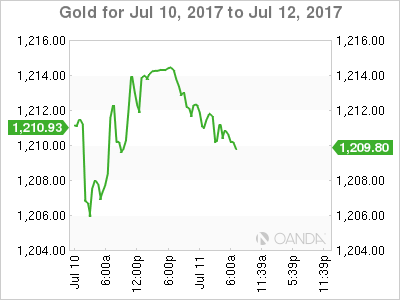

Gold prices (-0.3% to +$1,210.88 an ounce) have edged lower on a firmer dollar after touching near four-month lows in the previous session as the market waits for cues from the central bank on the path of U.S. interest rate hikes.

3. Bonds market selloff resumes, yields approaching last weeks high

San Francisco Federal Reserve President John Williams said overnight in Sydney that “it was a reasonable view to expect one more rate hike this year, and his own view was to start adjusting the central bank’s balance sheet in the next few months.”

Yields on 10-year Treasury’s have backed up +2 bps to +2.392%, while German bund yields climbed to +0.559% from +0.539%.

Investors should expect further pressure on yields as the U.S Treasury this week will auction a combined +$56B in notes and bonds.

Note: +$24B in three-year notes will be auctioned today, while +$20B in reopened 10-year notes on Wednesday, and +$12B in opened 30-year bonds on Thursday.

Elsewhere, Japan’s Ministry of Finance confirmed that Japanese investors have returned to owning French government bonds (OAT’s) after Macron’s election win.

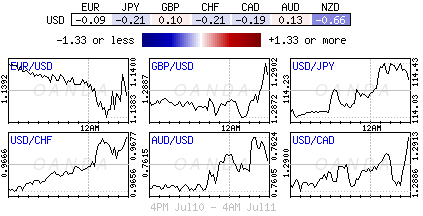

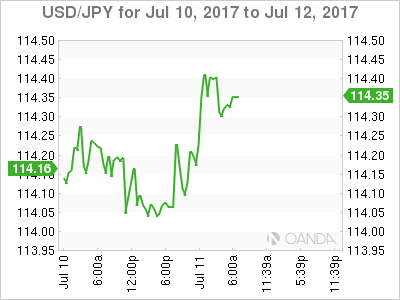

4. Dollar makes new highs against yen

Rate differentials are hurting JPY (¥114.27). The yen remains under pressure as Japanese monetary policy looks set to remain ultra loose, while the Fed is raising interest rates and other central banks, including in the eurozone, U.K, Canada and Scandinavia, switch their bias toward tightening policy.

The market believes that the Bank of Japan (BoJ) would be the only G-10 central bank not starting a rate normalization process at the latest by next year.

Elsewhere, sterling (£1.2916) is rallying before a speech by Bank of England policymaker Ben Broadbent (07:00 am EST) – anymore rate rise hints is expected to lift the pound further. GBP/USD is up +0.2%, while EUR/GBP is down -0.2% at €0.8833.

For the loonie (C$1.2909), the market seems somewhat divided on whether the Bank of Canada (BoC) will raise rates tomorrow (10:00 am EST), but data from the overnight index swaps market shows that money markets are almost fully priced for a +25 bps increase, while an +80% chance of a second hike has been implied by December.

5. U.S small-business confidence dragged by senate gridlock

Data this morning stateside showed that small-business owners’ confidence about their economic situation declined last month as the U.S Senate remains in gridlock over the health-care reform bill.

The National Federation of Independent Business’s (NFIB) small-business optimism index fell to 103.6 from May’s reading of 104.5.

Note: The index rose sharply after the 2016 presidential election and reached a peak of 105.9 in January.

The result sunk well below market expectations of 104.5.