- As expected, the ECB cut policy rates by 25bp today, bringing the deposit rate to 2.25%.

- The guidance struck a dovish tone, noting downside risks to growth and downplaying topside risks to inflation. Markets reacted by sending EUR/USD and European yields lower.

- We continue to expect the ECB to deliver 25bp cuts at the upcoming meetings, bringing the deposit rate to 1.50% by September 2025.

As widely expected, the ECB cut all policy rates by 25bp today, bringing the deposit rate to 2.25%. There were no new staff projections at this meeting, and given the ‘Liberation Day’ disruption of global trade, the previous version from March is naturally outdated, which was evident from today’s rather vague assessment of the outlook.

In line with our expectations, the ECB struck a dovish tone, noting the downside risks to growth and downplaying topside risks to inflation. This was further highlighted by Lagarde during the press conference saying that “we are facing a negative demand shock” from Trump’s trade war, and hence that consensus within the Governing Council sess tariffs as dampening for the medium-term inflation outlook. The ECB removed its characterisation of the monetary policy stance “becoming meaningfully less restrictive“, with Lagarde referring to the previous wording as being meaningless given the current uncertainty on the neutral rate and the persistence of recent drivers of financial conditions (real rates, FX, credit premia). Incoming data will guide the ECB in its assessment on how to navigate the current environment on a meeting-by-meeting approach; but based on the communication from Lagarde today, we find that the easing bias remains in place.

Lagarde alluded to discussions of delivering a 50bp cut today, although she was vocal that no members were in favour of this option at today’s meeting. However, given the dovish assessment of the current balance of risk for growth/inflation, we do not rule out the risk that a couple of dire PMIs in April/May could build a case for a more pronounced easing of the policy stance at one of the next meetings.

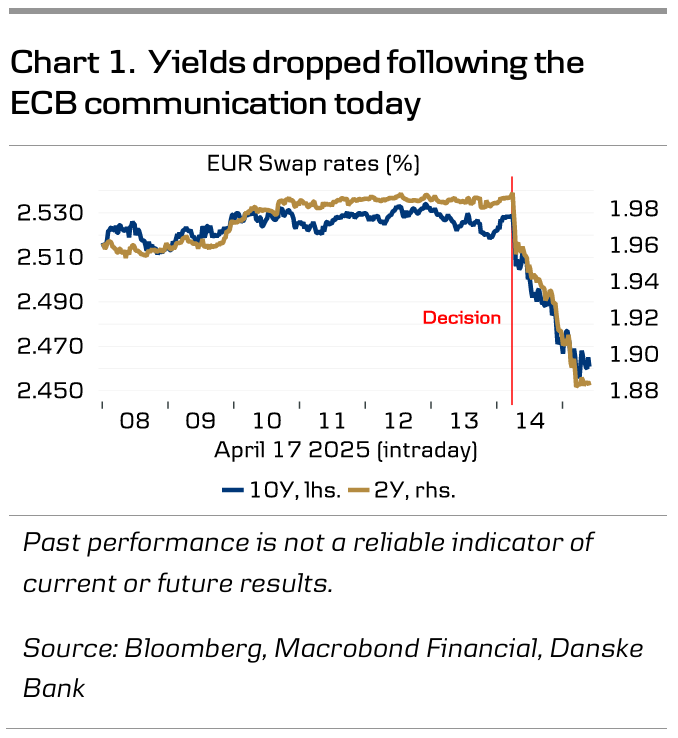

Market reaction. Markets reacted by sending European yields lower on the statement, with a further decline during the press conference. The 2Y swap rate dropped 10bp to below 1.90%, with the 10Y swap rate breaking below 2.50%. EUR/USD initially moved lower on the statement, but weak US data from the Philly Fed provided some support for the cross during the afternoon.

Our ECB call. We continue to expect the ECB to deliver 25bp cuts at the upcoming meetings, bringing the deposit rate to 1.50% by September 2025. Following trade war escalations, markets have recently converged with our view. We see risks to growth, inflation and rates, all to the downside in the medium term. Markets are pricing 22bp for June and 66bp for the remainder of the year.

{kind=link}