Summary

- As expected, the FOMC reduced the fed funds target range by 25 bps to 4.00%-4.25% at the conclusion of its meeting today, the first adjustment in nine months. Newly confirmed Governor Stephan Miran was the lone dissenter at the meeting, preferring to cut by 50 bps instead of 25 bps.

- The decision to ease reflected a “shift in the balance of risks” with the Committee believing that the “downside risks to employment have risen.” While inflation has ticked up since the spring, a development acknowledged in the post-meeting statement, job growth has downshifted sharply and the unemployment rate has risen to the top end of the Committee’s central tendency range consistent with full employment.

- Amid increased concerns about the jobs market, the median projection for the fed funds rate at the end of the year edged down by 25 bps to 3.625% relative to the previous projection from June, indicating an additional 50 bps of easing over the course of the FOMC’s October and December meetings. The median projection for 2026 dipped to 3.375%, implying just 25 bps of cuts next year remains the base case after a bit more easing this year. The median estimate for the longer-run, “neutral” fed funds rate was unchanged at 3.0%.

- Yet, Chair Powell in the post-meeting press conference struck a mildly hawkish tone in our view and continued to signal that the Committee remains in no rush to return to neutral. Rather, with policy still somewhat restrictive, Chair Powell characterized today’s adjustment as a “risk management cut” and the near-term monetary policy outlook as a “meeting-by-meeting situation.”

- Overall, the outcome of today’s meeting strikes us as a balanced response to the labor market’s loss of momentum and still elevated pace of inflation. With the Fed’s dual mandate in tension, what will the central bank do? We think the FOMC will put more weight on employment and cut the federal funds rate by 25 bps at each of its next two meetings, pushing the target range down to 3.50%-3.75% by year-end. We project two more 25 bps rate cuts at the March and June meetings next year followed by a long hold, resulting in a terminal fed funds rate of 3.00%-3.25%.

Chair Powell Corrals Most of the Cats

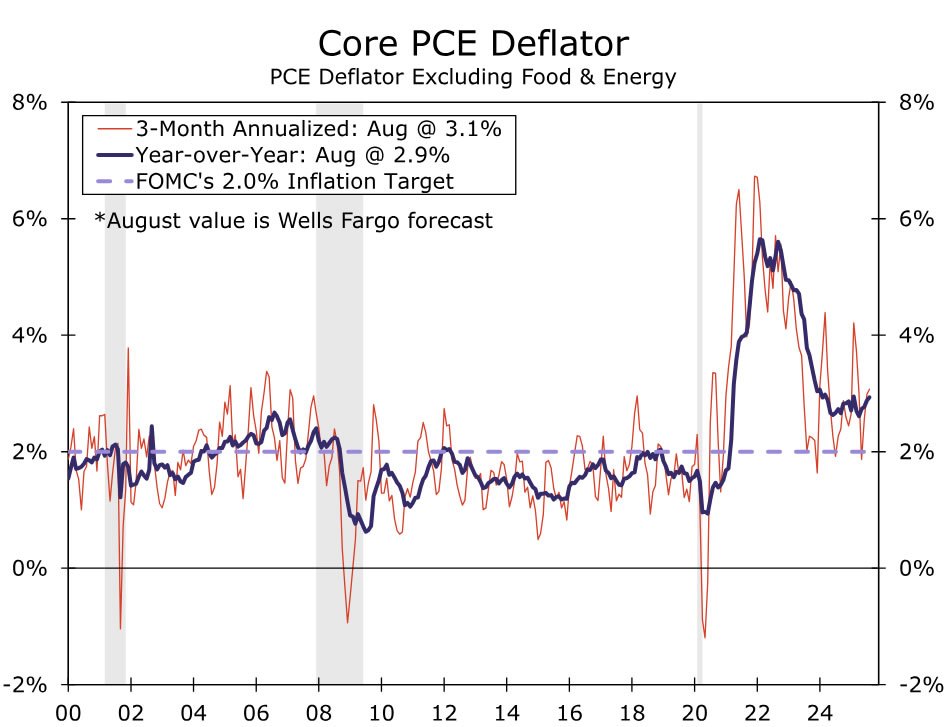

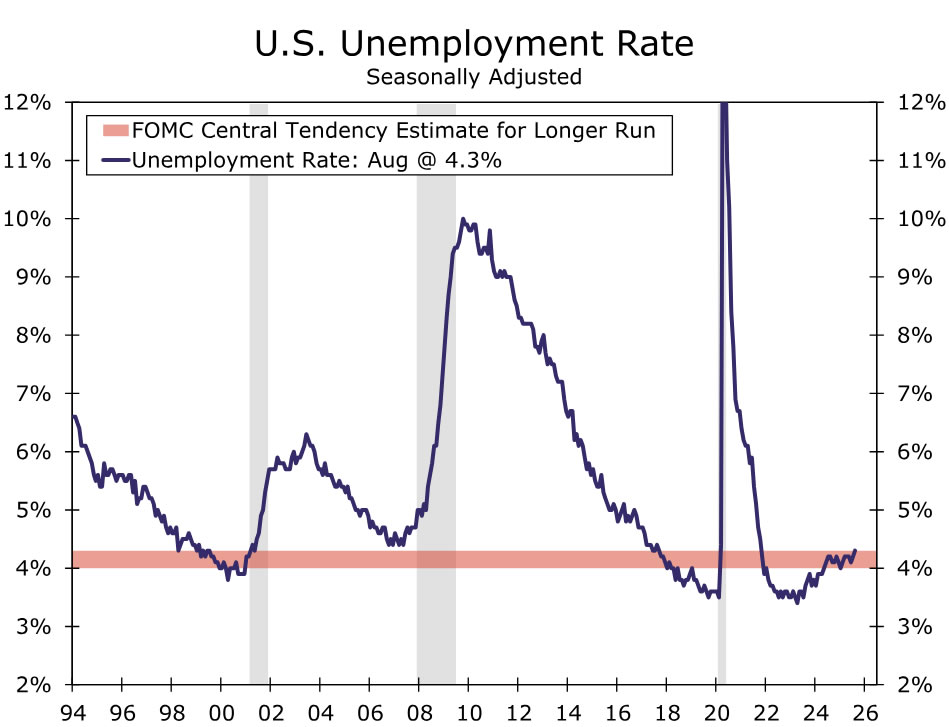

The September FOMC meeting did not disappoint. As was widely expected, the FOMC lowered the fed funds rate by 25 bps to 4.00%-4.25%. The move marked the first adjustment to the Committee’s policy rate since December and reflected a shifting balance of risk between the FOMC’s mandates of full employment and inflation. With the core PCE deflator running about a percentage point above target (Figure 1), the post-meeting statement maintained that inflation “remains somewhat elevated” and acknowledged that it has “moved up.” However, the recent deterioration in the jobs market overshadowed concerns about stubborn inflation. The Committee no longer views labor market conditions as “solid” and noted the recent slowdown in job growth and uptick in unemployment in its discussion of recent economic conditions (Figure 2). More tellingly, the statement added that “downside risks to employment have risen,” and that “in light of the shift in the balance of risks,” the FOMC decided to cut its policy rate. The post-meeting statement reaffirmed the ongoing pace of balance sheet runoff.

The decision was not unanimous but showed policymakers are generally more aligned than what many expected ahead of the meeting. Governor Stephan Miran, who was sworn in Tuesday morning ahead of the start of the meeting, was the lone dissenter and preferred a 50 bps rate cut. Governors Waller and Bowman, who both dissented in July, voted in line with the bulk of the Committee, while no partcipants dissented in a more hawkish direction.

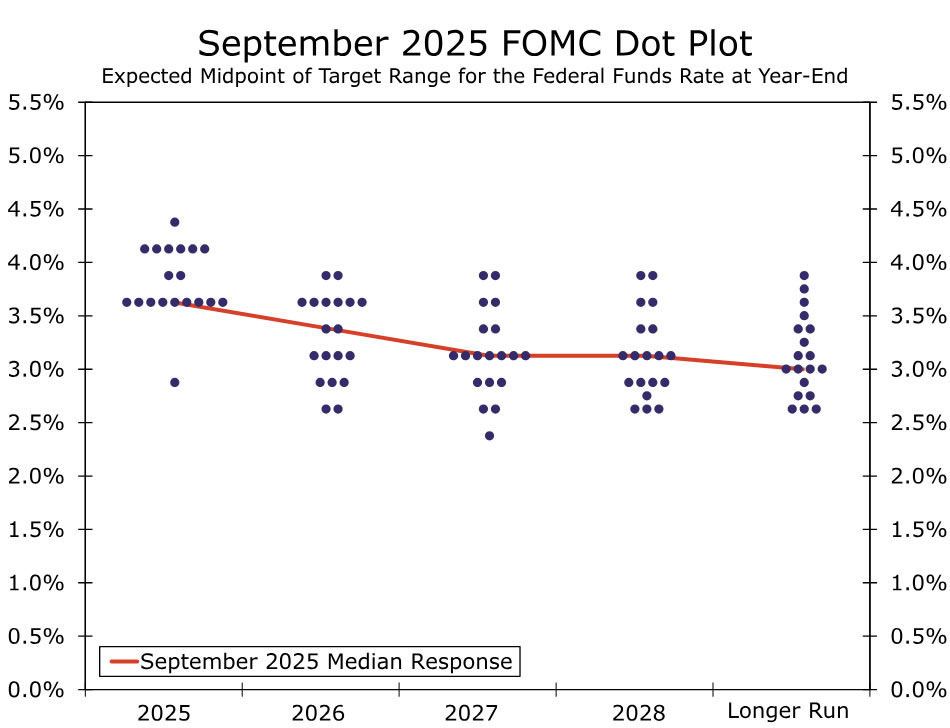

The Committee’s ongoing bias to ease was more apparent in the Summary of Economic Projections. The median projection for the fed funds rate at year end slipped to 3.625% from 3.875% in the June SEP, implying most officials see an additional 50 bps of easing over the Committee’s two remaining meetings of the year (Figure 3). The median dot for 2026 signaled just one cut next year, but this masks a decent amount of dispersion across the participants. Just two of the 19 participants were at the median (3.375%), and the median was just one dot away from slipping another 25 bps to 3.125%. Notably, the median estimate for the longer-run, “neutral” fed funds rate was unchanged at 3.0%. This underscores how most Committee members still view the policy setting as at least somewhat restrictive, giving some scope to lower the fed funds rate in an effort to cushion jobs market without outright accommodative monetary policy stoking higher inflation.

The Committee’s economic outlook brightened a bit relative to June, with 0.2 ppt increases in the median projections for real GDP growth in 2025 and 2026 and a 0.1 ppt increase to growth in 2027. The median forecast for the unemployment rate at year-end 2025 was unchanged at 4.5%, but it dropped by 0.1 ppt for 2026 and 2027. That said, the median headline and core inflation projections for 2026 rose by 0.2 ppt to 2.6% amid tariffs that are still slowly seeping into selling prices, expectations for stronger economic growth, anticipated fiscal policy stimulus and more accommodative monetary policy. The median participant’s projection does not have inflation returning to the FOMC’s 2.0% target until 2028.

In the press conference, Chair Powell struck a mildly more hawkish tone in our view, saying that he was not quite ready to say that a neutral policy stance was warranted and characterizing today’s rate cut as a “risk management” move. He also characterized the near-term monetary policy outlook as a “meeting-by-meeting situation” in a sign that although another two 25 bps rate cuts this year might be the base case, they are not a slam dunk pending new economic data in the coming months.

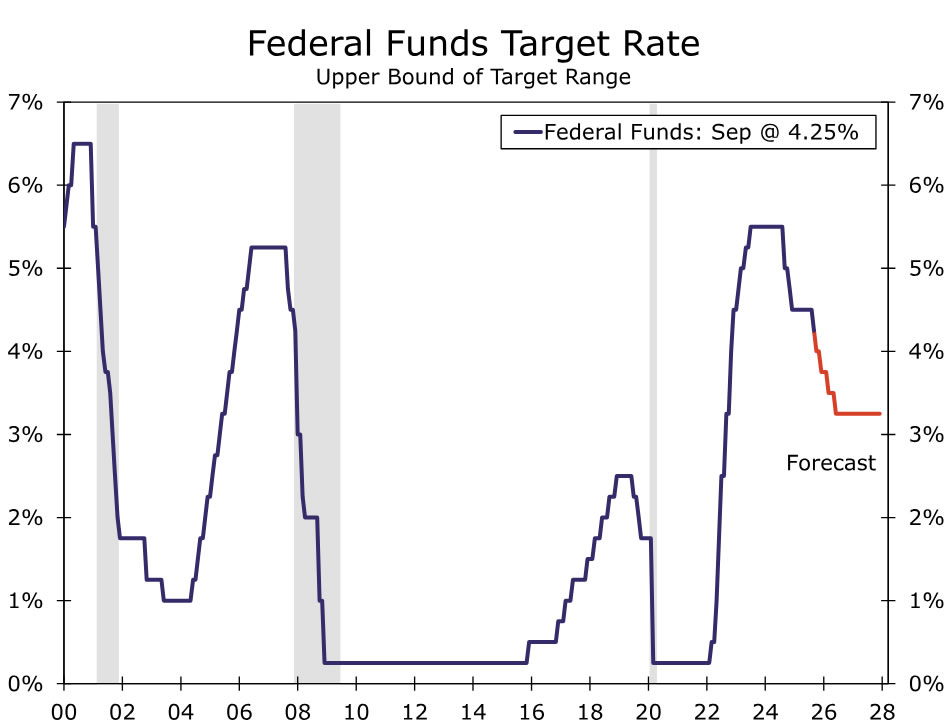

With the Fed’s dual mandate in tension, what will the central bank do? We think the FOMC will put more weight on employment and cut the federal funds rate by 25 bps at each of its next two meetings, pushing the target range down to 3.50%-3.75% by year-end. We project two more 25 bps rate cuts at the March and June meetings next year followed by a long hold, resulting in a terminal fed funds rate of 3.00%-3.25% (Figure 4).

{kind=link}