- We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 30 October in line with consensus and market pricing.

- Data has been close to expectations since the September meeting, and we therefore expect no shift in communication on the assessment of the economic outlook nor in the ‘meeting-by-meeting’ approach. We will pay close attention to any new details on the ‘good place’ assessment and what could change it.

- We expect a limited market reaction during the press conference.

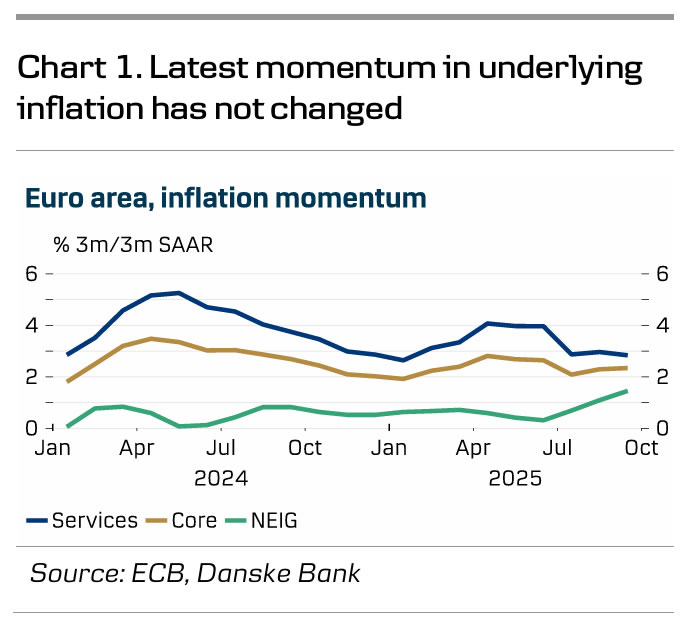

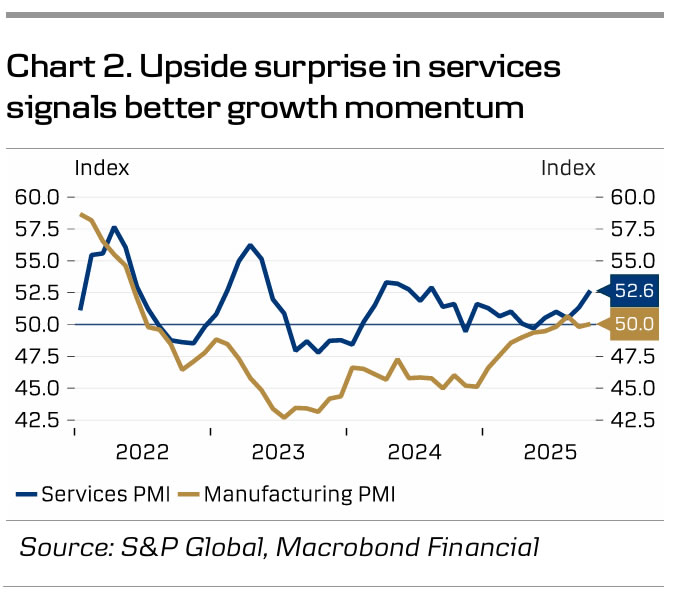

We expect the ECB to leave the deposit rate unchanged at 2.0% at the meeting on 30 October, in line with market pricing and consensus. Macro data since the September meeting has been close to expectations, suggesting the outlook has not changed. The September PMIs rose as expected while October PMIs surprised on the upside due to a strong increase in the services sector (see chart 2). PMIs suggest a slightly better growth momentum than the ECB staff projections, which forecasted 0.0% q/q GDP growth in Q3 and 0.2% q/q in Q4. Inflation ticked up to 2.2% y/y in September due to base effects while the momentum of underlying inflation was highly similar to that in recent months (see chart 1). September inflation thus aligned with staff projections for Q3 in both core and headline. Hence, we expect Lagarde to repeat the ‘meeting-by-meeting’ and ‘data-dependent’ approach.

Governing Council members continue to state that the ECB is ‘in a good place’, but there is growing divergence among members regarding the inflation outlook. This was evident in the minutes from the September meeting, where several members highlighted downside risks to inflation and expressed concerns regarding the euro’s strength and households’ persistently high savings rates. On the other hand, some members emphasised the potential inflationary effects of expansionary fiscal policies in the region and rising food inflation. We still see a clear majority of GC members that do not expect more cuts despite inflation projections being below target in both 2026 and 2027, but we are also hearing more dovish comments from e.g. Villeroy saying that a rate cut is more likely than a hike. Yet, with medium-term inflation expectations anchored close to 2%, decent October PMIs, and private consensus inflation expectations at 2% for 2027 we think the bar for another rate cut is high. This is also supported by the ECB seeing growth risks as balanced after having highlighted downside risks to growth since September 2023. Still, we do see a risk that the sentiment in the GC could change after the December staff projections if they show inflation below target on the full forecast horizon, including 2028.

Markets are currently pricing 2bp worth of cuts in 2025 and 10bp in 2026, leaving a 50% probability of one more rate cut. This chance of a cut has thus been lowered compared to before the September meeting when markets were pricing 8bp for 2025 and 8bp for 2026. While we see upside risks to current market pricing as we expect the ECB to remain on hold throughout 2026, we have recently taken profit on our payer positions in the short end of the EUR-swap curve as we see the risks as more balanced. At the press conference we will pay attention to communication about details on the ‘good place’ assessment by Lagarde and what potentially could change that view. However, we expect Lagarde to reiterate the place assessment but say that it is not fixed and that the ECB is ready to act.

. PMIs suggest a slightly better growth momentum than the ECB staff projections, which forecasted 0.0% q/q GDP growth in Q3 and 0.2% q/q in Q4. Inflation ticked up to 2.2% y/y in September due to base effects while the momentum of underlying inflation was highly similar to that in recent months (see chart 1). September inflation thus aligned with staff projections for Q3 in both core and headline. Hence, we expect Lagarde to repeat the 'meeting-by-meeting' and 'data-dependent' approach.){kind=link}