- We expect the Bank of England (BoE) to keep the Bank Rate at 4.00% on Thursday in line with consensus and market pricing. We now pencil in just two additional rate cuts through 2025-26.

- Data has come in on the hawkish side since the August meeting and both CPI and labour market report will follow next week ahead of the meeting.

- We expect a muted market reaction and remain bearish on GBP

We expect the BoE to keep the Bank Rate unchanged at 4.00% on Thursday 18 September in line with consensus and market pricing. Note, this meeting will not include updated projections or a press conference. The labour market report for July/August and CPI for August will be released just prior to the meeting next week and has the potential to heavily influence guidance at next week’s meeting. It will also be worth keeping an eye on the vote split, which caught a lot of attention at the previous meeting.

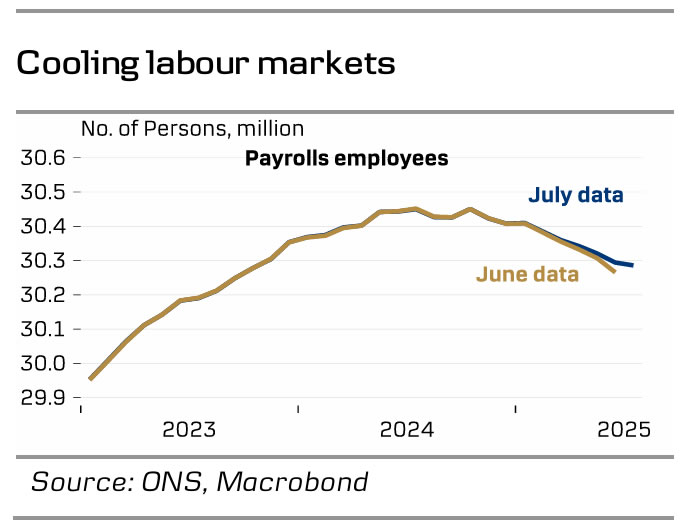

We expect the BoE to condition further rate cuts on disinflationary pressures, as we saw it in August. Since the last meeting, data has come into the hawkish side. Payrolls decline was less steep in July with 8K fewer jobs, the least since January. The weak development in previous months was also revised up, although the big picture is still a cooling labour market. Q2 GDP data was stronger than expected at 0.3% q/q, although largely driven by public spending. Retail sales data later showed a quite pronounced downward revision of H1, which indicates Q2 GDP-data could also be up for a revision lower. That said, July data showed a decent pickup. The notion of a continued modest recovery is supported by solid PMI data, particularly for services, while manufacturing remains quite weak. July CPI inflation came in higher than the BoE’s expectation. Headline inflation increased to 3.8% y/y in July with particularly service and food prices remaining elevated.

We will also look out for the annual decision on QT. The BoE has reduced its holdings by an annual pace of GBP100 bn. for two years now. Consensus is for slowing the pace to GDP72 bn. according to a Reuters survey.

BoE call. We expect the BoE to cut rates again in November, leaving the Bank Rate at 3.75% by YE2025, but we acknowledge that inflation will need to cool in August-September data for that to happen and see a substantial risk the next rate cut could be postponed. With the economy holding up better than expected and inflation still quite sticky above target, we revise our expectations for the bank rate next year and now expect one more cut in February leaving the Bank Rate at 3.50%.

Market reaction. We think the BoE is in wait and see mode which should imply a preference for not rocking the boat. That should mean a tempered market reaction. However, circumstances could change depending on upcoming data ahead of the meeting. More broadly, we stay negative on GBP. We therefore expect EUR/GBP to move higher towards 0.89 on a 6-12-month horizon.

{kind=link}