Summary

As we highlighted in our October International Economic Outlook, our views on the Bank of Canada (BoC) have changed. We now expect the BoC to cut its policy rate by 25 bps to 2.25% at October’s meeting, marking a shift from our prior forecast of a hold through December and through all of 2026. While we view tomorrow’s action to ease as the final cut in the BoC’s easing cycle, we believe the balance of risk is tilted toward more easing as uncertainty is elevated and growth prospects are subdued.

Bank of Canada Preview

In our October International Economic Outlook, we made an explicit adjustment to our Bank of Canada (BoC) forecast profile. To that point, we adjusted our view on the BoC’s October monetary policy decision, and we now expect BoC policymakers to deliver a 25 bps rate cut at this month’s meeting. Our revised view stems from our assessment of overall BoC monetary policy space, but also, in our view, policymakers’ seemingly stronger preference to support economic activity rather than control inflation.

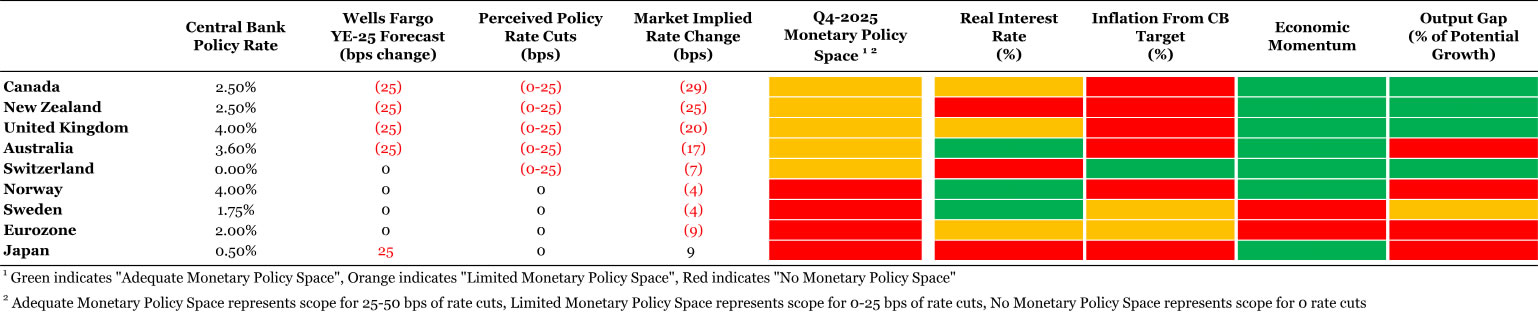

As far as monetary policy space, our forward-looking framework—which aggregates indicators including real interest rates, inflation trajectory, economic growth momentum and output gap—suggests that the Bank of Canada has room for additional interest rate cuts. In fairness, our framework says cutting rates is a close call as indicators are split. Split in the sense that policy settings and inflation indicators suggest the BoC should keep rates unchanged, but growth-related indicators say monetary policy should continue to be adjusted in a more accommodative direction, at least when all indicators are evenly weighted when assessed. However, as mentioned, we believe policymakers have communicated more of a bias toward supporting growth and are not overly concerned with inflation. Evidence can be found in the BoC’s prior official statement where policymakers were rather clear in that inflation risks have settled, but the economic outlook was deteriorating amid elevated uncertainty.

While recent inflation and jobs data surprised to the upside, we have yet to detect a change in sentiment on inflation from policymakers and the unemployment rate remains elevated. At the same time, uncertainty has increased as the Trump administration has signaled an additional 10% tariff will be imposed on Canadian exports to the United States. Reinforcing an elevated degree of uncertainty was a Q3 business outlook survey that painted a pessimistic picture of forward-looking growth prospects. This growth concern is compounded by mixed signals on consumer spending. Retail sales showed positive momentum in August, but Statistics Canada’s advance retail estimate points to a September contraction that will further complicate Q3 consumption and overall growth. Point being, when we adjust our framework to weigh growth momentum and growth prospects more heavily, we believe BoC policymakers have incentive to ease monetary policy in October rather than keep interest rates steady (Figure 1).

Source: Bloomberg Finance L.P. and Wells Fargo Economics

For now, we believe the October cut will be the final rate reduction in the Bank of Canada’s easing cycle. A cut this month would mean a terminal BoC rate of 2.25%; however, we believe the balance of risk is tilted toward more easing, with a terminal rate of 2.00% certainly a possibility. Leading indicators suggest growth is set to be sluggish for at least another quarter and possibly longer should latest tariff threats be imposed and should Canada opt to reinstate retaliatory tariffs amid the latest trade spat. A Federal Reserve that is also likely to be lowering policy rates into 2026 could also generate additional policy space for BoC policymakers to continue easing past October. To emphasize downside risks to our terminal rate forecast, our monetary policy framework, even after accounting for a cut in October, still screens that the BoC can deliver further easing, easing that financial markets are not fully priced for. Our framework also flags the BoC as having the most space of G10 central banks to continue easing past October, although similar to the dynamics around the October rate decision, there is a fine line between opting for more easing and holding rates steady. And finally, in addition to risks being skewed toward further easing beyond October, we do not anticipate Bank of Canada policymakers shifting toward rate hikes any time over our forecast horizon. Perhaps this longer-term BoC outlook can change over time, but for now, we do not see the evolution of Canada’s economy as consistent with tighter monetary policy through Q1-2027.

have changed. We now expect the BoC to cut its policy rate by 25 bps to 2.25% at October's meeting, marking a shift from our prior forecast of a hold through December and through all of 2026. While we view tomorrow's action to ease as the final cut in the BoC's easing cycle, we believe the balance of risk is tilted toward more easing as uncertainty is elevated and growth prospects are subdued.){kind=link}